Newmont Corporation

Industry leader in sustainability and environmental stewardship. Holds the world's largest gold reserves: approximately 100 million ounces.

Newmont Corporation is the world’s largest gold mining company, headquartered in Denver, USA. Founded in 1921, one of the oldest mining companies in the world.

Competitors: Barrick Gold, AngloGold Ashanti, Kinross Gold, Gold Fields, Newcrest Mining, Agnico Eagle Mines.

The company publishes quarterly investor updates with financial statements, presentations, and shareholder conference calls.

The Economy and the Gold Price

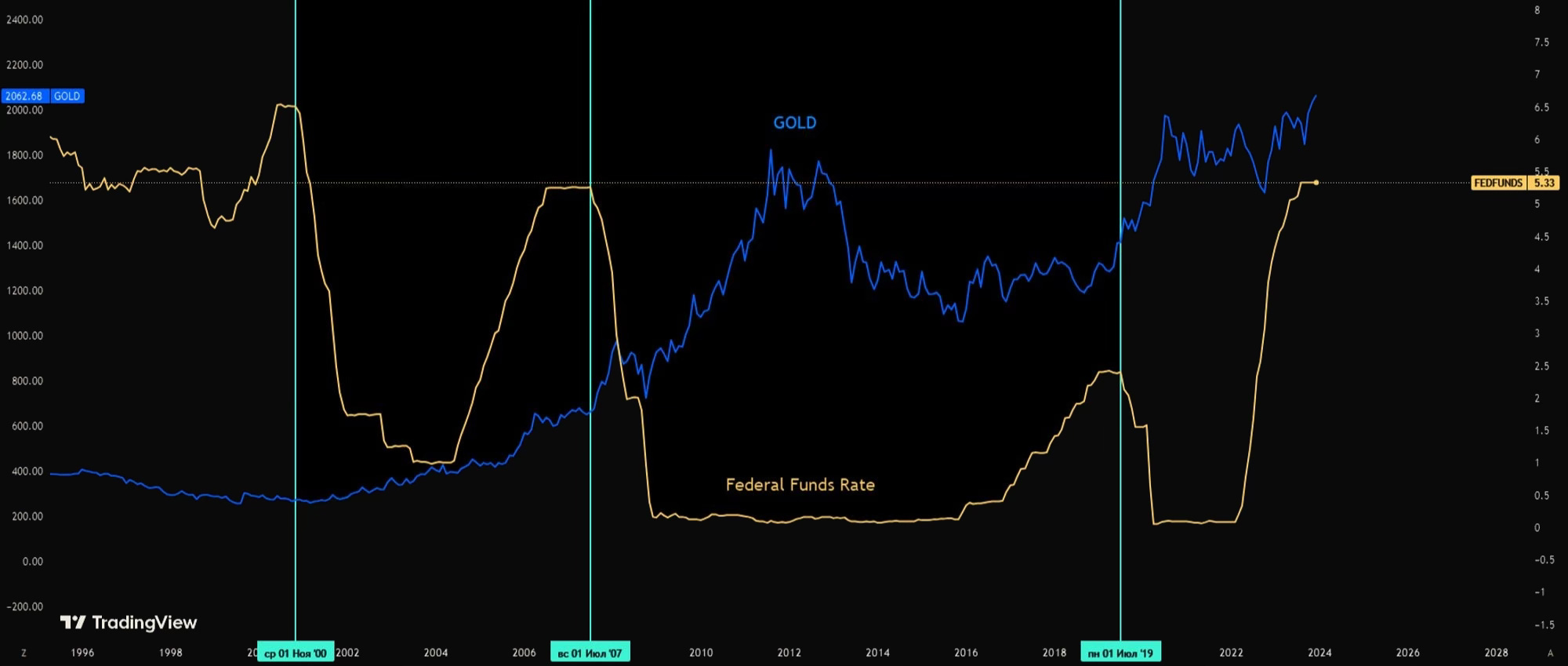

Interest Rates

Gold has historically been considered one of the most reliable assets in times of crisis and uncertainty. Against the backdrop of escalating geopolitical tensions (the Russia-Ukraine war, the Israel-Hamas conflict, the dispute over Taiwan) and a likely slowdown in major economies, demand for gold as a safe haven is rising significantly.

