Coherent Corp.

To truly appreciate the depth and scale of the new era of technology, you need to look below the waterline and examine those who are holding up that massive block of ice.

About the Company

Coherent is a global technology leader in materials, lasers, and components for telecommunications. Founded in 1971, the company has spent more than 50 years evolving into a vertically integrated supplier of advanced solutions for telecommunications, from materials and components to subsystems and systems. It serves several end markets.

Products and Markets

Industrial: fiber lasers used for battery laser welding, particularly in EV battery manufacturing, and in the production of advanced medical devices. Ultraviolet lasers used in semiconductor and display equipment, covering everything from ingots to packaged integrated circuits, as well as in the production of OLED displays for mobile devices and micro-LEDs for high-end televisions and large displays. The portfolio also includes complex laser systems and subsystems for a wide range of industrial applications including aerospace and defense, laser components, optics and crystals, and high-performance materials such as ceramics, metal matrix composites, and diamond materials.

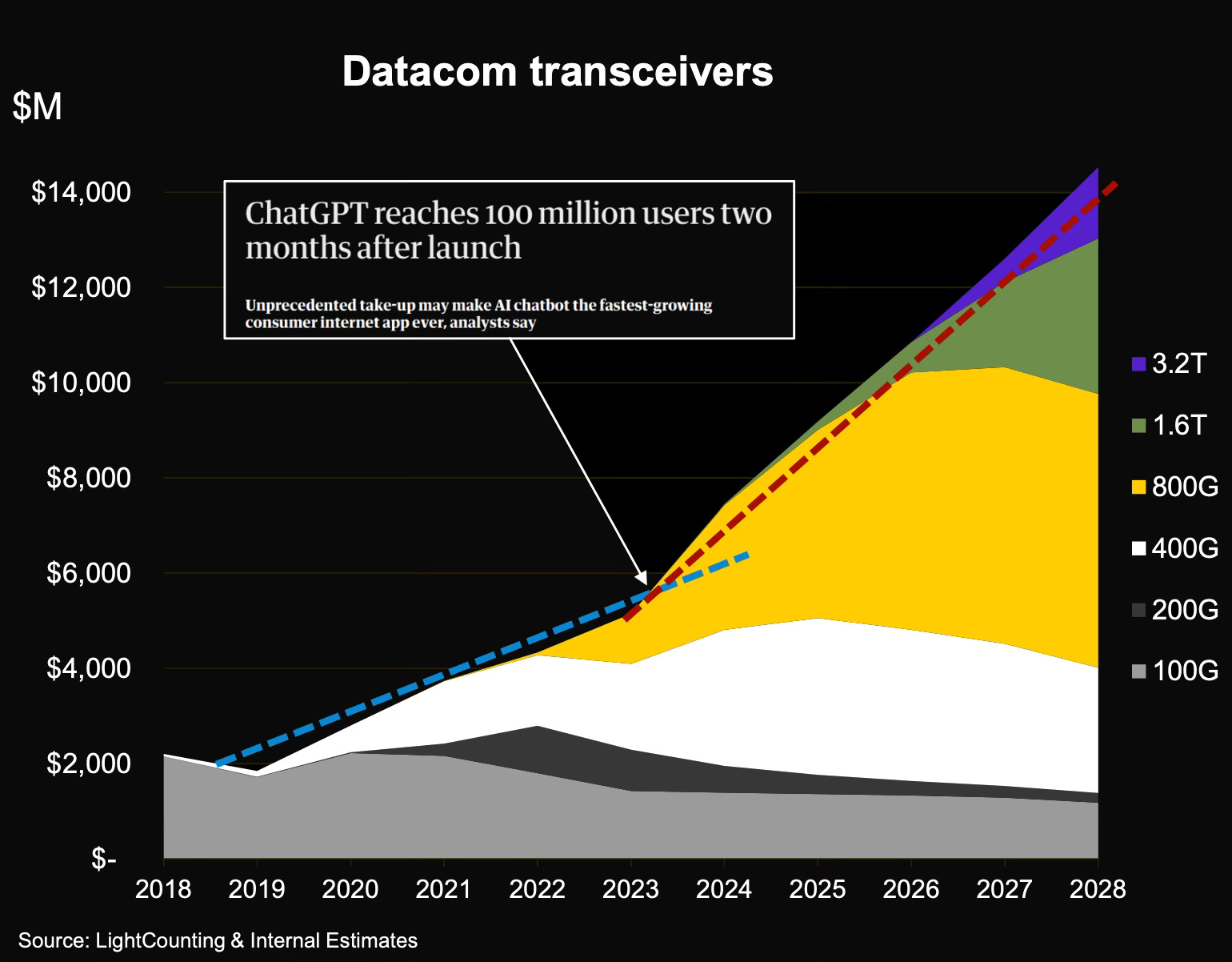

Telecommunications: embedded coherent transceivers, which are devices used in optical telecom networks to transmit large volumes of data over long distances via fiber optic cables using laser technology. The key differentiator of coherent transceivers is sophisticated signal processing on both the transmit and receive sides, enabling data transmission at far higher speeds and over much greater distances with less loss and distortion compared to conventional optical transceivers. This makes coherent transceivers critical for building the high-speed backbone and metro networks of modern telecom operators and cloud providers. These