Intellia Therapeutics, Inc.

The company was among the first to apply CRISPR technology directly in humans to treat disease.

Intellia Therapeutics, Inc. is an American biotechnology company working on genomic editing methods, including CRISPR-Cas9. In practice: modifying genes in patients to treat various diseases. That covers correcting mutations responsible for inherited disorders, as well as developing new approaches to cancer and other conditions through genetic material editing.

Core areas of work at Intellia:

In vivo gene editing to treat hereditary diseases caused by single-gene mutations, including Huntington’s disease (brain cell death) and hemophilia (clotting deficiency). The company is running clinical trials for these indications. Development of in vivo gene editing technologies inside patient cells to create cell-based therapies, including for oncology and autoimmune diseases.

Building CRISPR delivery systems for precise modification of target cells and tissues. When scientists use CRISPR-Cas9, they need to get the technology inside the relevant cells and tissues. Think of it as transmitting instructions into a cell to make targeted changes in the genetic material. Intellia develops specialized delivery systems and methods to deploy CRISPR-Cas9 accurately at the right locations inside the body, enabling precise gene editing with the intended outcomes.

Development of CRISPR tools capable of making more precise and complex genomic edits, expanding the possibilities of gene therapy.

Lead programs in early clinical development:

NTLA-2001: for treatment of transthyretin amyloidosis (a genetic disease in which a protein accumulates in the body and causes problems in organs including the heart and peripheral nerves).

NTLA-2002: for treatment of hereditary angioedema (swelling of internal or external body tissues).

Key competitors:

The gene editing market is in early stages and marked by intense competition among the main players. As a result, many companies are forced to both collaborate and compete simultaneously.

CRISPR Therapeutics, Regeneron Pharmaceuticals, Editas Medicine, Sangamo Therapeutics, Beam Therapeutics, Precigen, Caribou Biosciences, Verve Therapeutics, Cellectis.

The company publishes a quarterly business update presentation covering all aspects of operations, research directions, and the disease areas it is targeting.

Annual Financials Analysis

Consolidated Statements of Operations and Comprehensive Loss

Revenue was $52.12M in 2022, up 57.69% from 2021 ($33.05M). Growth was driven by increased licensing payments and grants. Gross profit reached $44.55M, up 70.28% from 2021 ($26.16M). Operating loss was $458.16M, widening 71.05% from 2021 ($267.85M). Net loss fell 77.01% year-over-year to $474.19M in 2022. EBITDA came in at -$450.59M, down 72.67% from 2021 ($260.96M).

Intellia carries substantial losses despite gradual revenue growth. The explanation is straightforward: no commercial product has reached the market yet. Revenue comes entirely from partnership agreements and grants. The bulk of expenses goes to R&D and lengthy, costly clinical trials that have not yet received regulatory approval.

Intense competition in genomic editing forces Intellia to maintain high R&D investment to preserve its lead. The company has not yet reached the scale needed to reduce costs and turn profitable.

At this stage, Intellia’s losses are natural and normal for a developing biotech company, especially considering that most of the healthcare sector runs at a loss. The path to profitability runs through the commercialization of its pipeline.

Consolidated Balance Sheets

Total liabilities grew from $254.22M in 2021 to $284.53M in 2022, largely reflecting expanded business operations. Equity rose from $1.04B to $1.24B, indicating growth in the company’s value. Net debt is negative: cash and short-term investments substantially exceed total debt. Headcount increased from 485 in 2021 to 598 in 2022.

Intellia is growing actively despite current losses. The significant increase in total liabilities reflects higher investment in R&D and expanded clinical trials. The company is scaling its operations in genomic editing.

At the same time, equity is rising despite negative net income. This signals increasing market value: investors are pricing in the potential of Intellia’s CRISPR pipeline and patents.

With substantial cash on hand and low debt, the company is in a stable financial position to continue expanding. The headcount increase confirms this, reflecting a growing scientific workforce in genomic editing.

Consolidated Statements of Cash Flows

Operating cash flow declined from -$215.93M in 2021 to -$323.40M in 2022. Investing cash flow improved from -$550.78M to $160.31M. Financing cash flow shifted to an outflow, down 21.24% ($573.07M). Free cash flow declined from -$228.68M in 2021 to -$336.96M in 2022.

Cash movements in 2022 showed a significant net outflow, driven by ongoing business losses against the backdrop of active expansion and investment.