Expected Fed rate cuts have historically been positive for gold prices as well, since lower rates reduce the yield on competing assets such as bonds and bank deposits. When yields on interest-bearing alternatives fall due to cheap money, demand rotates into gold as a more attractive store of capital. The chart showing the relationship between Fed rate cuts, marked by the red vertical line, and gold prices illustrates this clearly.

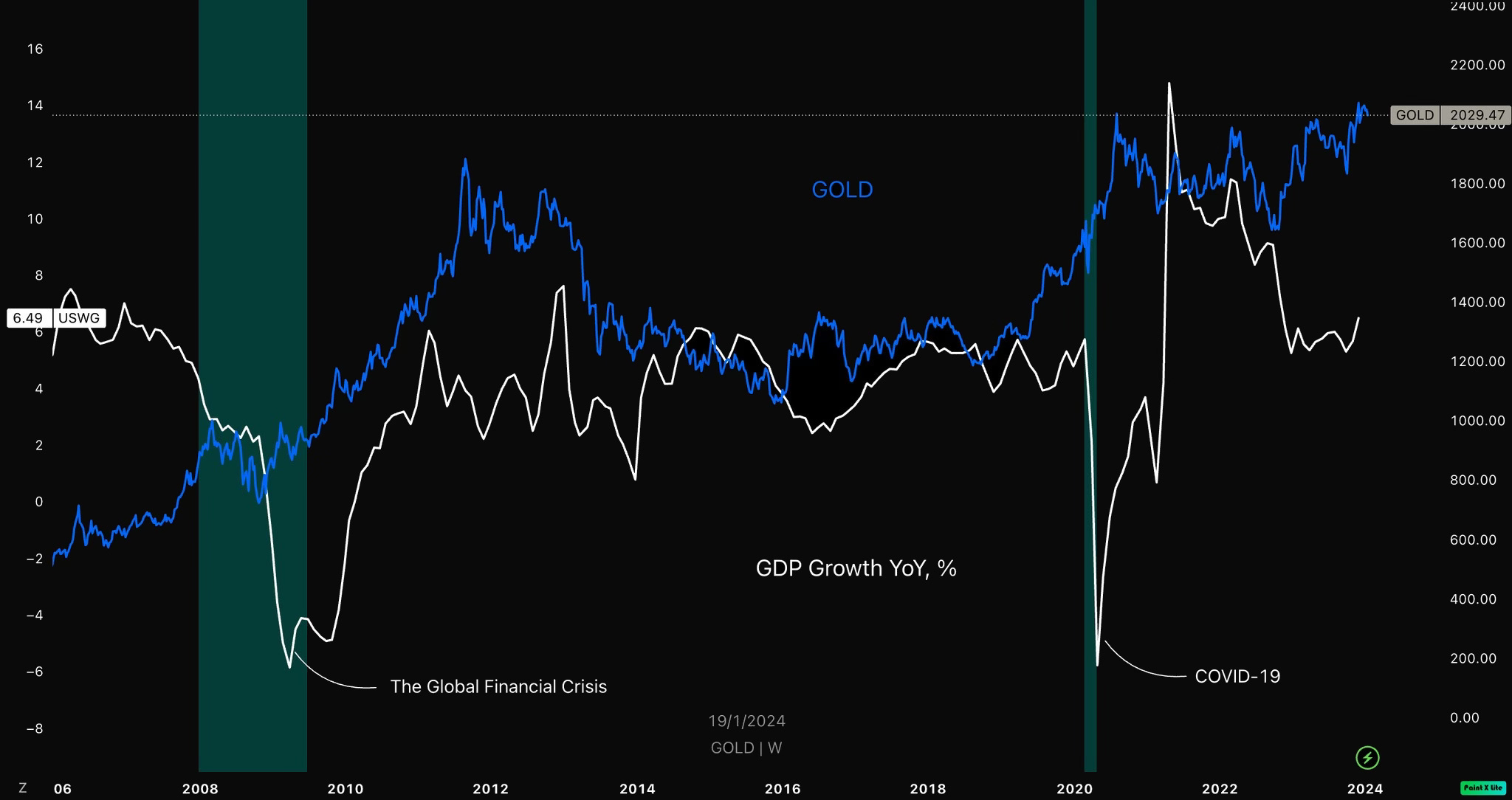

GDP

Another fundamental driver: every time US GDP has deviated significantly below the fifty-year average growth rate of 2.7%, gold prices have risen. Two clear examples from recent history are 2009 and 2020. During the 2020 pandemic, US GDP contracted 2.8% below the average, while gold prices rose 24.4%. The post-financial crisis period of 2009 produced a similar 2.6% GDP shortfall, during which gold rose 27.6%. Recessions are marked in red on the chart, showing the co-movement of GDP and gold prices.