transceivers support data rates from 100 to 800 Gbps, while conventional optical transceivers top out at 400 Gbps. Coherent is ahead of the competition on speed. The telecom portfolio also includes datacom transceivers for expanding cloud infrastructure bandwidth (with AI/ML components), wavelength selective switches for optical network routing, embedded optical line subsystems for network flexibility and scalability, pump lasers for terrestrial and submarine telecom systems, and laser diodes based on indium phosphide (InP) and gallium arsenide (GaAs) vertical-cavity surface-emitting lasers (VCSELs). InP lasers are widely used as light sources for optical transceivers in telecom equipment; GaAs VCSELs are widely used in optical interfaces for short-reach links inside and between servers in data centers, as well as in consumer electronics, sensors, and other devices. Both types are valued for their small size, energy efficiency, and integrability into optical data transmission circuits.

Electronics: Coherent produces and supplies high-technology components for consumer and automotive electronics. Its sensors are used in AR/VR devices and wearables for health monitoring. Lasers support 3D sensing and precision distance measurement. In vehicles, the company’s components improve EV performance and autonomous driving systems. The company also develops materials and optics for improved displays and communications systems.

Instrumentation: Coherent produces components and systems for instrumentation in medicine and science, including technologies for smart healthcare, rapid and precise medical diagnostics, and personalized medicine. For scientific research, the company develops environmental monitoring instruments and advanced research tools. Coherent also offers optics, lasers, and thermoelectric components used in biotechnology and environmental research, consistently bringing new innovations to market.

