Coupang, Inc.

In March 2021, the company completed its IPO on the NYSE. Post-IPO market cap exceeded $60B.

Coupang, Inc. is South Korea’s largest e-commerce company. Founded in 2010, headquartered in Seoul. The company has built its own logistics network for fast, convenient delivery.

Business and services:

Coupang.com online platform: a marketplace covering everything from electronics to groceries and apparel.

Rocket Delivery: express delivery within hours across South Korea.

Network of fulfillment centers and IT infrastructure for operational optimization.

Financial services: payment solutions, credit cards.

Subscription services: grocery delivery, video streaming, and more.

The largest competitors are American e-commerce giants with enormous resources and technology. All three already have some presence and operations in Asia: Amazon, Walmart, eBay.

Outside of eBay, their regional footprint is fragmented. Competition from the American giants will only intensify as they expand. For now, Coupang remains the dominant player in the South Korean domestic market. Local Korean competitors are also worth factoring in: SK Telecom, GS Retail, CJ Logistics.

The company publishes quarterly investor updates with financial statements and shareholder conference calls.

Annual Financial Review

Revenue grew from $11.97B in 2020 to $20.58B in 2022 (+72%), reflecting an expanding customer base and higher average order values as the company broadened its product range and services. Growth rates significantly outpace the market. Gross profit expanded from $1.99B to $4.71B (+137%) over the same period, indicating that the business is becoming more efficient: the company extracts more gross profit from each dollar of revenue. Scale and logistics cost optimization are contributing.

Operating income saw a sharp deterioration from 2020 to 2021 (from -$516M to -$1.2B), driven by heavy investment in business expansion: food delivery, marketing, engineering, and global expansion. Investments were scaled back in 2022. Pre-tax loss spiked from -$463M in 2020 to -$1.54B in 2021, a direct consequence of the surge in operating expenses from those investments. By 2022, the loss was reduced to -$93M following cost optimization. Net loss followed the same pattern: losses multiplied in 2021 to -$1.54B, reflecting the deliberate prioritization of investment over profitability. In 2022, net loss was brought down to -$92M. EBITDA showed a similar spike to -$996M in 2021 due to accelerating operating expenses. By 2022, Coupang refocused on efficiency and cost discipline, significantly narrowing both the operating loss and EBITDA.

In FY2021, Coupang posted strong revenue growth alongside a substantial deterioration in profitability and negative EBITDA.

In the first half of 2021, the company prioritized business scaling and revenue growth at the expense of efficiency and operating profitability. In the second half, it ran into labor shortages and a sharp demand drop tied to COVID outbreaks. Emergency capacity expansion proved costly and hit earnings hard. COVID-related expenses (staff bonuses, protective equipment, additional hiring) added roughly $130M in costs in Q4 2021 alone. A high share of investment went into startups like the food delivery service Coupang Eats, which were loss-making at the time. Logistics infrastructure expansion (warehouses, etc.) outpaced the growth of the business itself, reducing capacity utilization.

In effect, a COVID-19 outbreak coincided with active business scaling, and profitability paid the price. The company’s losses hit investors hard, falling well short of their expectations. For many, the logical move was to exit, given that a recovery to prior results could take a very long time, or might not come at all.

Balance Sheet

Assets grew from $5.07B to $9.51B, reflecting active investment activity and expansion of the business and infrastructure. Liabilities increased from $5.67B to $7.10B: the company is actively raising debt to fund growth. Liabilities as a share of total funding stand at 75%, which is high. Equity was turned from -$4.07B in 2020 to $2.41B in 2022, a shift largely driven by the IPO and roughly $4.6B raised from investors in 2021. Total debt increased modestly from $2.23B in 2020 to $2.4B in 2022, indicating continued active investment, though the pace of debt growth has slowed relative to 2020. Net debt flipped from positive to negative, moving from $837.72M in 2020 to -$1.28B in 2022. A positive trend: the company grew its liquidity and assets considerably faster than its debt load.

