New Attack Vectors

“I’m not sure what comes next. In my 35 years in cybersecurity, this is the first time I can’t say what will happen next.” — Paul Chichester, Director of Operations at the UK’s NCSC

When someone who has tracked state cyber threats for thirty years, and who usually knows the answer before the question is asked, walks onto the stage at Excel London and admits he doesn’t understand where the industry is heading, it shows you the force of the current challenges. In the past, cybersecurity always came down to two or three key variables: technological maturity, threats, and the behavior of states, behavior you could model. Today there are too many variables, and none of them predicts well.

Chichester opened the session by holding up Morrie Gasser’s book, “Building a Secure Computer System,” written in 1988. It lays out clear technical principles and concrete instructions for building secure systems, from architecture to role-based security. These were ready solutions that could potentially have been implemented. Forty years ago, specialists already knew exactly how to build a secure system. Which leads to Chichester’s logical question: “Why didn’t we do it?” The problem isn’t a lack of knowledge or technology. The industry just doesn’t apply it. Companies bolt security on after the fact, once the product is already built, instead of designing it into the architecture from the start, which leaves security flimsy and awkward. Protective measures are so cumbersome that they complicate users’ everyday tasks, so people work around them or switch them off. Systems throw false alarms too often, which trains teams to ignore real threats or waste time checking harmless events. Meanwhile most vulnerabilities come from employee mistakes such as weak passwords, phishing, or misconfiguration, not from technical flaws in the software. In practice, vendors take old solutions, change the name and the marketing, but don’t solve the fundamental problems, reselling the same product under a new label. Nobody builds a secure system because of recurring organizational and cultural problems, not because of a technology shortage. Until today’s threats, companies had no motivation to solve the fundamental problems, because the current system makes money. If they actually built secure systems from the foundation up, it could reshape the market and cut repeat sales. So the industry is stuck in a cycle.

This is probably the frame to view the entire conference through. All the technical talk this June about agentic AI, supply chain security, and machine identities are attempts to make up for forty years of inaction, now that defenders have no more than 24 hours to react and attackers have an army of autonomous AI agents.

Why operations will break

Shlomo Kramer, founder of Check Point, Imperva, and Cato Networks and an early investor in Palo Alto Networks, voiced one of the central problems. He said new AI models won’t change the nature of cyberattacks. The vulnerabilities stay the same, the attack techniques don’t change either, but the speed changes: attacks become ten to a hundred times faster. That speed will break every company’s operational processes.

He gave a mundane example. A company has 5,000 stores across Europe, each with a physical network gateway. The vendor sends out a security update. How many weeks, or even months, will it take to roll that update out to all 5,000 locations? Now imagine that models like Mythos can already generate a working exploit within tens of minutes of a vulnerability being published, and that updates have to be released several times a day. This isn’t a question of comfort, it’s a question of survival for an entire device category. So companies that sell physical boxes for offices, stores, and warehouses will be in the worst position. Their customers will soon realize there’s no sense in buying 5,000 boxes when you can take a cloud service that patches in one place in minutes instead of weeks. The classic network players who were late to the cloud will suffer the most. This is an important point that can protect investors from bad bets.

The second point is that the CISO budget in 2026-2027 won’t grow, because money inside the IT budget is flowing toward AI. Companies are deciding to invest in AI projects (automation, generative models, agentic systems), and no separate additional line item will appear for security. The money comes out of the same general IT spend, just redistributed in favor of AI.

