The 2008 Economic Crisis

A bank run is like a fire in a crowded theater: it is collectively irrational for everyone to run, but perfectly understandable that when one person runs, everyone else runs too.

Terms

Subprime refers to “below standard.” More risky and speculative compared to standard, reliable credit.

Systemic risk is the risk of a breakdown across the entire financial system due to the scaling of problems at individual institutions or markets.

Securitization is the bundling of loans into standardized securities backed by those loans, which can then be traded like any other security.

QE is a non-standard central bank monetary policy in which the central bank (the Fed) purchases government and other securities on the secondary market, thereby increasing liquidity in the financial system.

LIBOR, or “London Interbank Offered Rate,” is the average interest rate on interbank loans in various currencies on the London market, at which banks lend each other U.S. dollars.

Treasury-bill rate is the yield on short-term U.S. government securities, Treasury bills (T-bills), issued by the U.S. Treasury with maturities of up to one year.

TED spread, or “Treasury-Eurodollar spread,” is the difference between the 3-month LIBOR rate and the 3-month Treasury-bill rate. This spread reflects the risk associated with interbank lending relative to essentially risk-free government bonds.

Case-Shiller Index is a measure of U.S. residential real estate price changes.

On the eve of the financial crisis

In early 2007, most people could not imagine that within two years the global financial system would face its most serious crisis since the Great Depression. At the time, the economy appeared to be growing. The last major disruption had been the collapse of technology companies in 2000-2002. The Federal Reserve had responded by cutting interest rates to prevent a recession.

First, the Fed’s rate cuts made credit more accessible and cheaper for both households and businesses. This boosted consumer demand and business investment. Lower borrowing costs meant that individuals and companies could take on more debt on more favorable terms.

Second, lower rates reduced borrowing costs for companies. This made it easier for businesses to access financing, supporting expansion. Cheaper credit helped companies innovate, scale up production, and create new jobs.

Third: housing market support. Lower mortgage rates made home loans more accessible and attractive to buyers. This stimulated new mortgage origination and drove demand for housing. The housing market stayed active on the back of lower rates.

Fourth, rate cuts contributed to stock market gains. Lower borrowing costs encouraged investors to take on debt to buy equities, increasing demand for shares and pushing prices higher. This created positive market sentiment and expanded investment.

Finally, lower rates reduced yields on dollar-denominated debt securities, which weakened the dollar and had a positive effect on U.S. exports and investment inflows. A cheaper dollar made American goods and services more competitive on world markets, supporting export growth.