Cash Flows

Operating cash flow was positive in 2022 at $565.44M. A good sign: the core business is now generating more cash than it consumes. Investing cash flow came in at -$848.25M in 2022, showing that Coupang continues to invest actively in infrastructure and growth. Expected for a fast-growing company. Financing cash flow contracted from $3.58B in 2021 (IPO effect) to $247.35M in 2022, meaning the company relied less on external financing during the year. Free cash flow outflow in 2022 was -$258.82M, not a critical level given the scale of Coupang’s investments in future growth, and a marked improvement from -$1.08B in 2021.

Quarterly Financial Review

Income Statement

Revenue grew from $5.8B in Q1 to $6.18B in Q3 (+6.6%). Steady growth driven by an expanding product and services offering and a growing customer base. Pace outperforms the market. Gross profit grew from $1.42B to $1.57B (+10.6%), growing faster than revenue and pointing to improving operational efficiency. Gross margins expanded from 24.5% to 25.4%.

Operating income ran from $107M in Q1 to $147M in Q2, then pulled back to $87M in Q3. Positive trajectory versus Q1, with some softening in Q3 relative to Q2. Overall the data shows improving operating results versus the start of the year, driven by cost optimization and scaling of high-margin segments such as advertising. Q3 saw a modest slowdown due to investment in new initiatives. Relative to 2022, the trend is clearly positive. The Q2 profit increase was driven by a $100M quarter-on-quarter jump in gross profit against contained operating expense growth (only +$41M). In Q3, both effects were weaker: gross profit added $50M quarter-on-quarter while operating expenses rose $60M.

EBITDA declined from $255M in Q1 to $155M in Q3 as investment in business development increased. It remains in positive territory, providing room to fund further expansion. The overall picture is steady revenue and margin growth on the back of an expanding customer base, with Coupang continuing to invest in development, which is temporarily weighing on EBITDA.

Balance Sheet

Total assets show steady growth from $9.71B to $11.56B, a positive indicator reflecting business expansion. Liabilities are also rising ($7.15B in Q1 vs. $8.63B in Q3), which is consistent with asset growth. A slight acceleration in liability growth may indicate active use of debt financing. Equity shows positive momentum, increasing from $2.56B to $2.93B, driven by three consecutive quarters of net income. Another positive factor. Total debt is growing in absolute terms. Net debt (after deducting short-term investments and cash), however, is declining and moving into negative territory: the company carries no net debt position.

Cash Flows

Operating cash flow showed positive momentum in Q2 versus Q1 (up 59.5%), reflecting higher receipts from core operations. Q3 then saw a 9.6% decline versus Q2, pointing to temporary friction in sales and other operations. Investing cash flow remained negative throughout, with expenditures exceeding inflows. The largest outflow was in Q2, reflecting heavy investment, partly financed by debt. In Q3, the outflow contracted 63.7% versus Q2. Financing cash flow rose 214.5% in Q2 versus Q1, indicating active borrowing during the quarter, then fell 85.8% in Q3 as new borrowing slowed. Despite the pullback in operating and financing cash flows in Q3, free cash flow grew solidly: up 23.3% in Q3 versus Q2. The company has a reasonably strong liquidity buffer.