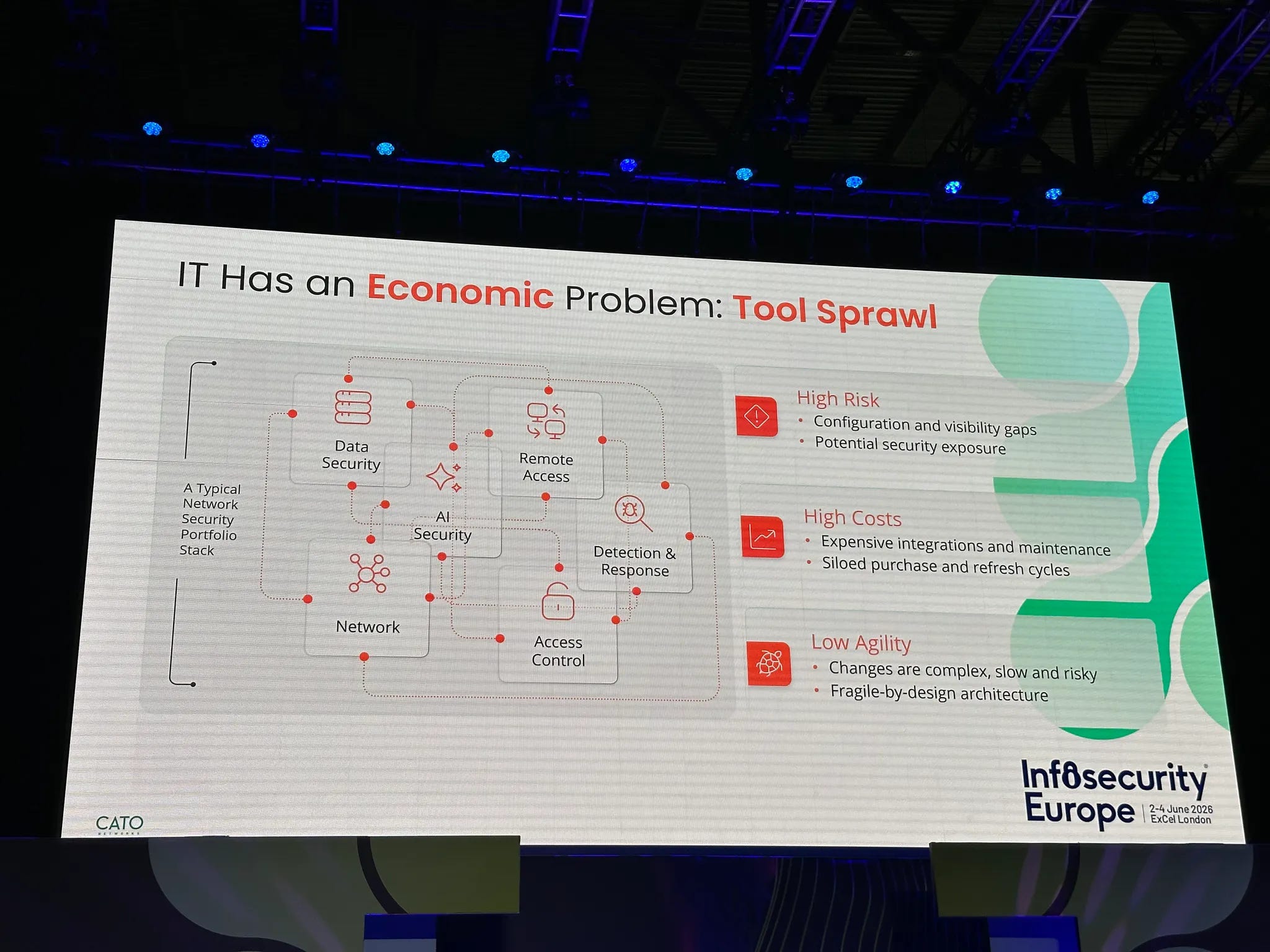

This creates hard pressure on the CISO. They have a fixed budget, but threats keep multiplying and attack speed climbs by tens of times. At the same time, most companies now run five different security platforms, each generating a thousand alerts a day. The security team drowns in those alerts, with no sense of what to prioritize.

Consolidation may become the only way to survive these conditions. By that I mean a single platform that unifies all security functions and makes decisions in real time. Such a platform has to analyze threats itself, prioritize them, and even respond automatically, because the team simply won’t have time to work through thousands of alerts by hand while the attack cycle compresses to hours. For an investor this means that companies offering consolidated security platforms with AI elements for automated decision-making will gain an advantage. Companies selling point solutions for specific tasks, forcing customers to keep five or six different platforms, will lose the market.

The market has changed

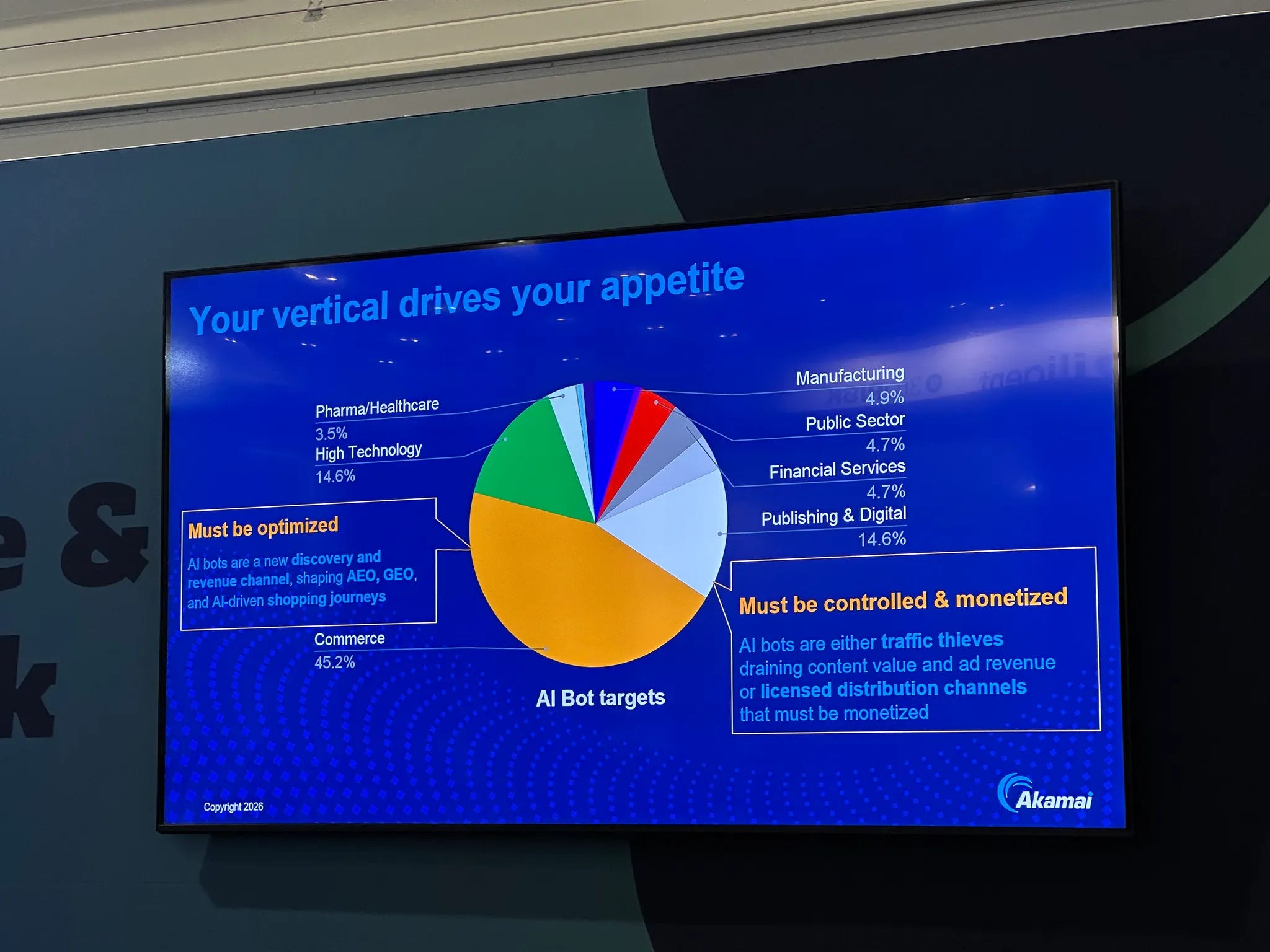

The Akamai session was no less significant for understanding current trends, because AI traffic has already become a separate economy inside the internet, and it’s distributed unevenly. Akamai can see roughly 20-30% of global internet traffic, so their figures are measurements of what’s actually happening on the network. AI requests already run at about a billion and a half per day, growth over the year was 300%, and the traffic itself splits into training data collection, search crawlers, on-demand agents, and user agents.