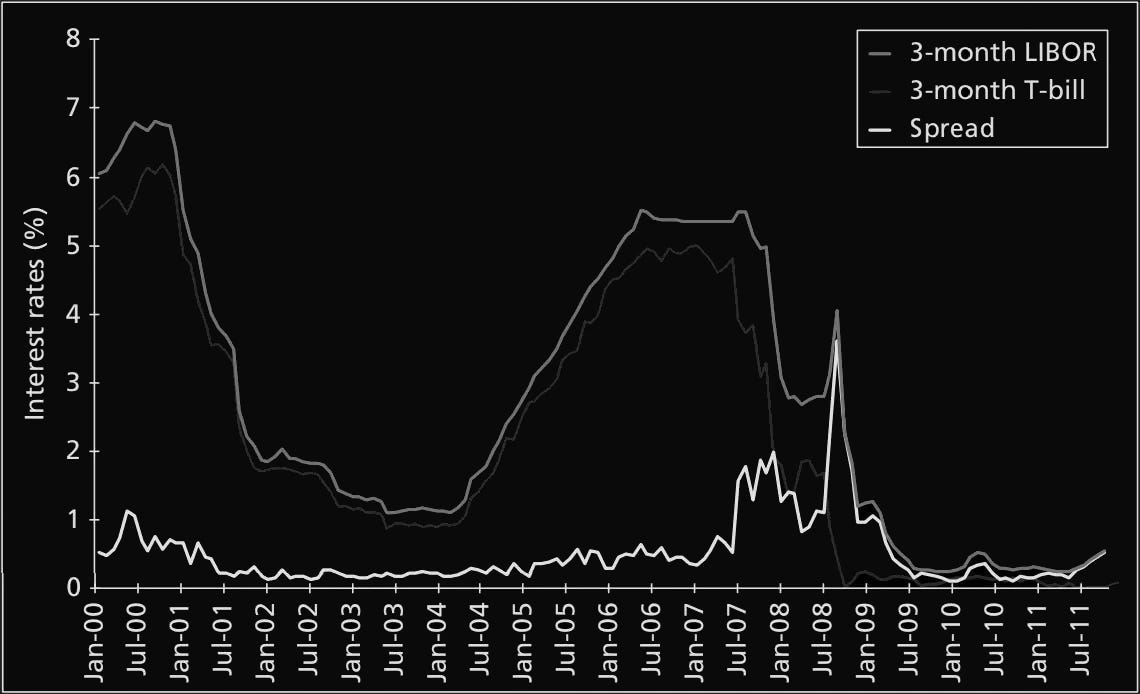

As described above, the Fed’s rate cuts pulled down rates on other short-term debt instruments as well: LIBOR, Treasury bills, and the TED spread.

Chart 1 shows that from 2001 to 2004, Treasury-bill rates and LIBOR, the rate at which banks lend to each other, fell simultaneously. These actions helped prevent a prolonged economic downturn, and the recession was brief, without producing serious damage to the economy.

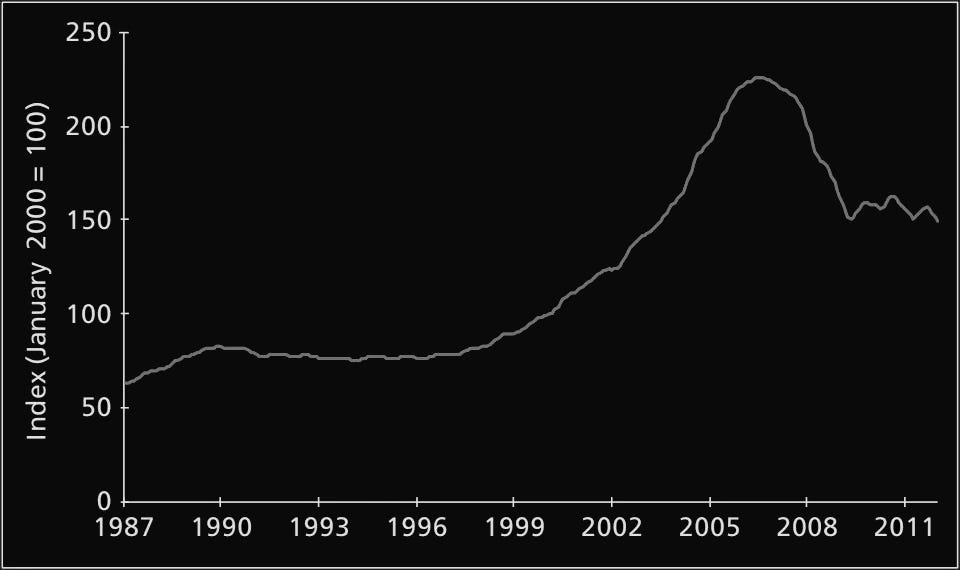

By the mid-2000s, the economy looked solid. After the sharp equity market decline in 2000-2002, markets began recovering sharply from 2003 (Chart 2) and recovered all losses from the technology crisis. The banking system also appeared sound.

One useful measure of bank stability was the TED spread: the difference between LIBOR (the rate at which banks borrowed from each other) and the Treasury-bill rate (the rate at which the U.S. government borrowed). In early 2007, this figure stood at just 0.25%, signaling that banks viewed default or financial system risk as unlikely.

The combination of low interest rates and a stable economy produced a real estate boom. U.S. home prices began rising in the late 1990s and accelerated after 2001, when rates fell sharply. Over the ten years from 1997, average property prices tripled (Chart 3).