Fed rate policy, potentially weak GDP growth, and contained inflation all point toward the start of a rate-cutting cycle this year. As returns on fixed-income investments look less attractive next year, demand for gold may increase, given that the opportunity cost of holding it will fall.

DXY

The broader US macroeconomic picture also looks less favorable against the backdrop of rising government debt. A weaker dollar is entirely plausible, and that too is a positive for gold, given their negative correlation, as shown in the chart. The logic: since gold is denominated in US dollars, a cheaper dollar raises gold’s value in other currencies, making it more attractive and lifting demand.

Central Bank Gold Purchases

Total central bank gold purchases in 2023 came to 1,136 tonnes. The highest level of net purchases on record since 1950, specifically since the dollar’s convertibility into gold ended in 1971. The 13th consecutive year of net central bank buying.

The buildup of gold reserves is driven primarily by the following:

Reserve diversification and risk hedging, as gold is viewed as a reliable asset amid geopolitical tensions and financial instability.

Inflation protection: gold preserves value over the long term, unlike paper money, shielding reserves from debasement.

Rebalancing away from dollar-denominated assets, reducing exposure to dollar fluctuations and US monetary policy (for China, this is part of a de-dollarization strategy and a reduction of financial dependence on a rival state).

Preparation for a potential transition to a new monetary system, possibly a gold standard, in the event of a crisis in the current fiat system.

Central bank reserve accumulation will most likely continue into 2024, helping them prepare for potential global financial shocks.

Gold has a unique advantage that no other asset possesses: in extreme scenarios, when financial systems or economies collapse, gold does not lose its value. Unlike paper money, equities, bonds, and other financial instruments, which depreciate rapidly during collapses, hyperinflation, and deep crises, gold continues to preserve purchasing power and function as a reliable store and medium of exchange. That is why I think holding 5-10% of an investment portfolio in gold is a sound idea.

Annual Financial Review

Income Statement

Compared to 2020, the years 2021 and 2022 saw a broad-based deterioration across most financial metrics: gross profit, operating income, net income, and EBITDA. The sharpest decline was in net income, from $2.83B in 2020 to $1.16B in 2021 and then a loss of -$429M in 2022.

This reflects higher operating expenses and a general downturn in the gold mining sector in response to the Fed’s rate hikes, as management itself acknowledged on the 2022 earnings call.

Based on management’s comments in Q4 2022, Newmont faced several headwinds that weighed on profitability. Inflation drove up prices for raw materials, energy, and other inputs required for mining operations. Steel, explosives, and fuel all got more expensive. As a result, Newmont’s operating costs for sourcing these inputs to keep its mines running increased. Inflationary pressure also forced the company to raise wages to retain staff, adding further to operating expenses.

In the end, despite stable production volumes in 2022, Newmont’s earnings declined due to higher operating costs across materials, energy, and labor. And since inflation affected the entire sector, other mining companies faced the same pressures in 2022.

Newmont conducted an impairment test on several assets and concluded that their carrying values were overstated by approximately $1.3B relative to fair market value. The CC&V mine was written down by $500M. The Cerro Negro and Porcupine goodwill was impaired by $800M. Goodwill is an intangible asset that arises when a company is acquired at a premium to the net book value of its assets: the impairment indicates that Newmont overpaid for these assets at the time of acquisition, and their actual value is lower.

The $1.3B is not a real cash loss. It is a revaluation and adjustment of carrying values to current market values. This primarily affects accounting metrics rather than actual cash flows, so it has no fundamental significance.

What does matter fundamentally is the Fed’s battle with inflation. Higher interest rates bring inflation down.