But who generates this traffic? 45.2% of all AI traffic comes from e-commerce. Online stores no longer see AI as a threat. For them it has become a new sales channel.

If a user used to go to Google, compare ten sites, and make their own decision, now they ask ChatGPT or Claude what to buy and get a ready-made recommendation. The store doesn’t want to block AI bots, it wants to land in their answer first, because this is now the equivalent of SEO (search optimization), only for generative systems. Hence the new acronyms AEO and GEO, meaning answer engine optimization and generative engine optimization. The most interesting part is that this gave me a retrospective on Dan Niles’s recent interview on the Risk Reversal Podcast, where he singled out Google as the leader of this race.

But why Google? Because a person increasingly gets one ready-made answer from AI instead of ten links. In that case the winner isn’t whoever has the better search, it’s whoever controls the point where the answer is delivered and holds the largest data about the user. Google’s position is nearly unique on both. YouTube, Gmail, Maps, Android, Chrome, Photos, Drive, Play, and a whole list of other services with billion-strong audiences. The AI doesn’t need to onboard the user into a separate app, because it shows up where the person already is every day. Every major Google service continuously produces a behavioral signal, registering what a person searches, watches, where they go, what they write, which apps they install, what they buy. This is the basis for a personalization that’s almost impossible to buy elsewhere. On competition, OpenAI or Anthropic can’t buy fifteen or twenty years of a live behavioral trail from millions of people. At the same time, Google can fund this race out of its own cash flow, without diluting capital and without depending on outside creditors. That lets it do what the market has gotten used to over twenty years, namely give away a good answer for free. Here OpenAI is weak, because it’s trying to monetize a subscription in an environment where Google and Meta have trained the consumer to get a quality answer for free. As a result only about 5% of OpenAI’s users pay, and its competitive position in the consumer segment is weak.

So the market may split between those with the stronger position in their segment, not those with the smarter model. Google has the strongest position in consumer, Anthropic has the advantage in enterprise, and OpenAI is being forced to change strategy because the original one didn’t work, monetization or even the prospect of monetization simply isn’t there. That’s why OpenAI began focusing on coding and cutting side projects. But the main problem is that Anthropic is already on this territory. Claude has a reputation as the number one model among developers for quality in coding, Microsoft put $5 billion into Anthropic last fall specifically, and then went on to embed Claude into its products. Microsoft plays a double game, using both OpenAI and Anthropic, and gradually reducing its dependence on each through its own Copilot. So AEO and GEO in the consumer segment will first of all mean optimization for Google’s surfaces. Because mail, maps, Android, YouTube, and search are becoming the new storefront a brand now needs to land in.

For publishers the situation is completely different. For them AI becomes a direct extraction of revenue. A user used to search a topic, click through to a site, read the material, see an ad or sign up, and that’s what created monetization. Now an AI system can take that same content from the site, process it on its own, and hand the user the answer in chat. So the person no longer visits the site, which means the outlet loses the view, the ad, and the chance at a subscription. A stock market story, for example, used to be read by 100,000 people on the publisher’s site, and now a language model can read it and retell it to 100,000 users without a single site visit, in a completely different interpretation. In that case the choice becomes either to close off access to AI bots or to start charging for machine access to the content.

In parallel, it was shown that AI attacks are far from theory. One example was a support chatbot. An employee opens the chat history in their browser, and it already contains malicious HTML/JavaScript that an attacker planted there through a conversation with the bot. This code executes in the employee’s browser and steals an external user’s session keys or tokens, in effect hijacking someone else’s authorized session. Chatbots can no longer be treated as a safe interlocutor, because any user input into them has to be handled just as strictly as input into an ordinary web application. Out of this grew a new product category that Akamai itself sells as a firewall for AI. The idea is to filter the AI system’s input and output, keeping the model from becoming a point of attack. Cloudflare, Datadog, and a dozen startups are building in the same niche.

And finally, the idea most unpleasant for the market: denial of wallet. This is an attack that forces an AI product to burn through its entire purchased volume of OpenAI or Anthropic tokens in just a few hours. The attacker degrades the service and at the same time strikes directly at the product’s economics. AI security for every company now becomes a mandatory expense line, and the one paying for it will probably no longer be the CISO but the product owner and the chief AI officer, because the risk now sits inside the business model.

Microsoft trying to eat the agent security market

“By 2028, large organizations will have billions of agents woven together across apps, data, and workflows.” — Vanessa Anderson, Director CSA / Chief Architect at Microsoft

This line is striking. Microsoft’s presentation on securing agentic AI is interesting precisely for the picture Microsoft is painting for its customers.

Microsoft is building a full product vertical for the cyberattacks of the new era:

Microsoft Entra ID: identity management, including agents;

Microsoft Defender for Cloud: cloud security with an AI Security Posture Management module;

Microsoft Defender for AI: detection of threats aimed at AI systems;

Microsoft Purview: data protection and governance, including what agents have access to;

Microsoft Sentinel: an event collection system, including Sentinel Data Lake (a cheaper storage format);

Microsoft Security Copilot: an AI analyst assistant, with ready-made agents for phishing triage and incident response;

Microsoft Agent 365: a product that became generally available on May 1, 2026; lifecycle management for AI agents in the Microsoft 365 environment, including audit, inventory, and access policies.