But Americans’ confidence in low financial risk, the economy’s recovery from the tech crisis, and rising real estate prices supported by falling interest rates all contributed to the 2008 crisis.

On one side, lower rates reduced returns on various investments, and investors searched for higher-yielding alternatives. On the other, low volatility and confidence in the absence of risk made investors less cautious, leading to a rise in risky investments, including mortgage loans. The U.S. real estate and mortgage lending market ended up at the center of the crisis.

Risky practices in mortgage lending

Before the 1970s, most mortgage loans were made by local lenders such as savings banks or credit unions. Homeowners took out long-term loans, typically 30 years, to buy a house and repaid them gradually. The primary asset of these lending institutions was mortgage loans; depositor funds were the primary liability.

The situation changed in the 1970s, when Lewis Ranieri, a vice president at Solomon Brothers, introduced the idea of buying large volumes of mortgage loans from lenders, pooling them, and selling the pools as financial instruments. These pools became known as “mortgage-backed securities.” Fannie Mae and Freddie Mac took on this role. The process eventually came to be called securitization. Fannie and Freddie became dominant players in the mortgage market, purchasing more than half of all mortgages originated by private companies.

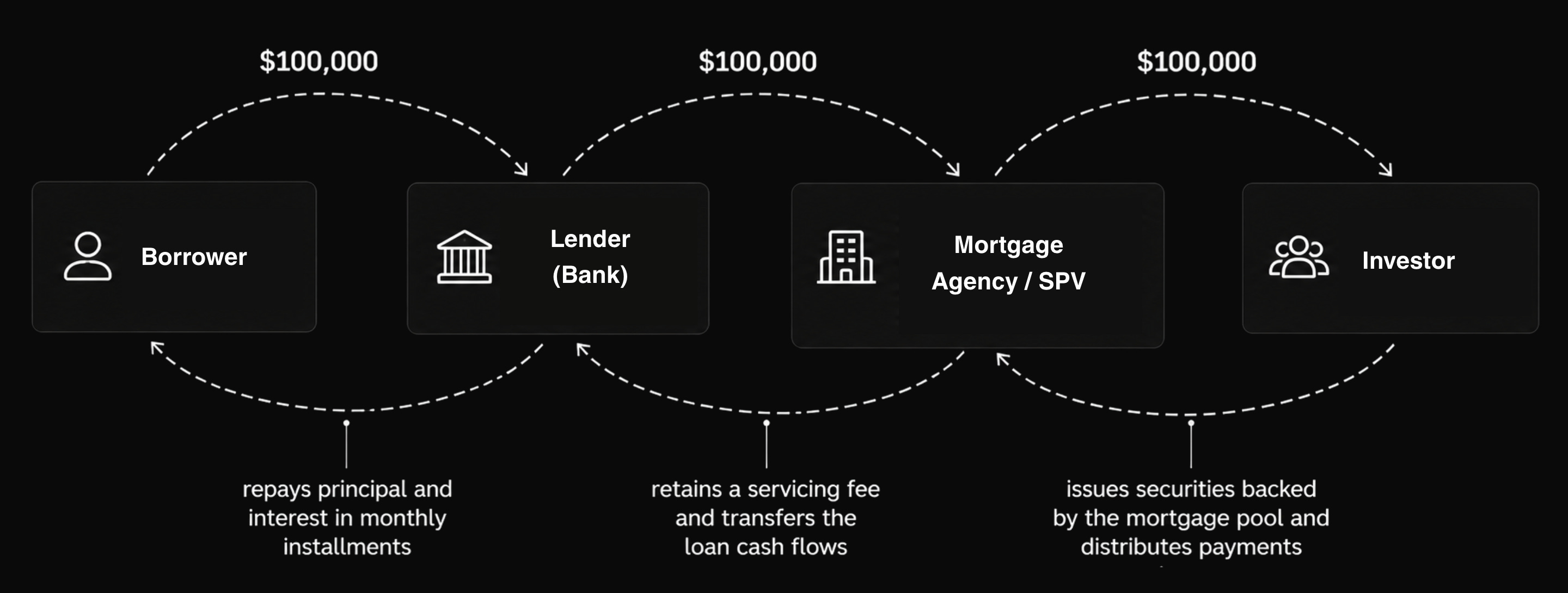

Diagram 1. Cash flows in mortgage-backed securities.