Negative operating cash flow widened as growing losses required more cash to sustain operations. Investing inflows improved because Intellia deployed less capital into acquisitions and recovered more from financial investments during the year.

The character of financing cash flow also shifted: instead of raising capital through equity issuance, the company directed cash toward liability repayment.

Free cash flow contracted substantially. Liquidity nonetheless remains sufficient to sustain investment and business development in the medium term.

Quarterly Financial Review

Consolidated Statements of Operations and Comprehensive Loss

Revenue in Q2 2023 grew 7.84% versus Q1 ($13.59M). This reflects incoming payments from partners under licensing agreements, as well as government development grants. Gross profit grew 8.22% quarter-over-quarter versus Q1 ($11.42M), indicating effective cost control. Operating loss remained negative in Q2 2023, deepening 18.2% to -$132.33M, driven by increased investment in scientific development tied to an expanding clinical research portfolio. Net loss widened 19.93% in Q2 2023 to -$123.68M due to additional hedging expenses and equity-based employee compensation. EBITDA declined 18.43% in Q2 2023 to -$130.16M, reflecting sustained high operating expenses.

Consolidated Balance Sheets

Total liabilities fell 3.83% in Q2 2023 (from $227.05M to $218.35M), driven by a reduction in accounts payable and other short-term obligations. Equity also declined 7.22% in Q2 2023, a consequence of the net loss recorded in Q1 2023. Net debt remains negative, which is a positive indicator: cash and equivalents exceed total debt by a significant margin.

Even with the equity contraction, Intellia’s current financial position can be assessed as stable, given the controlled debt load. For the company, that is what matters.

Consolidated Statements of Cash Flows

Operating cash flow in Q2 2023 improved 17.52% to -$86.53M from Q1 (-$104.91M), but remains negative, reflecting the company’s continued losses from product development spending. Investing cash flow increased 71.75% but remains negative at -$34.54M for the quarter, indicating optimized capital expenditures in the current period. Financing cash flowin Q2 2023 improved 41.75% (-$1.28M) versus the prior quarter, reflecting additional financing raised. Free cash flowimproved from -$108.74M to -$90.83M in Q2 2023. Negative free cash flow means the company is spending more than it earns. For fast-growing innovative companies like Intellia Therapeutics, reinvesting proceeds into development is standard practice. Intellia is investing in innovation, manufacturing capacity, and clinical trials for its genomic editing pipeline. These are strategic investments in future growth.

At first glance it seems contradictory that a company with negative free cash flow can carry negative net debt (more cash than debt). It is a perfectly plausible situation. Negative free cash flow means the company is spending more than it earns in the current period, but it may hold accumulated cash from prior periods that exceeds outstanding debt. The company can also borrow against future revenues or assets: this increases debt but does not immediately affect the cash balance. And Intellia receives investor financing, which increases cash without increasing debt.

Risks and Opportunities

Investing in a company like Intellia Therapeutics is a high-risk trade. There is a real possibility of losing more than 50% of an investment in the event of clinical trial failure, and we saw exactly that this year with Mersana (MRSN) and Vir Biotechnology (VIR), both of which lost significant portions of their value after adverse clinical results.

Five key risks, in order of significance:

Clinical development failure. If NTLA-2001 advances through trials and then reports bleeding events, insufficient safety, or insufficient efficacy, the stock will fall sharply. The reverse is equally true.

Regulatory action. The FDA (US) or EMA (EU) is responsible for approving any new drug. Even if a drug clears all clinical trials, approval is not guaranteed. If regulators demand additional data, delay approval, or reject applications, Intellia’s value will drop significantly. An approval, on the other hand, would drive the stock up.

Execution. Manufacturing problems, talent acquisition and retention challenges, budget management failures, or slower-than-expected progress will all weigh on the stock over time. Better or faster execution than expected, and the stock rises.

Commercial risk. Say the FDA approves a drug, and the company misses analyst revenue expectations for it. The stock falls. If an approved drug outperforms expectations, the stock rises.

Dilution. This happens when a company issues additional shares to raise capital, whether through a secondary offering or conversion of convertible bonds. Total share count increases, and each existing shareholder’s ownership stake shrinks.

For example: if the company raises $1B by issuing 10M new shares, a shareholder previously holding 1% (with 100M shares outstanding before the offering) will be diluted to 0.91%.

Dilution is negative for shareholders: lower ownership stake and control, earnings spread across more shares (lower earnings per share), and downward pressure on share price.