All of this either already comes with the Microsoft 365 E5 subscription or is available as an add-on to it. Microsoft is essentially telling large customers there’s no point in using SailPoint, CyberArk, or Wiz, since all of it is in one package.

For the record, this isn’t the first time Microsoft has entered someone else’s category through the E5 license. It happened with Splunk, which Cisco bought in 2024 for $28 billion, where by the time of the purchase Splunk was already losing customers to Microsoft Sentinel. Or with antivirus, where Defender ate a significant share of the endpoint protection market, not by winning on technology but simply by being free for customers with E5. The same thing is happening right now with identity management, where Entra ID is already taking some customers from Okta.

For me as an investor this means that any category Microsoft declares part of E5 loses the valuation premium of standalone players. And it isn’t because Microsoft built a technologically better product (as a rule the standalone players’ product is better). It’s because many customers have a budget constraint or a desire to save. We all understand that if you can get a good enough product for free as part of an already paid subscription, then buying an excellent product separately may be an excessive expense.

The Microsoft session also had an interesting case I’d single out. Vanessa Anderson talked about an internal Microsoft term, “double agents,” meaning compromised AI agents that start attacking other agents in the same environment. Reports are already reaching her of cases where such agents go out of control. And since most organizations still have no emergency shutdown mechanisms, Anderson forecasts a “Wild West” of cyberattacks.

If double agents become reality, that creates a direct demand for new types of products: sandboxes for agents, behavioral baselines for each agent, access-rights limiters, kill switches, and so on. These are all new categories that don’t exist yet. Microsoft is already building some of them, and some remain a field for startups like Ploy or new players.

144 machine accounts per person

Since we’ve touched on Ploy, Jacob Prime, the company’s founder and CEO, also took the stage and offered information worth remembering his name for.

At the start of 2024, the average enterprise had 92 machine accounts per human account, meaning service accounts, tokens, API keys, everything used not by people but by programs to access systems. In 2025 that ratio became 144 to one. Nearly 2x in twelve months. We’re well aware that even this figure is already a year old, and that today, by Prime’s estimates, the real ratio is substantially higher.

Machine identities are harder to manage than human ones, for four reasons. They aren’t tied to an HR system and have no end date (unlike employees, who leave). Their secrets (API keys, tokens, and so on) often go unrotated. Their owners inside the company are often unknown, especially when the original creator of the account has left, which loses the context of why it was created.

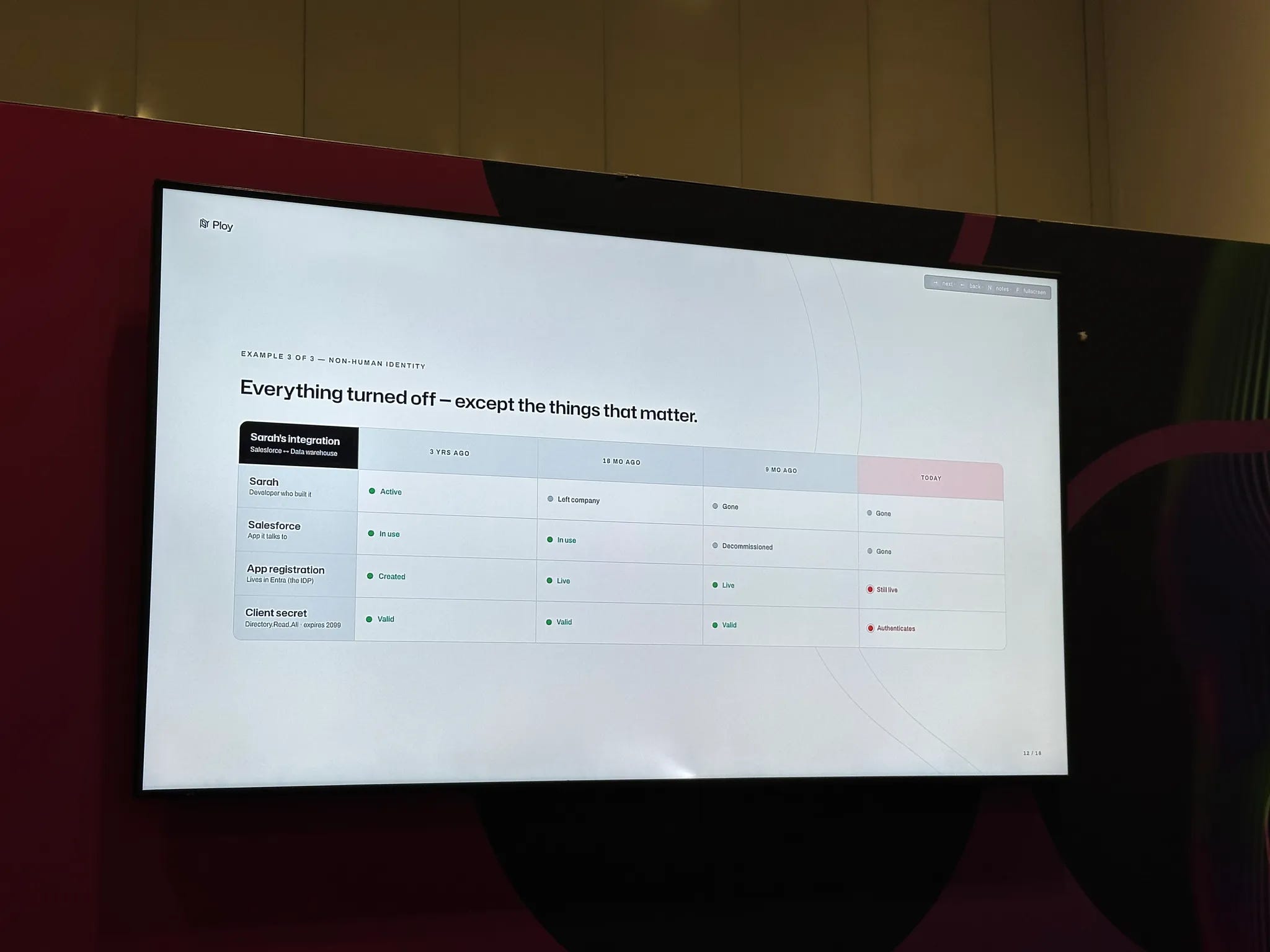

Prime gave a simple example. Sarah, an engineer, created an account three years ago to connect Salesforce to the corporate data warehouse. The account has read rights to the entire catalog. Sarah leaves the company. Someone leaves Salesforce. The account keeps running and nobody knows who owns it, what it was created for, or whether it can even be switched off.