Diagram 1 shows the path of cash flows from the original borrower to the end investor in a mortgage-backed security. It starts with the originating institution (say, a bank) making a loan to a borrower for $100,000. The borrower repays principal and interest over 30 years. The lender then sells the loan to a company such as Freddie Mac or Fannie Mae and gets its money back.

The lender can continue to service the loan, collecting monthly payments from the borrower and earning a fee for doing so. The loan payments, net of that fee, are passed on to the agency (Freddie or Fannie). These agencies pool multiple loans into mortgage-backed securities and sell them to investors such as pension funds or investment funds. The agency (Fannie or Freddie) typically guarantees that credit risk within each pool is minimal and receives a fee for this. The remaining cash flows then pass to the end investor. Mortgage-backed securities are sometimes called “pass-throughs” because of this cash-flow structure.

Until the final decade before the crisis, most mortgages bundled into mortgage-backed securities were owned or guaranteed by the government-sponsored entities Freddie Mac and Fannie Mae. These loans were low-risk and met defined standards: the loan amount, for instance, could not exceed 80% of the home’s value.

As securitization developed, mortgages began appearing that didn’t meet these standards and carried higher default risk. Private companies began securitizing these “non-conforming” loans. The key distinction was that investors in these securitized loans had no government guarantee and therefore bore borrower default risk directly.

This created a situation in which mortgage brokers originating these loans didn’t always conduct proper borrower vetting, since they could sell the loans to investors without bearing responsibility for possible defaults.

Those investors, naturally, had no contact with borrowers and couldn’t conduct detailed credit quality checks. Instead, they relied on borrower credit scores, which gradually displaced traditional due diligence.

A consistent trend soon emerged toward loans with minimal borrower documentation, and then with no documentation at all, requiring no verification of the borrower’s ability to service the debt. Other underwriting standards deteriorated as well. The permissible leverage on residential loans (measured by the loan-to-value ratio) rose sharply. By 2006, most subprime borrowers were purchasing homes by borrowing the full purchase price.

When home prices began falling, these highly leveraged loans quickly went “underwater”: the house was worth less than the outstanding loan balance, and many homeowners chose to walk away from both their homes and their debts.

Adjustable-rate mortgages became very popular, particularly among borrowers with weak credit histories. These loans offered low initial rates that could later reset: rising to the prevailing market rate plus a spread. Many borrowers used these low initial rates to buy homes, but when the loan rate began to rise, their monthly payments increased sharply, particularly as overall market rates moved higher.

Despite the risks inherent in adjustable-rate mortgages, many investors were confident that continuous home price appreciation would bail out bad loans. But from 2004 onward, the ability to refinance began to diminish:

Rising interest rates began creating problems for homeowners with variable-rate mortgages.

Home prices peaked around 2006, limiting homeowners’ ability to use home equity for refinancing. In 2007, mortgage delinquencies and losses on mortgage-backed securities began rising sharply.

That was the beginning of a financial crisis that would eventually damage the entire world.

Why did investors buy risky mortgages?

In practice, these mortgage loans were not treated as risky, and their ratings were high. The answer lies in financial engineering: securitization, restructuring, and credit enhancement. These mechanisms allowed investment banks to create high-rated securities (AAA, for example) from junk loans. One of the most important and destructive instruments in this process was the collateralized debt obligation, or CDO.

CDOs were designed to concentrate default risk from a common loan pool on certain investors, leaving others better protected from that risk. The idea: take a large number of loans that people took out at banks, bundle them into a single pool, then split the pool into two parts called “tranches.” There are senior and junior tranches. Senior tranches receive payments first; they have priority and are genuinely secured (most likely to be paid). Junior tranches receive payments only after senior tranches have been paid.