Revenue Structure

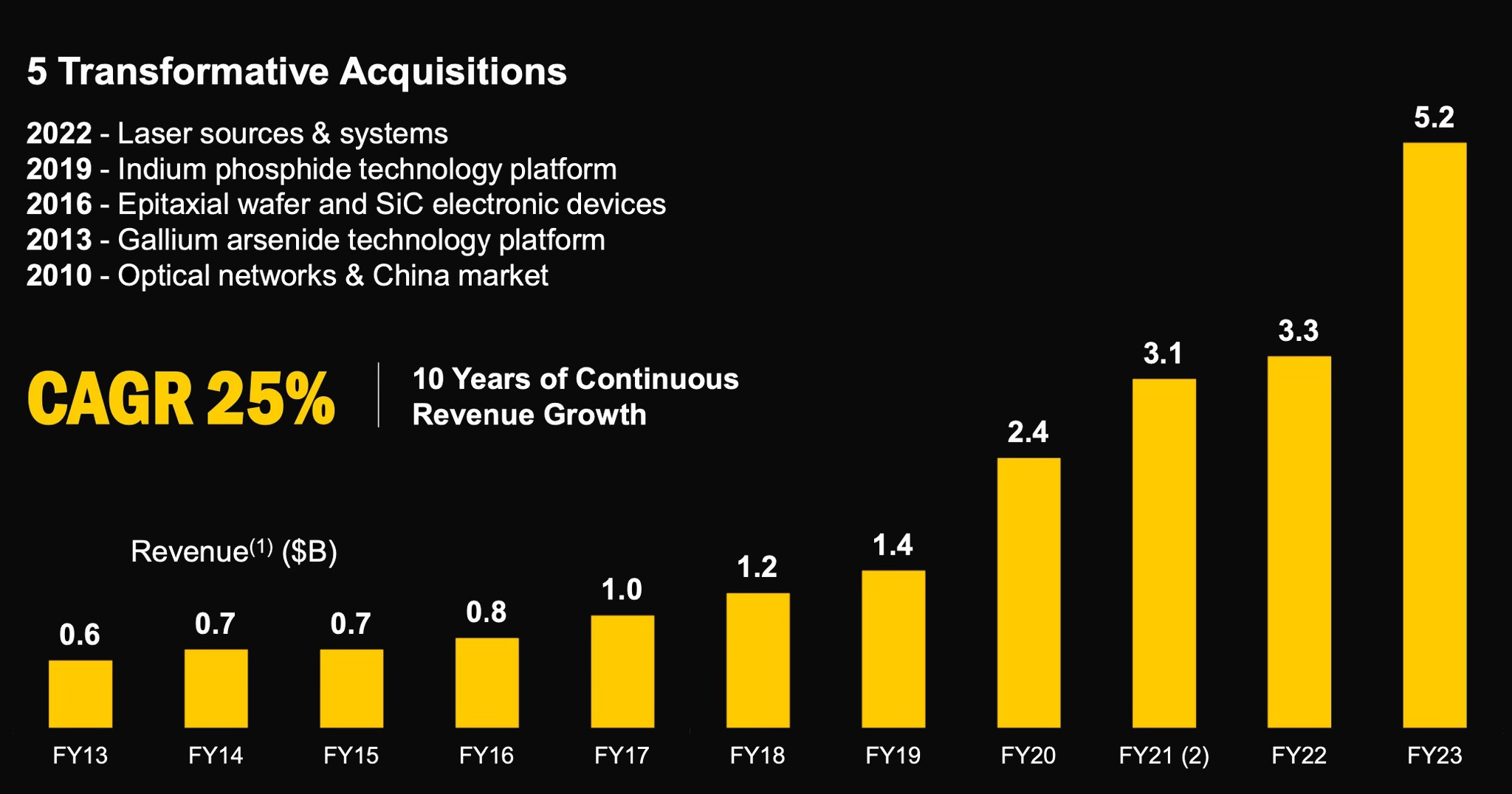

The company’s ten-year average revenue CAGR is 25%. Five significant acquisitions also contributed to this revenue growth. From all of the above, the natural question is: where does the money actually come from? The deliberate emphasis on telecommunications earlier was intentional.