Lower inflation means Newmont’s input costs (wages, materials, fuel, etc.) grow more slowly. But lower inflation also generally depresses commodity prices, including the metals Newmont mines.

High Fed rates are associated with economic uncertainty, which pushes investors toward fixed-income assets like bonds, whose yields rise with rates. A tightening cycle creates additional risks and pressure for Newmont’s business.

Balance Sheet

From 2020 to 2022, total assets declined approximately 7% (from $41.4B to $38.5B). Liabilities rose 8% over the same period (from $17.5B to $18.9B). Equity contracted more sharply, down 18% (from $23.9B to $19.5B). Net debt grew 4.5 times (from $0.5B to $2.3B).

Newmont’s financial position deteriorated: assets shrank, debt load increased, equity fell. This reflects lower revenue on the back of declining gold prices alongside higher capital and operating costs driven by rising interest rates.

Cash Flows

Operating cash flow declined from $4.9B in 2020 to $3.2B in 2022, reflecting a deterioration in operating profitability under cost pressure. Investing outflows surged from $0.2B in 2020 to $3.21B in 2022, likely reflecting active investment in production expansion. Financing outflows (dividends, debt repayment) first rose from $1.79B in 2020 to $3.06B in 2021, then fell back to $2.13B in 2022. Against this backdrop, free cash flow declined from $3.6B in 2020 to $1.1B in 2022. In 2022, cash generation contracted while capital expenditures increased.

Quarterly Financial Review

Income Statement

Based on the Q3 2023 earnings call transcript, the key drivers of the quarterly financial changes are as follows. Revenue declined due to lower gold production volumes. Gross profit fell on the back of lower revenue and higher production costs. Operating income dropped as a direct result of the gross profit decline. Net income was hit by lower operating income compounded by one-time settlement costs related to the labor dispute at the Peñasquito mine. EBITDA contracted due to reduced operating income from lower gold output versus prior quarters.

Management’s explanation for the Q3 2023 shortfall centered on production stoppages and reduced output at the company’s largest assets: the Peñasquito, Boddington, and Tanami mines, due to a strike, adverse weather, and project delays. This directly impacted gold production and sales volumes. Compounding the issue were weak operating results at the Nevada Gold Mines and Pueblo Viejo joint ventures, in which Newmont holds 38.5% and 60% stakes respectively.

Production costs and inflationary pressure also increased, weighing on margins. Settlement costs from the Peñasquito labor dispute further reduced net income. Management characterized these problems as temporary and emphasized a focus on improving operational and financial results in Q4 and through 2024.

Balance Sheet

The asset decline is driven primarily by depreciation of fixed assets, not fully offset by new capital investment. The modest increase in liabilities reflects higher accounts payable and other current obligations. The significant equity reduction stems from the net loss recorded during the period, which reduced retained earnings. Net debt growth reflects additional borrowings and lower cash and equivalents on the balance sheet.

Summarizing the Q3 2023 commentary, management focused on the decline in net income and equity as stemming primarily from temporary operational issues: the Peñasquito strike, reduced equipment performance at other assets, and unfavorable weather. The underlying ore reserves remain unchanged; only the extraction timeline has shifted. The increase in debt reflects financing requirements for an expansive capital program aimed at growing production and improving efficiency. Overall, the company’s financial position remains stable, as evidenced by the maintained investment-grade rating of A-.

Q4 is expected to show improvement in both operating and financial results as the temporary headwinds are resolved. In the medium term, the Newcrest acquisition will substantially strengthen Newmont’s business and profitability.

Cash Flows

The decline in operating cash flow reflects lower net income during the year due to production problems at key assets and a broad deterioration in operational results. Negative investing cash flows are tied to the execution of the company’s capital program, with the quarter-on-quarter reduction reflecting cost optimization in the face of production difficulties. The increase in financing outflows is driven by higher dividend payments in line with the company’s dividend policy. The positive free cash flow in Q3 reflects strong operating inflows and reduced capital outflows.

Based on the Q3 2023 earnings call, management’s commentary on cash flow dynamics pointed to the same conclusion: the operational deterioration is temporary, the ore reserves are intact, investing outflows reflect a deliberate expansion program, and the company remains confident in the fundamental investment case.