Why does this matter? Because senior tranches were considered safer. Even with risky underlying loans, a default rate above 30% seemed unlikely, so senior tranches often received the highest rating (AAA) from major rating agencies: Moody’s, Standard & Poor’s, and Fitch. A pool of low-rated mortgage loans thus produced AAA-rated securities.

CDOs, in theory, helped manage risk and create safe investments even from some risky loans. With hindsight, it’s obvious those ratings were completely wrong. The CDO structure made senior tranches less protected than investors believed. When home prices began falling nationwide, defaults occurred everywhere, and the expected diversification benefits never materialized.

Why did rating agencies underestimate the risks in these securities?

First, they relied on historical data that failed to account for changes such as the sharp run-up in residential real estate prices and the shift in borrower types: people taking loans with no down payments, rising payment schedules, and minimal documentation.

Second, there were obvious agency problems. Rating agencies were simply paid to assign ratings. They faced pressure from issuers who could shop for the most favorable terms, with the goal of securing high ratings.

Credit default swaps

Parallel to the CDO market, the credit default swap market was developing during this period.

A credit default swap, or CDS, is essentially an insurance contract against the default of one or more borrowers. The buyer of the swap pays an annual premium (similar to an insurance premium) for protection against credit risk. CDS became an alternative method of credit enhancement, ostensibly allowing investors to buy subprime loans and insure their safety.

The problem was that some companies selling CDS did not have sufficient capital to cover their obligations. AIG, for instance, sold CDS on risky mortgage loans totaling over $400 billion, with no ability to pay out if defaults occurred.

The rise of systemic risk

By 2007, problems had accumulated in the financial system. Many banks and investment companies were using short-term borrowing to fund long-term investments (such as mortgage-backed securities). This meant they constantly needed to raise new financing to refinance old debts. They had also taken on very large debt loads and depended on a continuous inflow of new funds. If markets suddenly stopped providing new debt, default risk would materialize. Many of the assets purchased with borrowed money (mortgage-backed securities) were illiquid: they couldn’t be sold quickly to repay debts.

Investment firms had also dramatically increased their leverage, making them vulnerable to funding risk, especially if asset prices fell. Even small losses could render them insolvent, at which point no one would want to lend them new funds.

An additional source of problems was investors’ heavy use of credit protection products including CDOs. Many assets inside these pools were illiquid and difficult to value, with prices highly sensitive to forecasts about future credit markets. If the economy turned down and credit ratings fell, selling these assets would be a difficult task.

On regulated exchanges, such as futures and options markets, participants must post collateral to guarantee their obligations. Prices are marked to market daily, and gains or losses are automatically debited or credited to traders’ accounts. If losses are too large and collateral is exhausted, the trader must post additional funds or close positions to avoid insolvency. All participants can see each other’s positions and risks.

On “over-the-counter” markets, where CDS contracts traded, contracts were concluded between two parties with less information available on positions and risks. Tracking profits and losses over time and assessing each participant’s credit risk was far more difficult.

This financial model carried systemic risk: the potential collapse of the financial system when problems in one market spill into others. When lenders such as banks have limited capital and fear further losses, they may rationally choose to hold onto that capital rather than deploy it to clients such as small businesses, thereby compounding funding problems for their ordinary borrowers. Any reduction in lending always harms the broader economy.

The crash

By autumn 2007, home prices had fallen, mortgage delinquencies had risen, and the stock market had begun its freefall. Many investment banks with large exposures to mortgage loans also began to experience difficulties.

In September 2008, the crisis reached a catastrophic inflection point. First, the federal agencies Fannie Mae and Freddie Mac, which held enormous quantities of impaired mortgage loans, were placed under government conservatorship. This triggered panic on financial markets.

Two of the largest investment banks, which had suffered serious losses from purchasing risky assets, came under severe pressure: Lehman Brothers and Merrill Lynch.