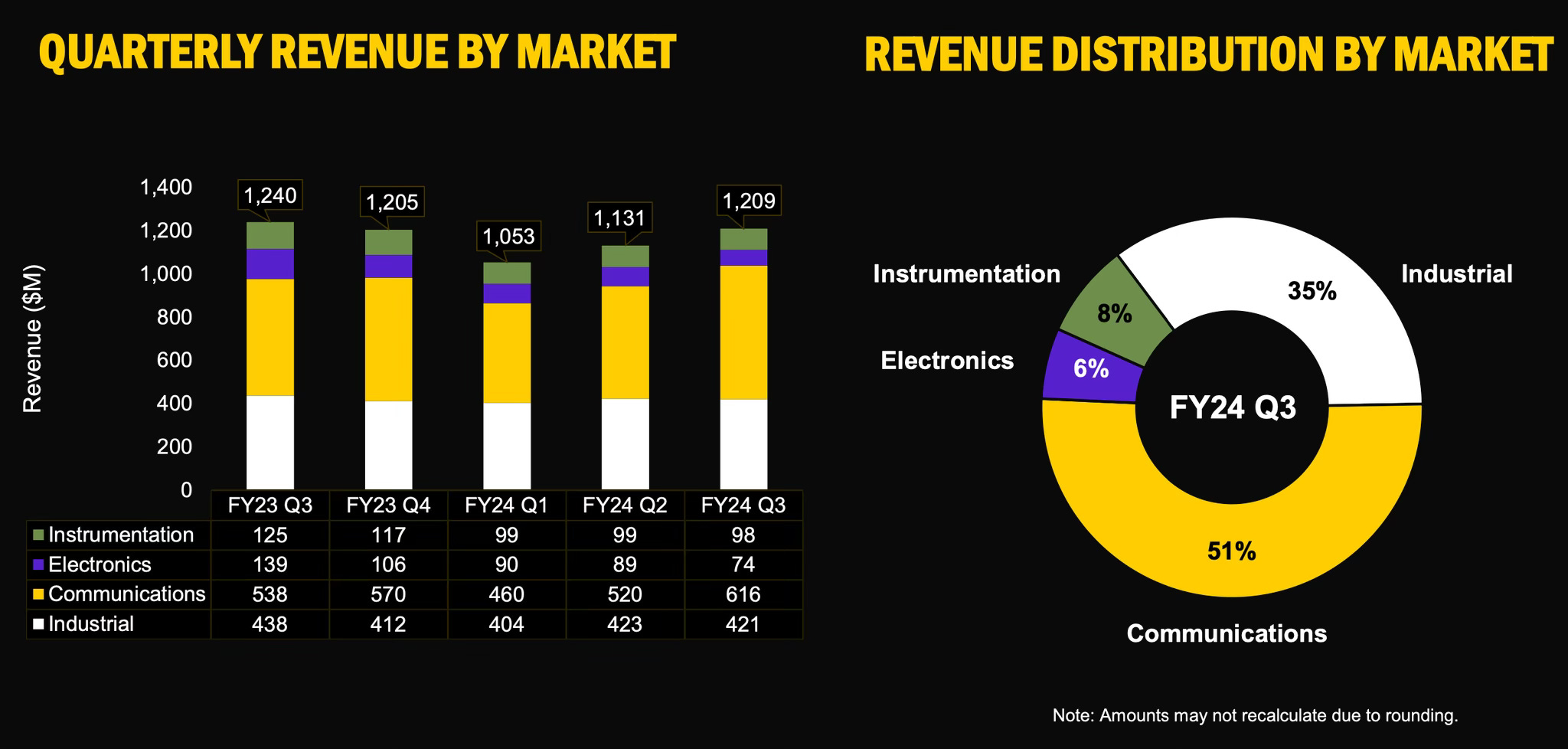

The two markets generating the most revenue are industrial and telecommunications. Industrial revenue is driven by demand for laser systems for EV welding. Laser use in semiconductor and electronics manufacturing also falls under industrial: precision material processing in the semiconductor sector requires lasers to achieve the tolerances needed.

Telecom revenue growth is driven by demand for 800G and higher transceivers for data centers serving AI applications and cloud computing. AI development is pushing humanity to a new technological level, and new technologies require more speed. According to Coherent management’s forecast, the dominant data transmission standard over the next five years will be 800G/1.6T.

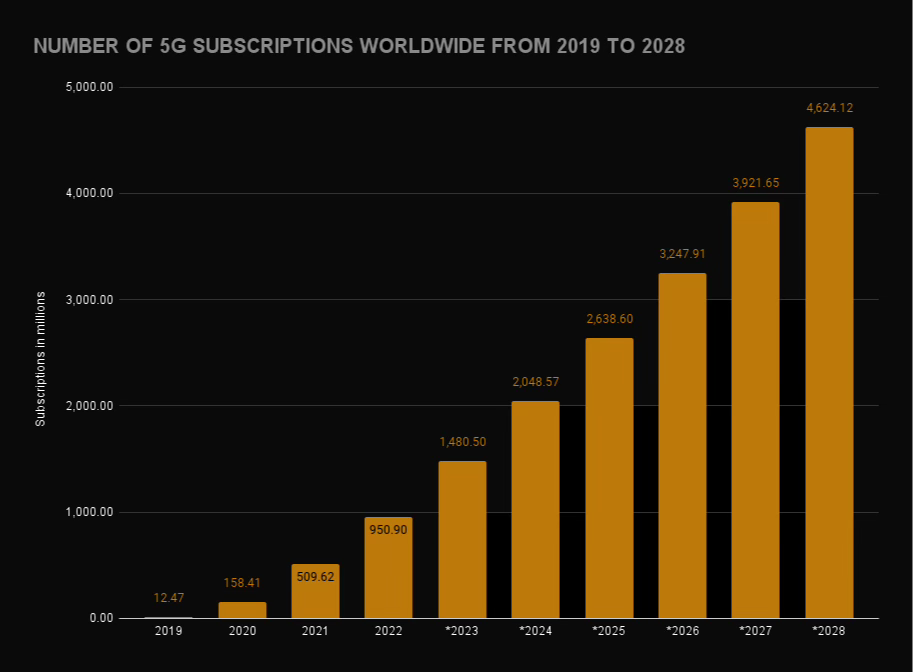

Companies are progressively migrating to fiber optic links to increase bandwidth. 5G network expansion also requires large quantities of optical components and high-speed transceivers. Based on current projections, 5G adoption will continue growing for the next five years, which will support revenue growth.