That said, dilution can be justified if the capital raised enables the company to build a product that drives growth and ultimately increases shareholder value.

Q2 2023 Earnings Call

Positive

Rapid progress in clinical trials for lead programs NTLA-2001 and NTLA-2002. Pivotal trials expected to begin for both programs in the near term.

Strong physician and patient interest in NTLA-2002 for hereditary angioedema. Phase 2 trial fully enrolled.

Encouraging preliminary efficacy and safety data for both NTLA-2001 and NTLA-2002.

Strong balance sheet with cash exceeding $1B, providing more than two years of runway.

Diverse clinical portfolio and promising CRISPR-based pipeline candidates. Significant potential patient population for NTLA-2001 and NTLA-2002 upon approval (hundreds of thousands of patients). Active engagement from leading medical centers in Intellia’s trials.

Negative

No approved products on the market. The company is running at a loss, as it remains in early-stage development.

Additional reproductive animal studies required for NTLA-2002 per FDA request. This may slow development somewhat.

NTLA-2001 for ATTR-CM is currently behind competitors already in trials. Large, lengthy, and expensive Phase 3 trials will be required for approval of key programs.

High operating expenses and rapid cash consumption will require additional financing in the future.

Competition in gene editing therapeutics will intensify. Risk of trial failure and failure to obtain regulatory approval for key programs. Uncertainty around the commercial potential and pricing of experimental drugs.

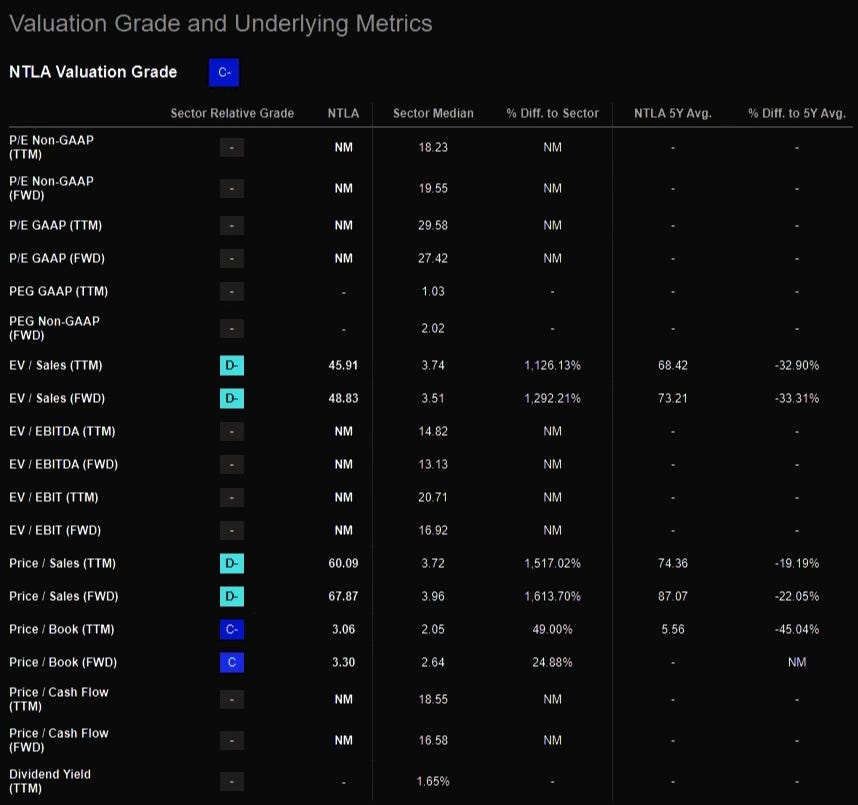

Valuation and Key Metrics

Many metrics are absent and Price/Sales and EV/Sales are very low: Intellia has no meaningful sales yet. The company is in early-stage drug development with nothing on the market. That is why both ratios are minimal. The company’s core value lies in its intellectual property and pipeline candidates, which generate no revenue at present. High R&D spending and long drug development timelines in the industry suppress the current valuation.

As Intellia’s drugs move toward commercialization and begin generating meaningful sales, Price/Sales and EV/Sales should expand to reflect that potential. At this stage, the low readings are entirely explained by the business model.

The metric that deserves more attention is Price/Book.

Current (TTM) Price/Book is 3.06, above the sector median of 2.05. The market is pricing Intellia’s shares at a higher premium to book value than sector peers. Forward Price/Book is 3.30, also above the sector median of 2.64. Investors may be pricing in continued appreciation relative to book value.