Merrill Lynch avoided bankruptcy: Bank of America agreed to acquire the firm for $50 billion in a government-supported transaction. Merrill Lynch became a division of Bank of America. Merrill Lynch’s depositors and clients did not lose their funds; their accounts, assets, and liabilities were transferred to Bank of America (and it was an excellent acquisition for the buyer). Losses fell only on the company’s shareholders.

The sale of Merrill Lynch preserved the firm and prevented far larger shocks to the financial system that would inevitably have followed its bankruptcy. Lehman Brothers, unfortunately, found no buyer. No one was interested in acquiring the bank, as its losses were considerably larger than Merrill Lynch’s. Buying a bank means taking on all of its liabilities and problems, and neither other banks nor the government had an interest in facilitating such a deal. Because beyond Lehman, there was also the problem of AIG: the government was forced to extend a credit line to the company to prevent its collapse, since AIG had guaranteed enormous volumes of CDS transactions and its failure could have severely damaged the banking system. The Treasury then proposed a $700 billion facility to purchase distressed mortgage-backed securities.

The Lehman Brothers bankruptcy had a severe impact on the short-term credit market. Lehman had been borrowing large sums by issuing short-term debt instruments known as commercial paper. The primary investors in these instruments were money market funds, which invested in short-term, safe debt obligations. When Lehman failed, concerns arose that these funds might suffer losses on their large commercial paper holdings, and fund clients began withdrawing their money. The funds in turn began shedding commercial paper and moving into safer, more liquid Treasury bills. This caused short-term funding markets to close.

The freeze in short-term credit markets compounded the financial crisis. Large companies and banks found it difficult to obtain short-term credit. Small businesses that depended on bank loans were also affected and could not continue operating. Companies without sufficient capital were forced to scale back operations.

Unemployment rose sharply, and the economy entered a deep recession. The crisis on financial markets spilled into the real economy, and the damage spread across the world.

Wall Street reform

The crisis generated extensive discussion about how to improve financial system governance and reduce risk. In 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act was passed, proposing changes to reduce the danger of a systemic crisis.

The law requires banks to hold more capital: a financial reserve they must maintain. This matters because, if a bank runs into trouble, more capital allows it to better absorb losses and reduces the risk that its failure will affect other banks. Also, when banks have more of their own skin in the game, it may encourage them to take less risk, since they themselves bear the losses rather than government entities such as the FDIC.

Transparency requirements, particularly in derivatives markets. Standardizing CDS contracts, for instance, so they can trade on centralized exchanges for proper regulation. Daily margin requirements prevent CDS market participants from taking positions that exceed their capacity, and exchange trading makes it easier to analyze firms’ exposure to losses in these markets.

Restrictions on risky activities banks can engage in. The so-called Volcker Rule, named after former Fed Chair Paul Volcker, limits banks’ ability to trade for their own account and to own or invest in hedge funds or private equity funds.

Addressing regulatory oversight gaps that became apparent in 2008, by providing clear authority and accountability to different regulators to avoid duplication and “regulatory arbitrage,” where an issuer seeks out the most permissive regulator to boost securities’ credit ratings.

Compensation structures that incentivize employees to act in the company’s long-term interest rather than for quick profit. Specifically, employee compensation (bonuses, options, etc.) should depend on long-term performance results, not just quarterly or annual profit figures. If executives misstate financial results to show better numbers and collect bonuses, they should be required to return those bonuses. This is meant to prevent excessive risk-taking by companies and their executives: banks sometimes take enormous risks in pursuit of large profits and corresponding bonuses for senior management, but when things go wrong, losses fall on the company and even on the government. Rating agency incentives: few people are comfortable with a system in which rating agencies are paid by the firms they rate. The law provides for the creation of an Office of Credit Ratings within the Securities and Exchange Commission to oversee rating agencies.

All of this is logical and coherent. But was the law fully implemented?