Coherent Corp. operates across multiple continents, and there is a geopolitical risk from China. A trade war could partially reduce the company’s earnings, which is worth factoring in when buying the stock. But the broad diversification of production and supply chains may allow the company to weather such challenges.

Valuation

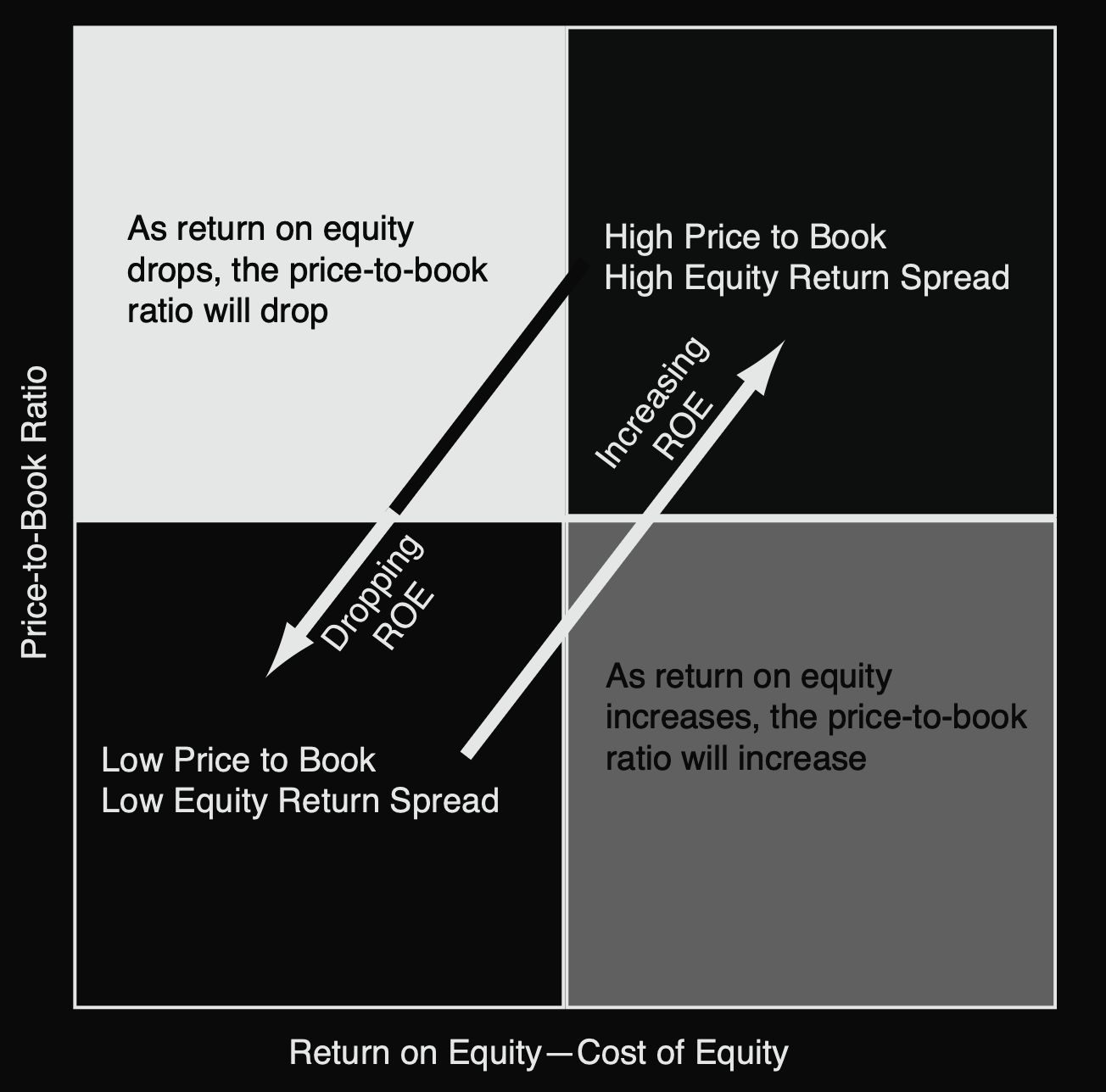

Tracking the Return on Equity and Price-to-Book multiple together is one of the core principles of financial analysis and stock valuation.

