Nvidia Corporation

Nvidia has earned a reputation as an innovator. The company pioneered the development of graphics processors that, by most accounts, transformed computer gaming.

NVIDIA is an American company focused on the development of graphics processors and related technologies.

Core areas of NVIDIA’s business:

GPU production: the GeForce series for gaming and graphics work, the Quadro and Tesla series for workstations and data centers.

Tegra system-on-chip (SoC) production for mobile devices.

Software development: the DirectX and Vulkan graphics APIs, the CUDA and cuDNN frameworks for neural network acceleration, image processing technologies.

AI, machine learning, and computer vision platforms: the NVIDIA DGX deep learning platform, NVIDIA AI model libraries and frameworks, the NVIDIA Drive platform for autonomous vehicles, NVIDIA Omniverse for 3D design and virtual worlds.

GeForce NOW hardware for game streaming and cloud services built on its own technology stack.

The company develops both hardware and software across all of these areas.

NVIDIA’s primary competitors in GPUs and AI solutions: AMD in discrete GPUs (Radeon cards, data center and supercomputing GPUs); Intel with its integrated and discrete GPU lineup and AI solutions including Habana Labs; Qualcomm and Apple with mobile SoCs that include GPUs and neural engines; Samsung with Exynos SoCs and AI development efforts; Amazon with its cloud AI chips Trainium and Inferentia. On the startup side: Tenstorrent (AI chips for automotive and robotics), Graphcore (Colossus processors for ML), and Cerebras Systems (CS-1 and CS-2 deep learning chips). Not all of these competitors are publicly traded.

Artificial intelligence is not another fad like the metaverse or NFTs. Once you integrate AI tools into your workflow, the productivity gains are obvious. More and more people are discovering these technologies and incorporating them into daily life, paying for subscriptions to AI-powered apps and services. Now consider the optimization potential for large enterprises: cost reduction, margin expansion, throughput improvement. Every company wants this.

The fact that NVIDIA leads in AI-specific chip production explains the sales trajectory. Calling NVIDIA a bubble is wrong. The company validates its valuation every quarter with earnings that no other company in the world is currently matching.

Annual Financial Review

Income Statement

Revenue came in at $60.922B, up 126% year-over-year: an enormous jump driven by explosive demand for NVIDIA’s solutions, especially in the data center segment. Gross profit reached $44.301B, also sharply higher versus the prior period, pointing to improved business profitability. Operating income was $32.972B: NVIDIA continued investing in growth, pushing operating expenses higher, but the revenue surge kept operating profits at a high level. Net income hit a record $29.760B on the back of revenue and profit growth. EBITDA reached $34.480B, reflecting the high operational efficiency of NVIDIA’s business model.

These core financial metrics delivered impressive growth in 2023 and drove the stock performance. The numbers reflect NVIDIA’s leadership in accelerated computing and AI for data centers.

Balance Sheet

Total assets grew to a record $65.73B as of January 2024, up from $41.18B a year earlier, reflecting major investment in business expansion. Cash and short-term investments increased substantially to $25.98B from $13.3B, strengthening the company’s liquidity position. Total liabilities rose to $22.75B from $19.08B, though liabilities as a share of total funding fell to 34.6% from 46.2%, a strongly positive development. Equity nearly doubled to $42.98B from $22.1B, driven primarily by accumulated retained earnings. Total debt declined to $11.06B from $12.03B. Net debt turned negative at a record -$14.93B, a very positive indicator of the company’s liquidity position.

The company’s financial position strengthened materially across all of these metrics over the past year.

Cash Flows

Operating cash flow was a very strong $28.090B, indicating high profitability in the core business. Investing outflow of $10.566B reflects investment in securities and capital expenditures for business expansion. Financing outflow of $13.633B was driven primarily by $12.316B in share buybacks, which exceeded proceeds from new share issuance. Free cash flow came in at $27.02B, an excellent indicator of profitability and cash generation.

As of January 2024, the cash flow profile reflects a mature, high-yield business that is actively reinvesting in growth while simultaneously returning substantial capital to shareholders through buybacks.