Multiples

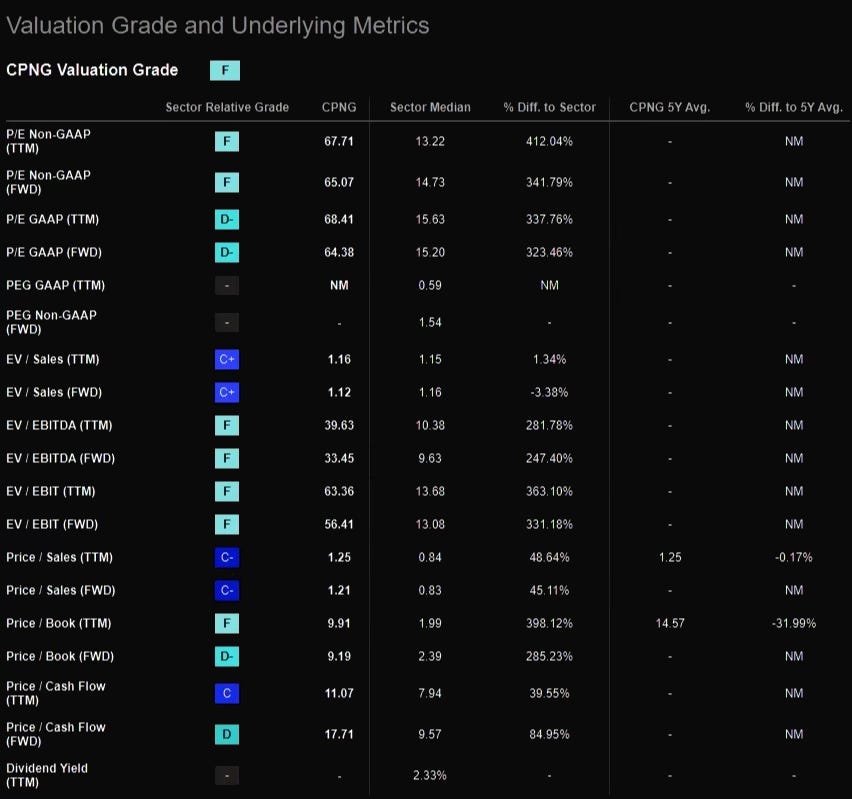

Valuation and Key Metrics

Coupang’s valuation multiples show the stock trading at a premium to sector averages.

P/E (TTM and FWD) is roughly 4-5 times above sector medians. Investors are willing to pay up, pricing in strong future earnings growth. EV/EBITDA (TTM and FWD) likewise shows a large premium to the sector: the market is paying a significant multiple for Coupang’s growing operating earnings. Price/Book (TTM and FWD) is nearly 5 times the sector median, indicating that investors place a high value on the company’s intangible assets and growth potential.

The picture is one of strongly optimistic market expectations and a willingness to pay a substantial premium for exposure to Coupang.

Growth Rate and Key Metrics

Revenue Growth (YoY)

Revenue Growth (YoY): Coupang’s revenue is growing 13.85-13.80% year-over-year, roughly 3 times faster than sector medians. This points to strong demand and business momentum.

CapEx Growth (YoY): Capital expenditure growth fell 10.07% year-over-year, while the sector average shows 8.10% growth. Declining capex in consumer sectors typically raises flags for investors. Here it may indicate that Coupang has eased off expansion investment after an active growth phase.

Coupang is posting strong revenue growth alongside slowing investment. On one hand, a positive sign: the company is focused on monetizing existing demand. On the other, sustainable long-term growth will require continued infrastructure investment, which could weigh on profitability again down the road.

Q3 2023 Earnings Call

Positive

Key metrics continue to grow: revenue, gross profit, active users. Growth rates are accelerating versus prior quarters. Active user growth in Q3 was 14%, versus 10% in Q2 and 5% in Q1. Product assortment is expanding, which is feeding through positively to the company’s key metrics. Developing segments are gaining momentum, including food delivery via Eats and the new Taiwan market. Eats, for example, has reached a 20% share of the food delivery market. The company is generating record cash flows: $2.6B in operating cash flow in Q3. Management is confident in achieving the long-term EBITDA margin target of above 10%.

Negative

Adjusted EPS came in at $0.05, missing analyst estimates by $0.02. The company fell short of net income forecasts. Gross profit in the Product Commerce segment declined versus the prior quarter, indicating margin pressure in the core business. Losses in the Developing Offerings segment widened to $161M from $91M a year earlier, reflecting significantly higher investment in new business lines. Adjusted EBITDA declined for the total business, though management expects improvement ahead. Margin pressure from product and service assortment expansion. These near-term headwinds may continue to weigh on profitability.

Based on the earnings call transcript, Coupang’s results look promising, and I see no reason to sell the stock at this point (if you’re holding it). The company is delivering consistent growth across key metrics and strengthening its competitive position. The earnings call revealed that the Taiwan expansion is producing encouraging results and the market reception has been positive. Coupang noted that its app became the most downloaded in Taiwan in 2023. Good news for investors. Management also indicated readiness to cut investments that are underperforming expectations: “We are disciplined about capital allocation. We start with small investments, then test and iterate carefully. We invest more capital over time into opportunities with the best long-term cash flow potential. Within our international initiatives, we closed our operations in Japan, where we were not generating the returns we had hoped for. In contrast, we like what we see in Taiwan, which is showing the same signs of transformative potential that we saw in Korea when we launched Rocket Delivery.” That kind of discipline inspires confidence.