The increase in negative financing cash flows reflects higher dividends under the stated dividend policy.

Management attributed the negative trends to temporary factors and expressed confidence in the fundamental long-term attractiveness of the business.

Shareholder Call

Key Positive Takeaways

The upcoming Newcrest merger will create the world’s largest gold mining company with 10 Tier 1 deposits, a business with significant long-term growth potential and the ability to generate stable returns for decades. Newmont has a strong global operating model and experienced leadership that has already executed successful M&A, including the Goldcorp deal. This gives investors and management confidence that the Newcrest asset integration will succeed.

The Lihir and Cadia deposits in the Newcrest portfolio have significant potential for cost reduction through the Full Potential self-improvement program, which has already demonstrated strong results at Newmont’s existing assets. Newmont has a solid balance sheet and a sensible dividend policy. The company generates substantial free cash flow even in the current volatile environment.

Newmont is well positioned in the market against the backdrop of growing gold demand from central banks and investors. This creates favorable long-term prospects for the sector. The successful resolution of the Peñasquito strike in Mexico, the largest polymetallic deposit in Newmont’s portfolio, and its return to production materially improves the company’s outlook.

Key milestones reached at major development projects including Tanami, Cerro Negro, and Porcupine, which will expand the resource base and extend mine life in these regions. Strong Q3 financial results despite the headwinds: revenue of $2.5B, adjusted EBITDA of $933M. A demonstration of business resilience. Successful commissioning of five new autonomous haul trucks at Boddington, enabling faster operations and access to higher-grade ore.

First-ever A- rating from Fitch, underscoring Newmont’s strong financial position and flexibility.

Key Negative Takeaways

Production guidance for 2023 lowered to 5.3 million gold ounces from existing assets, due to the Peñasquito suspension, weaker-than-expected performance in Nevada, and reduced output at Pueblo Viejo.

Gear ring wear on one of the Ahafo mills reduced throughput to 60% in Q3, with approximately 70-80% capacity expected in the near quarters. Delays at the Tanami expansion project, requiring additional assessment of the lower shaft section, which may result in schedule and budget revisions.

Underperformance at uncontrolled joint ventures, Nevada Gold Mines and Pueblo Viejo, weighed on overall production metrics. Potentially material changes to Newcrest’s reserves and resources after audit under Newmont’s standards.

Significant restructuring and severance costs tied to the Newcrest integration. Uncertainty around the terms of a new collective agreement at Peñasquito following the strike, creating potential long-term risks.

Production volatility at Boddington in coming quarters due to higher stripping volumes and drawdown of ore stockpiles before transitioning to higher-grade ore.

Potential upward pressure on project capital costs, particularly in Australia, from rising labor costs, which could require budget revisions.

Difficulty forecasting 2024 production and costs until the Newcrest integration is complete and new mine plans are established.

Given the risks and potential benefits discussed on the call, a sensible strategy is to hold current positions (if you own the stock) or add modestly to capture the potential upside from the Newcrest acquisition in the medium term.