Quarterly Financial Review

Income Statement

Revenue reached a record $22.1B, up 22% quarter-on-quarter and 265% year-on-year. The primary driver was the data center segment, where revenue rose 409% year-on-year to $18.4B on strong demand for Hopper architecture products for training and inference of generative AI models and LLMs. GAAP gross margin expanded to 76%, non-GAAP to 76.7%, reflecting the right component cost structure and the high weighting of the data center segment in revenue. GAAP operating expenses rose 6% quarter-on-quarter, non-GAAP 9%, due to investment in compute capacity, infrastructure, and headcount, though high gross profit absorbed these increases without impacting results. Net income hit a record $12.29B for the quarter, up 33% from the prior quarter ($9.243B). Quarterly EBITDA also reached a record, up 30% from the prior quarter ($10.789B), the result of unprecedented revenue growth at high margins.

Q4 FY2024 was an exceptional quarter: new records for net income and EBITDA, driven by explosive demand and high profitability.

Balance Sheet

Total assets grew to a record $65.73B from $41.18B a year earlier. Cash and short-term investments rose to $25.98B from $13.30B. Total liabilities increased to $22.75B from $19.08B, while their share of total funding declined to 34.6% from 46.4%. Equity grew to $42.98B from $22.10B, driven by retained earnings growth. Total debt edged down to $11.06B from $12.03B. Net debt turned negative at a record -$14.93B. The company's financial position strengthened substantially across all key metrics over the past year.

Cash Flows

Operating cash flow of $11.499B is a very strong result: the core business is generating a large cash inflow. Investing outflow of $6.109B reflects ongoing capital investment in infrastructure and growth. Financing outflow of $3.629B is driven primarily by $3.5B in share buybacks, exceeding proceeds from new share issuance. Free cash flow was a positive $11.25B, indicating the company can self-fund its growth from operating cash flows without external financing.

Shareholder Call

Negative

Following US export restrictions introduced in October 2023, NVIDIA did not receive licenses to supply certain products to China and was forced to suspend those shipments. Alternative products not requiring a license have been introduced, but the China business has contracted materially. Demand for NVIDIA products, particularly newer generations, significantly outpaces supply. The company is making large upfront payments to suppliers to secure manufacturing capacity, indicating dependence on their ability to deliver components. Management addressed these issues indirectly, but they could have a modest impact on future results.

Positive

Record quarterly revenue of $22.1B, up 22% sequentially and 265% year-on-year. Full-year revenue reached $60.9B, up 126%. Data center revenue for fiscal year 2024 was $47.5B, more than tripling year-on-year. Hopper architecture demand for AI acceleration and high-performance computing remains very strong, and the networking business exceeded a $13B annualized revenue run rate. The company made significant progress in software and services, with annualized Q4 revenue from that segment reaching $1B. Positive momentum across automotive, healthcare, financial services, and the “sovereign AI” concept for individual countries and regions building their own AI infrastructure. CEO Jensen Huang expressed confidence in continued growth conditions through calendar years 2024 and 2025 and beyond.

Risks

Supply chain and manufacturing capacity: supply shortages against high demand; dependence on component suppliers and their ability to ramp production; potential disruption from geopolitical factors.

Geopolitics: ongoing US export controls on China; operational difficulties in that market; broader instability affecting global supply chains. Taiwan Semiconductors plays an outsized role here, manufacturing the vast majority of NVIDIA’s chips. Any escalation of tensions around Taiwan creates a direct risk to production and supply.

Competition: intensifying competition in AI accelerators from other technology companies; risk of alternative or disruptive technologies emerging.

Technology: challenges in transitioning to new product generations and manufacturing processes; risk of delays in developing new architectures.

Operations: difficulty scaling rapidly into new markets, particularly software and sovereign AI; talent acquisition and retention risks.

Finance: market volatility affecting the stock price; currency risk from global operations.

All of these risks simply need to stay in view, with close attention to what management says about them. At present, the most material risks are supply chain and geopolitics.