Risks

Macro risks: economic slowdown in Korea or Taiwan, reduced consumer spending; rising inflation and interest rates constraining demand and profitability.

Competition: intensifying pressure from local or international players.

Operational risks: supply chain and logistics disruptions (e.g., pandemics); challenges scaling into new markets (Taiwan).

Geopolitical risks: deterioration in North-South Korea relations, renewed conflict; military provocations and threats from North Korea; escalating tensions around Taiwan, invasion risk. Relevant given that Coupang is actively expanding into these regions.

These risks exist everywhere, in every company. None of them should be ignored: each has a direct bearing on the company’s financial performance.

Shareholders

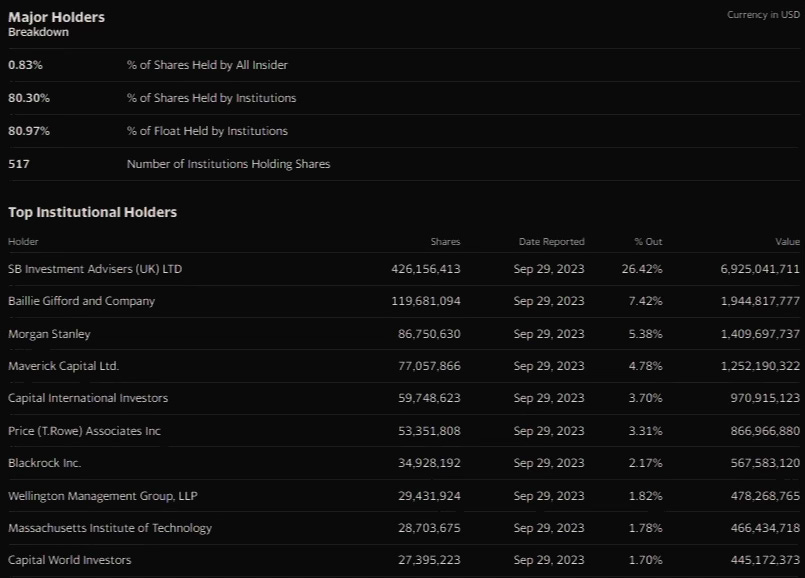

The majority of shares (80.97%) are held by institutional investors, a signal that the company is attractive to large investment funds and other institutional players.

The largest holder is SB Investment Advisers (UK) LTD with 26.42% of all shares. This entity holds significant influence and control over the business. Detailed information on SB Investment Advisers (UK) LTD is limited. It likely represents large investors, possibly institutional or high-net-worth individuals.

Other major holders include investment and asset management firms from the US and UK, indicating broad global institutional interest.

Insider and management ownership stands at just 0.83%, meaning control and governance are effectively in the hands of outside investors.

The ownership structure reflects strong institutional conviction alongside minimal management and controlling-party ownership. The key beneficiary is the opaque SB Investment Advisers.

Conclusion

Coupang is showing signs of improving fundamentals. Its near-term strategy is centered on expanding the customer base and improving profitability while maintaining a focus on high service quality. Coupang stands out in South Korea’s competitive e-commerce market through its innovative logistics network and rapid delivery capability. The company is also benefiting from its advertising business, which is growing strongly with high operating margin potential.

Consistently growing active customer counts and sustained revenue growth, despite periodic fluctuations, point to continued expansion. The outlook in South Korea and Taiwan looks promising, supported by management’s commitment to service quality and ongoing innovation.

An additional argument for Coupang: the company is a top-2 holding for Stanley Druckenmiller, whose fund has averaged roughly 30% annual returns over many years. His current position represents 13% of his portfolio. The company also ranks 13th in the Bill and Melinda Gates Foundation portfolio at 0.4%.

Despite a difficult global economic environment, Coupang’s position is strong: a solid cash cushion, no net debt, reputable investors, and gradually improving revenue and earnings. All of this makes the company an attractive candidate for long-term investment.