No. Some provisions of Dodd-Frank were enacted, but key points never took effect or were later rolled back. The Volcker Rule was substantially weakened and allows banks to invest in hedge funds and private funds within defined limits. Requirements for the segregation of client funds and banks’ proprietary operations were never adopted. Derivatives trading regulation was relaxed in favor of banks. Proposals to cap executive compensation at banks found little support. And reform of rating agencies produced no meaningful change to their business model or conflict of interest. The crisis did not, in the end, lead to the sweeping and successful reforms that had been intended.

The printing press and the Fed

Wall Street reforms were unsuccessful, but the shift in Fed policy is a different story. In response to the global financial crisis of 2008, the Fed fundamentally changed the direction of its policy. These changes were a response to the scale of the disruption to the economy and financial system, and reflected central banks’ transition to quantitative easing.

After the Lehman Brothers bankruptcy in September 2008, the global economy faced a sharp contraction in liquidity, collapsing equity markets, and the risk of a full-scale crisis. The Fed under Ben Bernanke began aggressively cutting interest rates. By December 2008, the rate had been lowered to essentially zero (0-0.25%), where it remained for seven years, until December 2015.

This aggressive monetary stimulus was meant to support consumer demand, prevent deflation, and stabilize the financial system. But rate cuts alone, as a regulatory tool, proved insufficient. Non-standard measures were needed to flood the economy with liquidity.

In November 2008, the Fed announced the first round of its quantitative easing program (QE1). Under QE1, the Fed purchased mortgage-backed securities and government bonds totaling up to $1.75 trillion: a “printing press” to expand the money supply and stimulate demand. QE1 ended in March 2010, but a second round (QE2) launched in November 2010, purchasing $600 billion in assets through June 2011. QE3 started in September 2012, with the Fed buying $85 billion in assets per month. Over the full QE period from 2008 to 2014, the Fed expanded its balance sheet more than fourfold, from $900 billion to $4.5 trillion.

Large-scale quantitative easing was accompanied by a shift to a 2% annual inflation target. This allowed stimulus policy to remain in place longer under conditions of low inflation. Another development was the introduction of forward guidance in 2011: the Fed began publishing projections of the future path of interest rates, substantially improving the transparency of monetary policy for markets.

The Fed’s QE measures from 2008 to 2014 succeeded in avoiding a deflationary spiral, stabilizing the banking system and equity markets, and maintaining credit availability. The one problem: the new Fed measures did not solve the problem of low economic growth and contributed in large part to the formation of financial bubbles through excess liquidity. The impact of Fed policy in the post-2008 period remains a subject of debate to this day.

Conclusion

Ben Bernanke, Fed Chair from 2006 to 2014, cited in one interview the emergence of panic and the loss of confidence in the financial system as the primary cause of the global financial crisis of 2008: a modern-day “bank run”:

“People talk a lot about the housing bubble and subprime mortgages in the United States. By 2006-2007 we saw that house prices were falling, there were problems with mortgage loans, foreclosures were rising, and so on. What we didn’t fully anticipate was that the subprime mortgage crisis and problems in other credit markets would create a broad financial panic. It was the panic, the runs on short-term credit that brought down or nearly brought down many large financial institutions and turned it into a global financial crisis. A bank run is like a fire in a crowded theater: it is collectively irrational for everyone to run, but perfectly understandable that when one person runs, everyone else runs too. A widespread panic arose in which fear dominated the financial system and nearly shut it down entirely.”

The human factor, specifically the fear and panic of depositors, played a central role in the escalation of the financial crisis. Despite the existing economic problems and structural deficiencies, there is no country that has ever been immune to financial imbalances and disruptions. As an economy grows, the number of potential risks always grows with it.

In fact, in 2008 the share of low-credit-quality subprime loans in the overall mortgage market was not large. The majority of mortgage loans had been made to borrowers with solid credit histories and collateral. The question of ensuring banking system liquidity could also have been resolved without the need for the Fed's aggressive quantitative easing. But depositor panic, and regulators' insufficiently rapid response, created additional difficulties and made the situation worse.