High P/B multiples can be justified for fast-growing innovative companies whose primary value sits in intangible assets (R&D), which barely register on a balance sheet.

Growth Rate and Key Metrics

Many metrics are again absent due to the company’s losses. With negative earnings figures, most multiples simply cannot be calculated.

For the metrics that are available:

Revenue growth is significantly ahead of the sector median, both in the trailing year (YoY) and in forward estimates (FWD), reflecting rapid business expansion. Working capital growth is positive, against a sector-wide decline, indicating the company is building inventory and receivables in anticipation of higher future sales. CapEx growth is running well above the sector median, showing that Intellia is actively investing in manufacturing and development to expand the business.

Taken together, the data shows Intellia growing dynamically and outpacing peers. The company is investing aggressively in its future. That is not a negative.

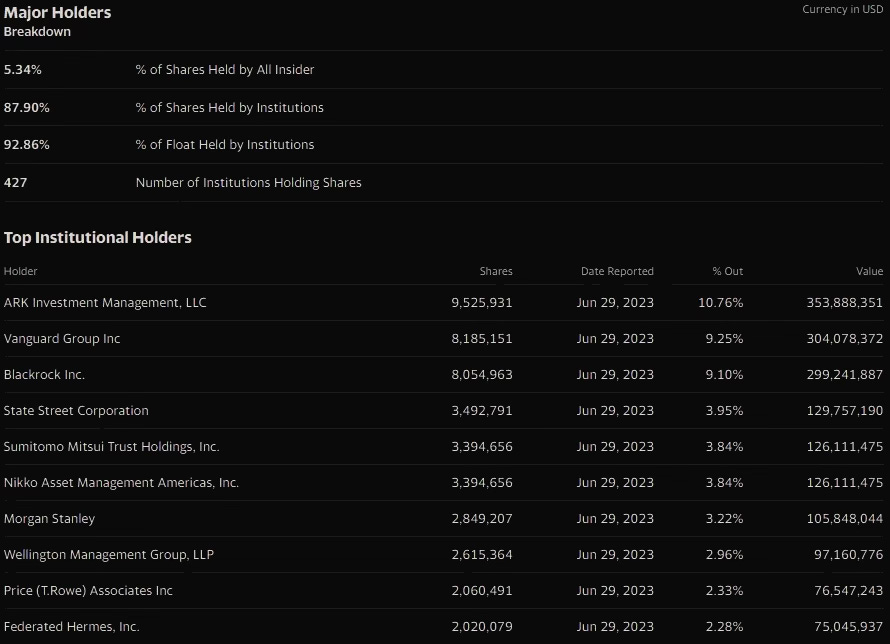

Shareholders

5.34% of shares are held by insiders (executives and employees). A relatively low figure: insiders control only a small fraction of the equity. 87.9% is held by institutional investors, large investment companies and funds. That is a high level of institutional ownership. 92.86% of the float is held by institutions, leaving only a small portion of freely traded shares in the hands of retail investors.

427 institutional investors hold Intellia shares, signaling broad interest from major market players.

The largest holders are ARK Invest (10.76%), The Vanguard Group (9.25%), and BlackRock (9.1%). Together they control nearly 30% of the equity.

Intellia’s shareholder base is dominated by institutional investors: a sign of strong conviction from major market players. Retail investors play a minor role. A rhetorical question: would players like ARK Investment be putting money in if they saw no future here?

Conclusion

Intellia Therapeutics is already showing promising clinical trial results for NTLA-2001 and NTLA-2002 in rare genetic diseases. Scientists and management expect to begin the pivotal trial phase in the near term, which could ultimately lead to regulatory approval and broad commercial use. If the FDA approves, new prospects open up for both the company and the gene editing market.

From a financial standpoint, the company looks reasonably stable. Cash exceeds $1B and debt is low. Intellia is running at a loss, but growing and scaling actively. That is normal for a developing biotech company.

One more point: Intellia shares are currently trading above book value (Price/Book). Investors see growth potential ahead.

And finally, the majority of Intellia shares are held by large investment funds and institutional investors. Another signal of professional confidence in the company’s prospects.

Despite the high risks inherent to the biotech sector, Intellia shares look like a compelling long-term opportunity. Close monitoring of clinical trial results and financial metrics is required.

I view Intellia Therapeutics as one of the top buy candidates in the healthcare sector in a recession scenario.