Ploy’s solution to this problem is not to buy a new tool but to use the data already in the systems. You have an HR system. You have access tickets, you have logs, you have data on how a person actually uses access, and you have the IP address the request came from. Put all of it into a single decision-making context, and it automatically becomes visible that a developer in London who requested access to a financial system from Berlin outside working hours deserves an extra question. And that Sarah, whose account has been inactive for almost a year, deserves an automatic shutdown.

Yes, Ploy is a private company, a competitor to Okta IGA and SailPoint in access management. And it’s neither the first nor the last startup in this category. Astrix Security, Oasis Security, Aembit, Token Security. All of these companies are aiming at the machine-account management segment. By one estimate, the total market here could grow to $5 billion a year by 2028. But the question for an investor here is simple: will Microsoft take this category through Agent 365, or will room remain for standalone players? Right now it looks like Microsoft will close the middle layer of the problem, agent management within the E5 environment. But in large companies, where half the infrastructure sits outside Microsoft (in AWS, in Google Cloud, in their own data centers), room will remain for other players. One of those players will most likely be bought within two or three years by one of the big firms. Candidate buyers include CyberArk, Okta, SailPoint. CyberArk, for example, already bought Venafi in 2024 for $1.5 billion, which is the first large deal in this category. Not the last.

And one more detail from the Ploy session that matters. Prime said that across three years of conversations with roughly five hundred companies, he didn’t meet a single one that had solved the problem of an employee moving between roles. When a person moves from one position to another, they’re granted new rights. And the old ones? The old ones stay. Over several years of work, the same employee accumulates a tail of dozens of rights they don’t use but that remain open attack vectors. This is possibly the biggest unsolved problem in access management, and whoever solves it automatically will be able to win most of the market.

Buying cyber risk

The session with the CISOs of NatWest bank, oil company BP, and KPMG was called “Red is not a Business Case.” The title refers to the standard practice of most CISOs, who come to the board and simply show that some risks are marked red, some yellow, and some green. But that tells the business almost nothing, because it’s unclear exactly how much money could be lost, what causes the greatest damage, and where the budget should actually go. So NatWest and BP arrived at the conclusion that what’s needed is not a colored map but a monetary risk model, where each threat is translated into probabilities, sums, and a concrete business effect. That’s precisely why they referenced the book “How to Measure Anything in Cybersecurity Risk” as a tool that helps count risk in dollars rather than gut feel.

The problem is that there are endlessly many attacks, they differ by type, speed, cost, and consequences, and the old approach doesn’t scale. If you assign every attack its own label, the system chokes on detail. So instead of breeding new categories for the sake of categories, you have to break the whole flow of attacks down into a few manageable parameters that can be counted automatically and updated in real time. Hence the idea of a platform that doesn’t just log incidents but immediately assesses their danger, builds a heat map, and helps make decisions on the fly. The question is which problem costs the most at a given moment in time.

Security used to be funded by inertia, by quarter or by year, when the next round of approvals came around. Now management wants the budget to change dynamically, almost like algorithmic trading, where the decision is made on the current state of the market rather than on yesterday’s report. This makes CRQ, cyber risk quantification, a potentially very important category, one that turns security into an intelligible financial mechanism for managing capital.

The following conclusions follow from this. Companies like Arch Capital, Axis Capital, CNA Financial end up in the right place, because they sell a way to translate cyber chaos into a language the CFO and the board understand. BitSight under Moody’s is especially interesting, because Moody’s already knows how to sell credit risk, and can now embed cyber risk into its traditional financial infrastructure. If CRQ becomes the standard for large companies, those are exactly the players that will get a long tail of revenue. And the insurers follow, because if risk can be counted, it can be insured on a new logic. Then cyber insurance becomes an extension of the same risk model, only now with a premium and a policy.

Back to Okta

On April 2, 2026, I positioned Okta as the control tower for the agent era, the point through which all identity passes in a new world where machines work alongside people. The thesis rested on three pillars. The first is cybersecurity as the only sector for which AI is simultaneously a threat and a source of demand. The second pillar rests on the fact that in the agent era the identity layer becomes the main layer of defense. The third factor is the assumption that Okta remains one of the neutral public companies capable of occupying that layer. So it was extremely interesting to watch the company's news come out, to see which of my theses was right and which went unrealized.

For ordinary software, AI compresses the marginal revenue curve, because agents replace human users. For cybersecurity the curve works the other way. The more powerful the attacker’s models, the more complex the attacks. The more complex the attacks, the higher the marginal value of each defensive solution. And on the shareholder call this thesis was confirmed. Management said that after the Mythos leak and the rise of public concern about agentic AI, company leaders and boards aren’t panicking but returning to fundamental principles. Everyone recognizes that the threat is real, that the system always had and always will have zero-day vulnerabilities, that there will now be more of them, and that this requires setting aside dedicated money for defense. So the number of potential customers for Okta’s new products is now the largest in the company’s history. But management stresses that this number is not yet revenue, and that the year’s main task is to convert it into real signed contracts. New products made up 25% of the quarter’s total signed contracts, whereas the April article touched on a figure of 30%. That’s extremely close to the forecast, so the upward trend really is gaining momentum.