Return on Equity measures the profitability of equity capital, specifically how efficiently a company uses its capital to generate earnings.

Price-to-Book compares the market value of a company to its book value, meaning the amount shareholders would theoretically receive in a liquidation after all assets are sold and all debts paid.

Low ROE and low P/B points to problems: a company that uses its capital inefficiently, trading below book value. High ROE and high P/B indicates a successful company with efficient capital use, reflected in a high market valuation.

What conclusions can we draw from the metric trends at Coherent?

ROE is negative as of Q2’24, but it is higher than in the prior quarters (Q4’23 and Q1’24). Negative ROE means the company is running losses and carries a high debt load. Both are true, but they are driven primarily by investment in the business.

Price-to-Book stands at 1.73, below the IT sector average of 3.18 and below the industry average of 2.92. Relative to both benchmarks, the company is priced at roughly half. P/B has also been rising for three consecutive quarters.

Net income: over the last four quarters, the company has been rapidly climbing out of losses on the back of revenue growth and operating income tied to...

Net debt: debt has been declining steadily for seven consecutive quarters. In the most recent quarter, the company paid down $58M of debt and refinanced its $2.4B credit facility, cutting the interest rate by 0.25%, saving $9M per year. As a result of these improvements in earnings and debt, Moody’s upgraded the company’s credit rating to Ba2, reinforcing expectations of further financial improvement.

Based on the matrix framework described above, further improvement in the Price-to-Book and Return on Equity metrics should be expected.

Most Recent Shareholder Call

Coherent Corp. reported strong results for Q3 of fiscal year 2024 (the company’s fiscal year differs from the calendar year), supported by strong positions across several key market segments. While 800G transceiver demand for data centers and AI applications was the primary growth driver, the company is demonstrating technological leadership across a broader range of areas.

In the 800G/1.6T transceiver segment, Coherent continues to grow revenue and expand its customer base. The company also announced progress in developing 200mm silicon carbide wafers to meet growing demand. Executive VP Sohail Khan noted that the company “is shipping engineering samples to several customers, and the feedback from them is very good.”

In the materials segment, a new optical circuit switch (OCS) based on liquid crystal technology was announced, potentially opening new growth opportunities. Chief Technology Officer Julie Sheridan Eng noted that Coherent is already in sample supply discussions with many customers.

In lasers and photonics, CTO Julie Sheridan Eng highlighted the company’s advantages in developing VCSEL, EML, and silicon photonics technologies for the next generation of 1.6T/3.2T transceivers.

In telecom, despite a slower-than-expected overall market recovery, Coherent sees growth opportunity in China and in the digital coherent optics module market through its differentiated products.

On the financial side, Coherent raised its full-year revenue and earnings guidance to $4.62-4.70B and non-GAAP EPS to $1.56-1.73, supported by business diversification. Temporary margin headwinds have been resolved or are in the process of being addressed.

Operating cash flow remains strong at $117M for the quarter. Temporary gross profit headwinds from manufacturing issues have been resolved.

As CEO Chuck Mattera summarized: “We have 300 years of experience in our management team. We will show investors the depth of our technology, our markets, and the business as a whole. The best is yet to come.” He is probably right.