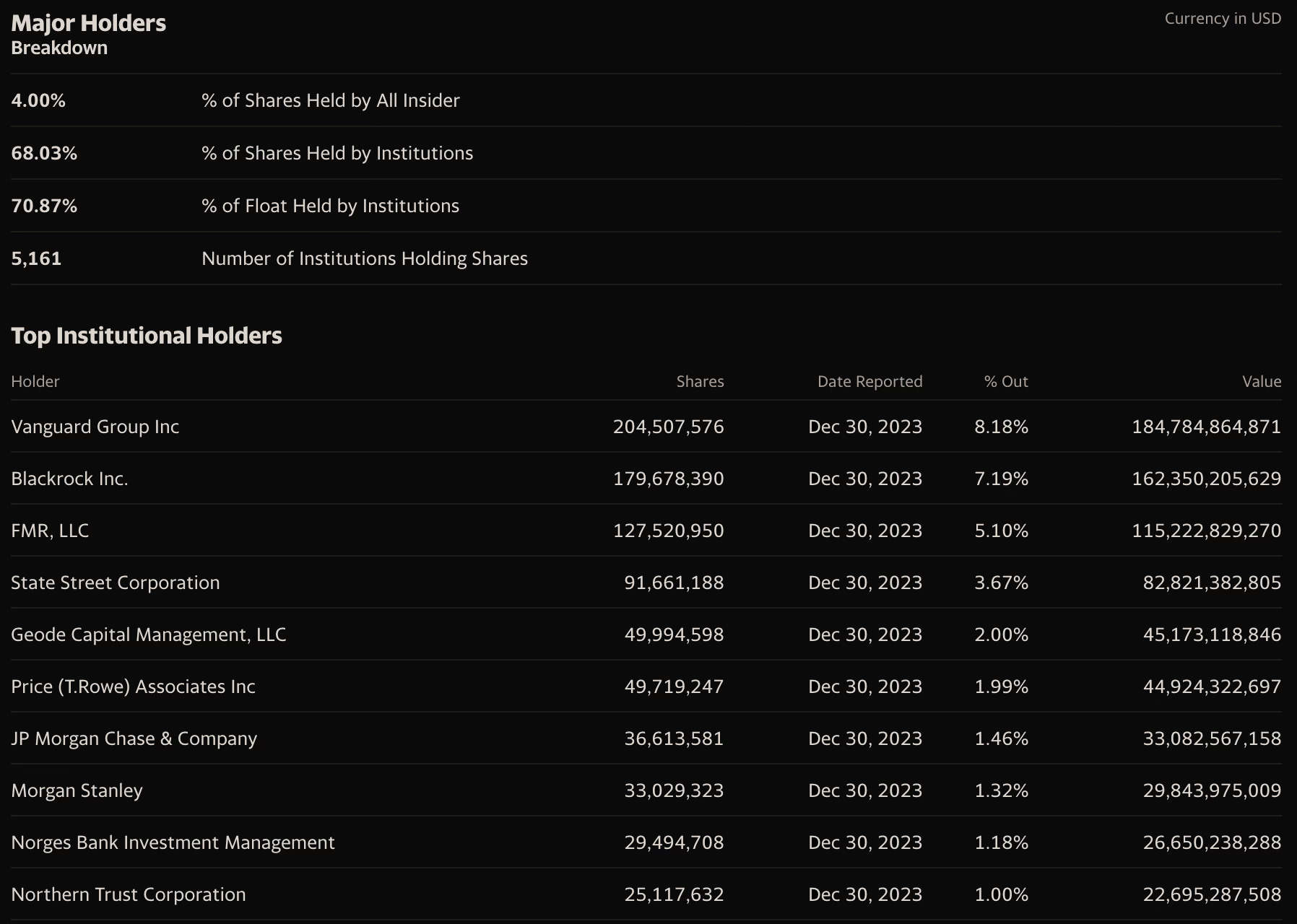

Shareholders

The top holders are major financial institutions: Vanguard Group, BlackRock, and FMR, LLC. Their conviction is evident from the scale of their positions. Insiders hold 4% of shares, while institutional investors hold 68.03%. Over 70% of the total float is held by institutions, meaning roughly 30% of freely tradable shares are available to other market participants.

Conclusion

90% of the AI data center chip market. 80% of the total chip market. Revenue up 265% in the most recent quarter. Record quarterly net income of $12.29B, eight times higher than a year ago. New solutions in development including a superchip for quantum computing and chips for robotics. Growing sales across gaming, automotive, healthcare, and other AI-driven sectors. All one company.

Whatever happens with interest rates, what matters is corporate earnings. If NVIDIA continues to beat estimates, analyst forecasts will be revised upward again. Investors look at current data first, then build forward projections from it. The stock price ultimately follows future results.

If those future results disappoint, the stock will fall sharply. But NVIDIA’s chip architecture is far ahead of the competition. AI technology is still in early stages of deployment and adoption, and the chip giant is in the most advantageous position to capture an even larger share of value as more companies turn to its products to build AI models. With AI integrating across every sector of the economy worldwide, demand for chips will only grow. Every macroeconomic correction, therefore, could be an excellent buying opportunity.