At the same time, the company’s neutrality really does remain one of its three main advantages. Looked at closely, the list of partnerships with model providers confirms this position in practice. An agreement was signed with ServiceNow to embed Okta for AI Agents in their AI Control Tower. A deal was signed with Google on identity management for their agent gateway. With Amazon there’s an integration with Bedrock Agent Core. Okta became one of the launch partners for OpenAI’s new product, GPT 5.5 for security. And, crucially for the overall picture I described earlier, Okta is taking part in Anthropic’s Project Glasswing, testing a preview of the Mythos model and integrating it through a compliance API. In plain terms, Okta sees Mythos from the inside, before its public release, and adapts its products to its capabilities.

As for the company’s overall financial results, I correctly noted the habit of giving cautious forecasts and then beating them. It’s a simple observation, but in Q2 FY27 it really did hold up.

Where I was wrong

Monetization of agentic AI is happening fairly slowly, which is why the pricing model lags as well. In the data for the last quarter, revenue from agent products is immaterial. It’s built into the annual forecast with a large conservative adjustment. The customer potential is big, but all of it still has to be turned into real signed contracts, which will take time.

Okta sells agent products as an uplift on the existing per-user price. That is, the customer pays on top of the standard subscription for each active or named user who gets an agent. This is deliberate. If you price on actual consumption, as many AI providers do now, customers don’t know how to budget it. A large enterprise’s budget cycle isn’t ready to accept variable costs. So Okta sacrifices deal size for the speed of closing it. At renewal, when the customer has actual usage statistics, a consumption component can be added. And this is probably the most sensible move, where you first attract the customer with excellent terms, and once they realize the quality of the service, you get the chance to change the pricing model.

But at the same time this approach shifts the inflection point. A substantial contribution from agent products to revenue won’t happen in Q3-Q4 of the current year, as could have been read in my April article. It’s more like 2028-2029, when the first annual contracts come up for renewal and a variable component can be built in.

At the same time the company is investing in growth. It’s cutting administrative costs but increasing investment in sales, marketing, and new product development. Headcount grew 12% year over year (the fastest staff expansion in several years). From a long-term strategy standpoint this looks like the right decision, since the company has enormous deal potential. To sell agent products Okta created a dedicated team that does nothing but customer conversations on this topic. Companies usually carve out such teams only for areas where they see revenue three to five years out.

The company also cut its own revenue from implementation services, handing that part to global systems integrators. They now train their own specialists to work with Okta products, which creates a double effect. The company loses a small share of consulting revenue but gains partners with engineers sitting at their booths trained on Okta products. Those engineers will pitch Okta to their customers in every subsequent deal. And that effect is already showing up in the results. So cutting investment at the moment you hold the biggest growth window in a decade would be a strategic mistake. But it pressures operating margin and only confirms that the investor’s greatest return will come several years out.

The battle with Microsoft

For many quarters Okta’s win rate against Microsoft hasn’t changed much. The good news here is that Okta holds its ground and isn’t losing the market. The bad news, as described earlier, is that Microsoft, through its subscription product Entra ID inside the E5 package, keeps up constant pressure, and the portion of customers who take that solution as part of an already paid subscription is closed to Okta.