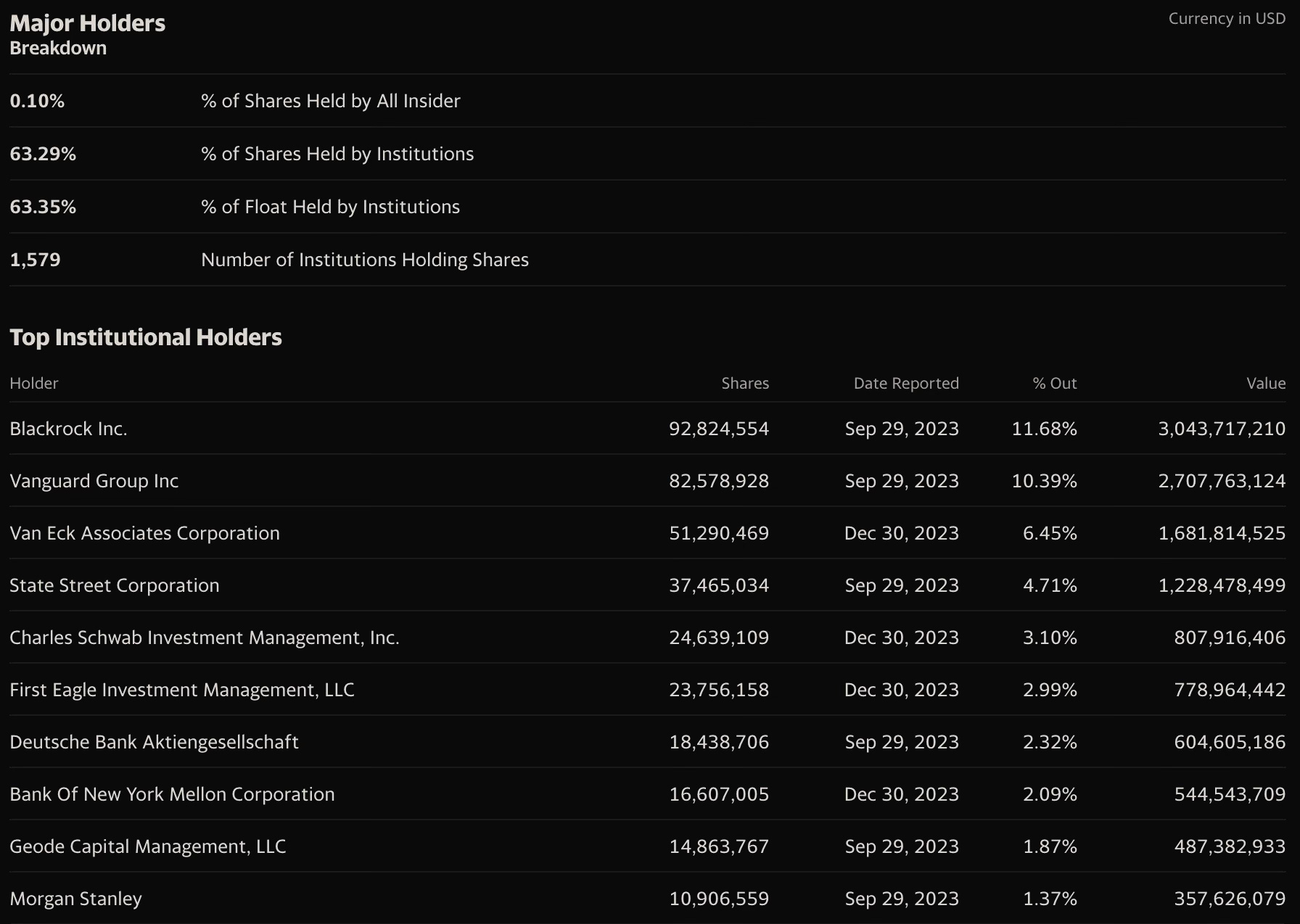

Shareholders

Insiders hold less than 0.1% of shares. Management’s interests are therefore weakly aligned with shareholder value. The dominant shareholder group (63%) is institutional investors, signaling that analysts and funds believe in the company’s long-term potential.

The key holders are the world’s largest asset managers and investment funds: BlackRock, Vanguard, Van Eck, State Street. This provides stable demand from conservative long-term investors. A large float means high liquidity and broad accessibility for different categories of investors.

The shareholder structure reflects Newmont’s investment appeal from the standpoint of long-term demand and liquidity.

Conclusion

Based on a comprehensive analysis of Newmont Corporation’s financial results, market outlook, competitive advantages, and growth plans, I conclude that the shares currently represent an attractive addition to a long-term portfolio. Three key arguments:

Despite the temporary difficulties of recent quarters, driven primarily by operational problems at specific assets, Newmont retains strong competitive positioning and leading industry efficiency metrics. This supports confidence in a financial recovery.

The strategic acquisition of Newcrest Mining will significantly expand Newmont’s scale and diversify the business with high-quality assets. The anticipated synergies will have a meaningful positive impact on future profitability.

Fundamental factors, including growing global gold demand, dollar weakness, and declining interest rates, create a favorable macro environment for the gold mining sector and for Newmont specifically.

Given these factors, I consider a purchase of Newmont shares with a medium-term (or long-term) investment horizon to be reasonable, as a portion of investment capital in your portfolio. Over that period, the company will have the opportunity to complete the acquisition and return to a growth trajectory in earnings and business value