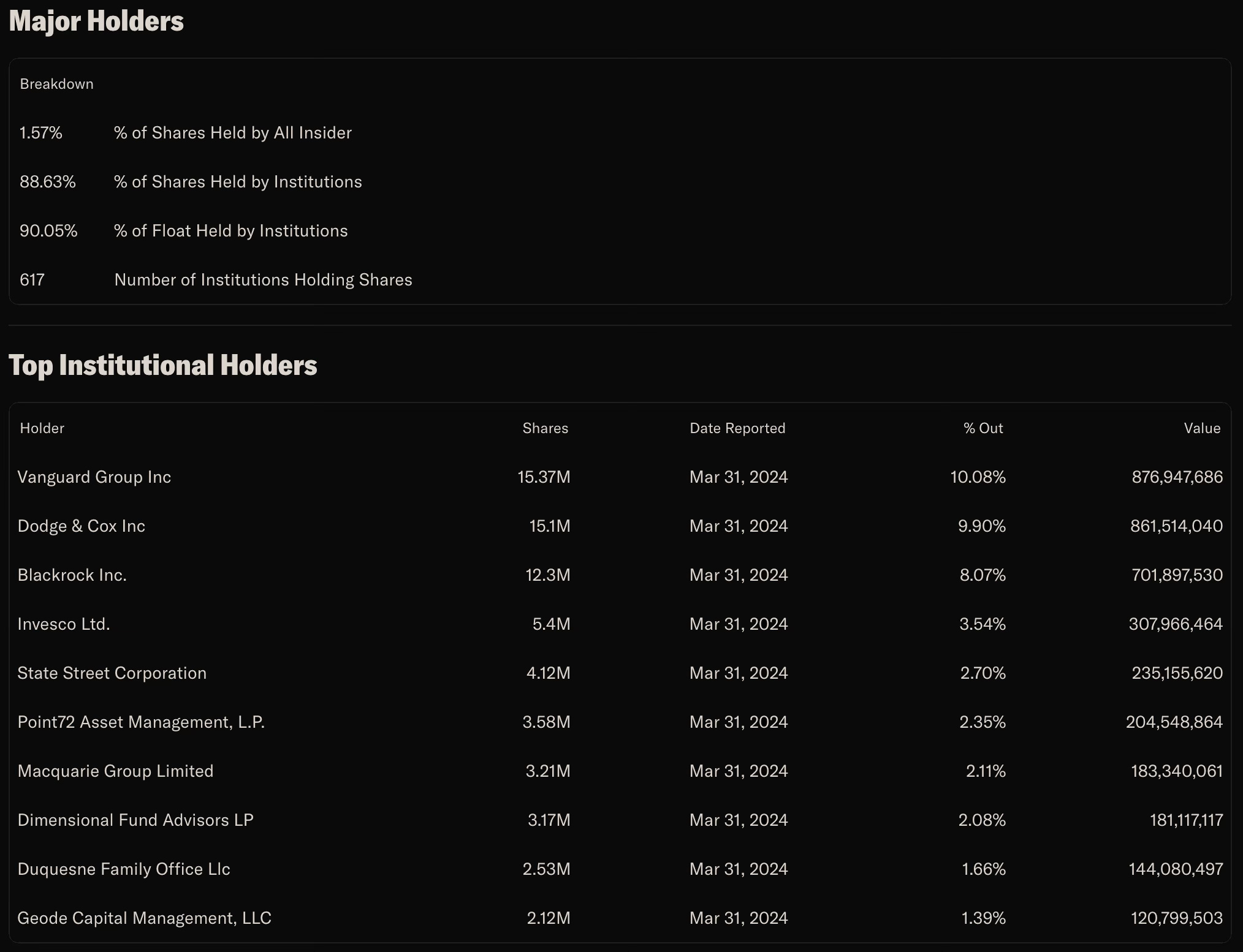

Shareholders

Insider ownership stands at just 1.57%, with the controlling interest in the hands of outside investors. Institutional interest is high: 88.63% of all shares are held by institutions. The largest positions belong to Vanguard Group Inc. (10.08%), Dodge & Cox Inc. (9.90%), and BlackRock Inc. (8.07%). Also worth noting is Stanley Druckenmiller’s fund, Duquesne Family Office LLC, which holds 1.66% of the company, representing 3.5% of his portfolio.

Conclusion

Coherent is a multi-layered company with broad product diversification. The first thing I see in Coherent’s outlook is growth in the customer base for 800G transceiver sales, driven by AI/ML scaling. The second is growth in telecom equipment sales for 5G, as that technology continues to expand.

There is also a large volume of products tied to automotive, computers, and portable devices. But those will likely lag due to elevated inflation and interest rates. Consumers may simply cut back on new gadgets and electronics, which would weigh on sales of those components. However, these factors may ultimately have limited impact on overall revenues given the company’s diversified business lines.

Declining debt, gradually improving earnings, positive guidance from management, high analyst ratings, and a company priced well below fair value: compelling arguments for a medium-term buy.