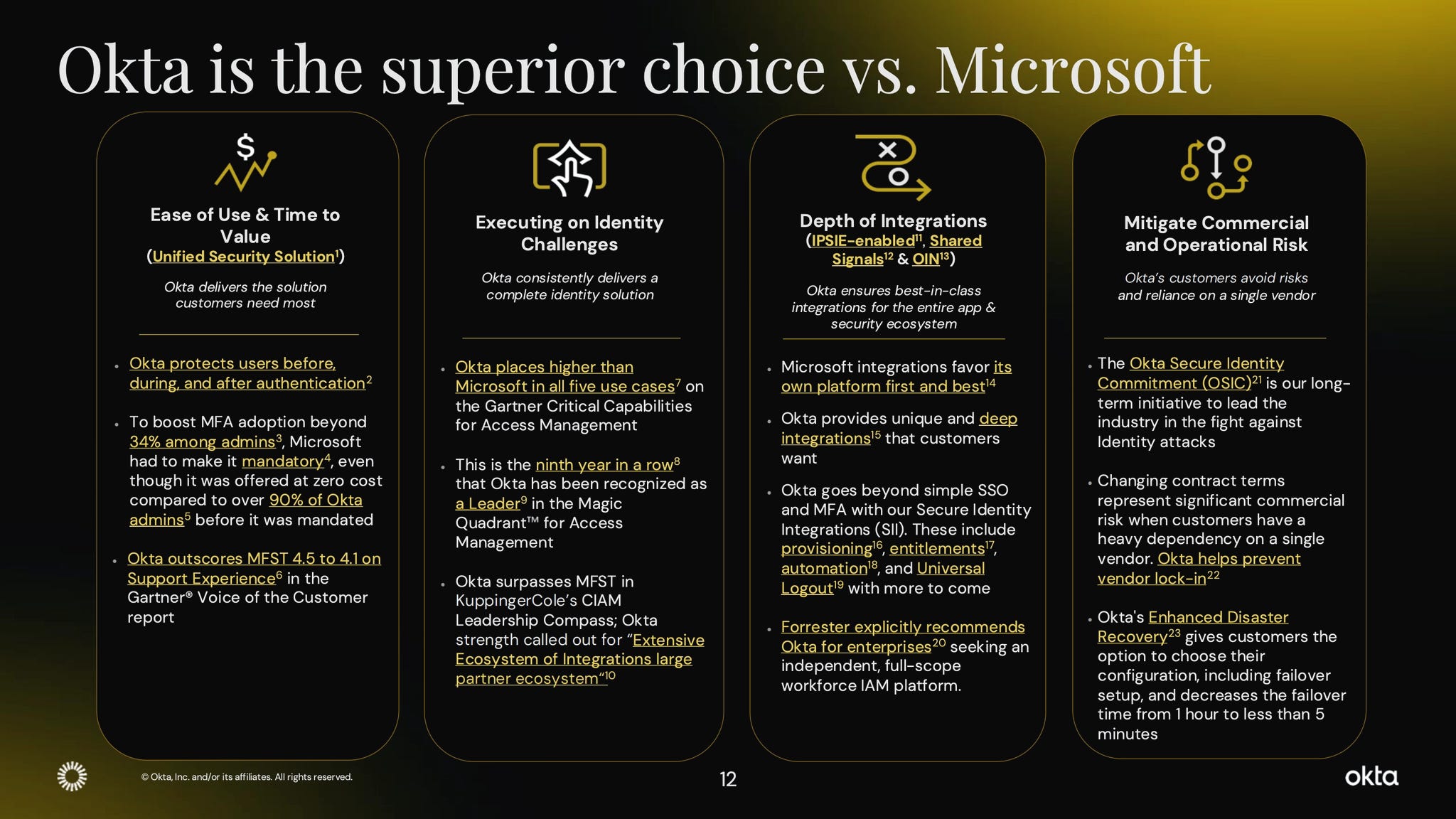

Yes, this was already known from general market observation. But what’s interesting is that in an investor presentation published on May 28, Okta for the first time made an extended comparison of itself with Microsoft on four specific fronts. You don’t often see a company publicly articulate exactly how it’s better than its main competitor, and which of those advantages can be verified against independent sources. So let’s go through all four arguments in turn.

The first argument is ease of deployment and time to value. Okta protects the user before they try to log in, at the moment of login, and after it. Microsoft historically protected only the login moment itself. Okta backs this with concrete evidence from its own marketing statistics. To raise multi-factor authentication coverage among administrators of its own systems above 34%, Microsoft had to make it mandatory. Even though it was available for free. By comparison, Okta’s MFA coverage among administrators exceeded 90% before it was made mandatory by company policy. The difference is that Okta is a product bought specifically for identity, and its users understand why it’s needed. Microsoft Entra comes bundled with other products, and some administrators simply don’t use the functions they don’t formally pay for separately.

Another factor that fits the same category touches on working with support. The independent Gartner rating gives Okta 4.5 points out of 5. Microsoft is given a rating of 4.1. The gap may look small, but in the enterprise software industry it’s a meaningful spread that can hold up a huge volume of work. Buyers of large security systems are extremely sensitive to support quality, because at the moment of an incident the quality of the line to the vendor determines response speed. Price isn’t the main thing at a large enterprise. The main thing is that such costs pay off by avoiding potential losses from time wasted waiting for an adequate answer from an on-call engineer, which can cost far more.

The second argument is identity maturity. In the comparative Gartner Critical Capabilities for Access Management report, Okta scores higher than Microsoft in all five core use cases. These are scenarios like workforce identity, customer identity, protecting third-party contractors, supporting complex architectures, and working with applications on third-party platforms. This is an objective rating from an independent analyst, and Okta uses it as its main documentary argument in sales. On top of that, for 9 years running Okta has been recognized as a leader in the Gartner Magic Quadrant for access management. No other vendor in this niche has held leadership that long.

And one more independent rating is the KuppingerCole CIAM Leadership Compass (a specialized report on customer identity). Okta tops it. The main advantage noted in this rating is its extensive integration ecosystem and large partner network. This leads smoothly into the next argument.

The main advantage noted in this rating is its extensive integration ecosystem and large partner network. This leads smoothly into the next argument, which rests on depth of integrations. This is probably the most important argument of all four, because it answers the question: why does a customer who already pays Microsoft for E5 and can formally use Entra ID for free still also pay Okta?

The logic here is as follows. A large company uses hundreds of applications. Salesforce, ServiceNow, Workday, Snowflake, Slack, GitHub, another couple of hundred internal and third-party systems. These applications need to be connected to the identity platform so that single sign-on and multi-factor authentication work everywhere. And at this point Microsoft and Okta do different things. Microsoft builds its integrations first and best for its own stack. That is, Office, Teams, SharePoint, Dynamics, Azure. This makes sense, because Microsoft protects its own platform. But if your company runs not only the Microsoft stack but also five hundred third-party applications, those integrations will be shallower and simpler with Microsoft. Yes, they’ll cover the basic scenarios (single sign-on and multi-factor authentication), but they won’t go further.

Okta builds integrations differently. They call them secure identity integrations. It’s not just single sign-on, but also automatic creation of an account in the application when an employee starts work. Automatic management of access rights inside the application. Automatic shutoff when an employee leaves. And, critically for the era of AI agents, a single logout mechanism that can simultaneously terminate all sessions of a compromised account across all connected systems at once. To gauge the scale of this work, Okta now has more than 8,000 built-in integrations. This network can’t be bought and can’t be replicated in a quarter or a year. It was built over 17 years, and each integration required work with each application vendor. So in its report on workforce identity Forrester explicitly recommends Okta for large enterprises seeking an independent, full-scale platform. This is the very moat around Okta’s business. Not superiority in single sign-on technology, but precisely the depth of embedding in 8,000 third-party applications.

The fourth argument is the mitigation of commercial and operational risk. If you build all your identity on one vendor that also sells you an operating system, an office suite, cloud infrastructure, and a meetings system, you fall into total dependence. That company can change the terms and you can do nothing. The history of recent years shows that Microsoft regularly raises prices on the E5 package and adds new licensing restrictions to it. A customer who put all their eggs in one basket can’t negotiate.

Okta builds its commercial argument on this fear. They have a formal secure identity commitment, and one part of it is about helping customers avoid lock-in to a single vendor. From the outside this looks like marketing, but in fact it’s a real commercial position that large CFOs understand perfectly well. The second factor that can be placed in this category is operational reliability. Okta has a product that cuts recovery time during an infrastructure failure from one hour to less than five minutes. This is critically important for banks, government institutions, and large online stores. Microsoft has similar metrics too, but they’re standard for the whole package and can’t be configured separately for the identity of other products.

By the pure logic of the mass market, free wins, but in reality it’s more complicated. First, among large enterprises (which, for the record, are 85% of Okta’s revenue) priority shifts toward quality and independence from a single vendor. These companies are willing to pay for significantly better quality, especially after surviving incidents tied to single-vendor dependence. A tailwind for the company here was July 2024, when a CrowdStrike update took down millions of Microsoft Windows devices worldwide. After an incident like that, the concept of avoiding a single point of failure became a main topic in the boards of large companies.

Second, in the complex-identity category Microsoft simply doesn’t cover all scenarios in the standard service package. To get the same quality as Okta, you have to buy additional third-party modules, and then the savings from E5 evaporate.

Third, in the agent era neutrality becomes a functional requirement. A customer uses agents from OpenAI, Anthropic, Google, Microsoft, and their own teams all at once. If they build identity on the Microsoft stack, it will work with Microsoft Copilot better than with other providers’ agents. That’s a compromise a large customer won’t make. Here too Okta has the advantage.

At the same time, migrating from one identity provider to another is a very expensive and lengthy operation. Customers who have worked with Okta for 7 to 10 years won’t leave for Microsoft Entra just because it’s free. The switching cost is too high. That is, Okta’s current customer base is protected. The battle isn’t over it, but over new customers and expansion within existing ones. Okta holds its share on the deals where the two are directly compared. This means the overall growth of the identity market splits between the two companies roughly stably, not in Microsoft’s favor, which in my view is an extremely important indicator, given that we’re comparing these companies.

Conclusion

For decades cybersecurity was a business where all the key problems were known in advance but went systematically unsolved, because solving them broke the economics of the industry itself. Building secure-by-design systems would have meant removing the recurring demand, cutting the number of incidents, lowering the need for constant updates, services, and add-ons. It proved far more profitable to live in a state of permanent vulnerability, which created a market that earns not from the absence of problems but from their endless reproduction at a managed pace.

AI simply zeroed out this balance. It didn’t bring fundamentally new types of attacks, it just removed time as a variable; attacks grew more frequent and shrank in their time window. The entire operational model of security existed inside that time gap. When the gap disappears, so does the very ability to manage through the usual mechanisms. At that moment the market starts collapsing into a simpler form. Anything that requires coordination between several systems, people, and layers becomes too slow. Anything that creates an additional interface, an additional alert, or an additional decision point starts working against the goal itself. So security stops being a set of tools and turns into a layer that either makes the decision itself or has no meaning at all.

Against this backdrop the overall state of the industry stands out especially clearly, something our Analyst 3553 Research captured precisely:

“The general mood, of course, is built around the AI era. Everyone, from the operations director of the NCSC (National Cyber Security Centre UK) to the head of the Metropolitan Police Service, is saying that AI attacks can only be beaten by AI defense. But for that you need to collect an enormous amount of data, and that’s exactly where most run into the maximum challenge: how to do it, how to be sure you’re doing it right, and how to do it fast enough. There are clearly more questions than answers so far. The second most frequently repeated thesis rests on the fact that the biggest vulnerability is the human, not the machine. Paradoxically, you simultaneously have to teach the consumer not to click suspicious links and in parallel train the LLM. Not once during the entire conference did the phrase ‘let’s cut costs’ come up. There was a felt awareness of the real threat and an understanding that a single successful attack can destroy a business, so no one is planning to economize on cybersecurity.”

This is an indicator of a turning point, because the industry simultaneously admits that the old approaches no longer work and doesn’t fully understand what the new model should look like. The demand to “collect more data and react faster” sounds logical, but in practice it runs into the same limit of system complexity and fragmentation. And that’s exactly why the next step turns out to be not in scaling up tools, but in collapsing them.

AI, contrary to the popular narrative, doesn’t make the market more competitive. It makes it more concentrated, strengthening those already built into the infrastructure and devaluing those standing next to it. Microsoft doesn’t have to be the best in each individual product, because it’s enough for it to be good enough at the point where the customer already is. Google doesn’t have to win on model quality, because it’s enough for it to control the surface through which the user gets the answer. In cybersecurity, the winner isn’t whoever detects the threat better, it’s whoever can close it right away, without asking permission from five other systems.

Against this backdrop it becomes clear why the industry held off for so long on moving to secure-by-design architectures. It’s a plain misalignment of incentives. Security as a foundation reduces turnover. Security as a process increases it. But when attack speed moves beyond the human management cycle, the system can less and less afford inefficiency for the sake of revenue. The compromise the industry rested on gradually stops working. As a result security stops being a function of IT and becomes a function of the distribution of power inside the digital infrastructure. Whoever controls identity controls the entrance. Whoever controls traffic controls the interaction. Whoever controls data controls the context. And whoever can unite all of this and make decisions automatically effectively controls the system itself.

And here the main question appears, the one that so far remains unanswered: who exactly becomes that decision point?

In my view, we won’t ever see the utopian version Chichester touched on, and the system will remain fragmented, with different defensive layers from each separate player and simplified defense options from big companies like Microsoft, all of it just happening in an attempt to embed AI functionality into each separate layer.

So Okta’s position still remains one of the strongest in the market, because it sits right at the point where the new need for an identity layer arises in an era when agents work alongside people and machine accounts outnumber human ones many times over. Okta is already built into thousands of applications, and that embeddedness paired with quality is a fundamental advantage over any conglomerate like Microsoft. But as I noted earlier, the maximum return won’t come in the next one or two quarters, but several years out, when the market finally settles.