Ukrainian Resources

An assessment of what is happening on Ukrainian territory through the lens of critical and scarce natural resources.

You can talk endlessly about justice, the struggle for independence, free market relations elevated to an absolute. But each of these terms is, in the end, utopian. In one of his articles, Ray Dalio accurately depicted Ukraine’s role in the global geopolitical picture as the starting point for subsequent wars. In this article I’ll try to highlight Ukraine’s significance through the lens of its natural resources.

Energy is an advantage

Energy resources are the foundation of any economy, and their role extends far beyond everyday needs like lighting or heating. Access to energy determines a country’s power and competitiveness on the world stage.

Energy powers factories and enterprises, enabling the production of goods on which the economy depends. Metallurgy, chemical manufacturing, technology: all of these industries require enormous energy inputs. High energy prices raise production and logistics costs, making products less competitive on international markets. This matters particularly for countries that depend entirely on energy imports. Without a stable and affordable energy supply, production stops, GDP falls, jobs disappear, and the economy weakens.

In geopolitics, energy is leverage. Countries with large reserves of oil, gas, coal, or uranium can dictate terms, influence prices on global markets, and shape relations between states. Control over energy resources tends to become a decisive factor in international conflicts and alliances alike.

The transition to cleaner energy is an important factor that deserves its own article. Go deeper and it’s not simply a hyped environmental goal; it’s a necessity for maintaining the economic resilience of many states in conditions of global change. Countries that invest in renewable energy and energy-efficient technologies gain a strategic advantage, reducing dependence on oil and gas price volatility and minimizing geopolitical and climate-related risks. Apply basic logic: even building and manufacturing the new technologies that will accelerate the transition to “green” energy requires, again, energy. For that reason, the transition path will likely take several decades.

So if any energy source capable of increasing productivity and generating profit matters, what energy resources does Ukraine actually have?

A graveyard of resources

Ukrainian territory holds strategic importance in the global economy because of its resources. It contains significant reserves of oil, natural gas, and coal, which form the foundation of Ukraine’s energy potential. It also holds minerals critical to modern industry, including rare-earth metals in high demand on global markets.

Ukraine ranks among the world leaders in assessed mineral wealth. The country is home to 117 of the 120 most widely used minerals, holds the largest assessed uranium reserves in Europe, the second-largest reserves of iron ore, titanium, and manganese, and the third-largest reserves of shale gas.

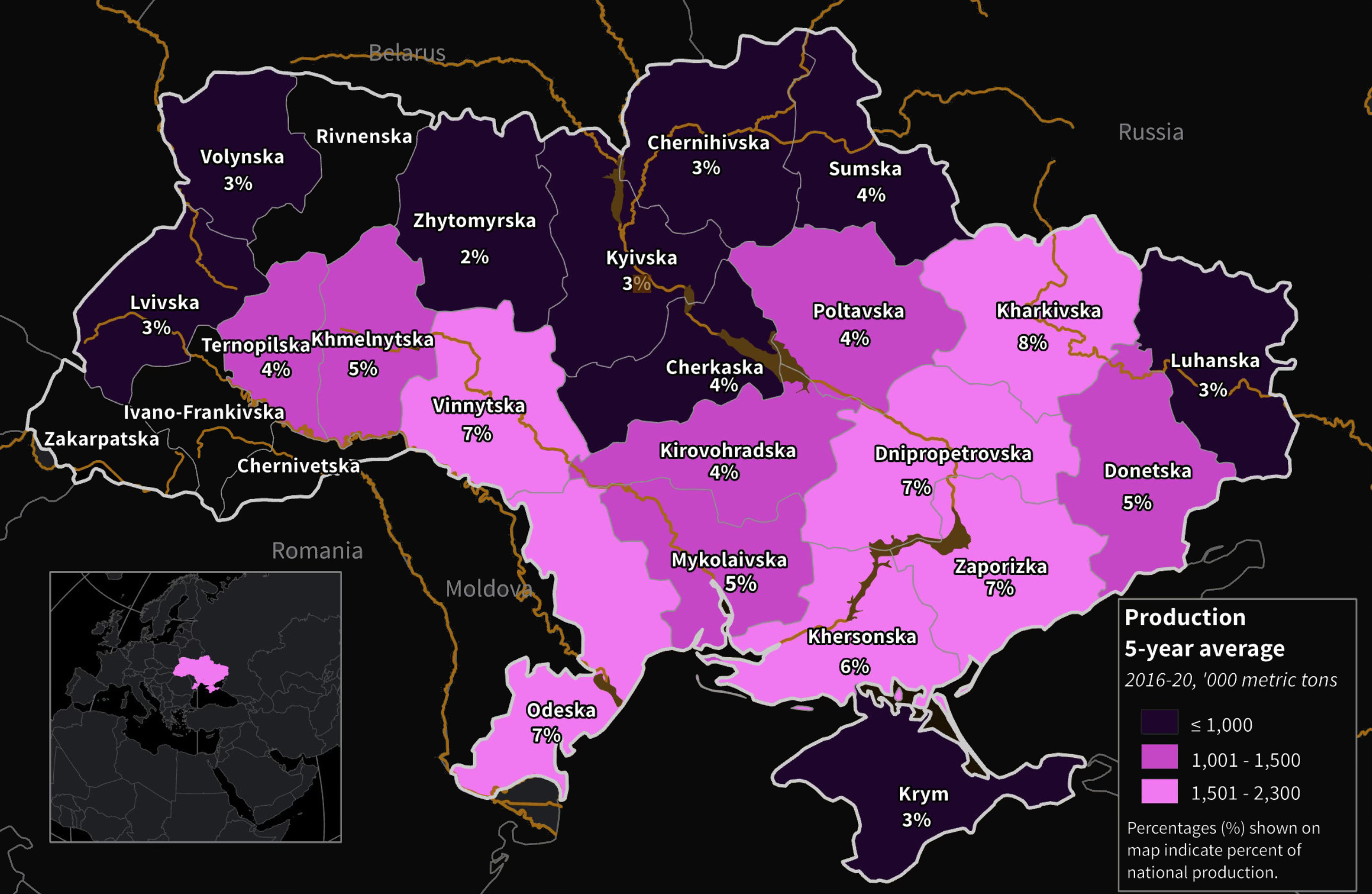

The eastern and southern regions of Ukraine are key agricultural zones, as noted by the USDA. Ukrainian wheat, corn, barley, and sunflower supply food to many countries around the world. The war has not only disrupted the extraction of these resources but also blocked export routes, threatening global food supply chains. Supply route blockades imposed by several European countries have compounded the problem.

Setting aside agriculture and coal, many of Ukraine’s resources remained underdeveloped and unstudied throughout the Soviet period and much of the post-Soviet era, due to a lack of technology and investment. This continues to play an enormous role today, keeping the “agrarian superstate” label in place. Most of the population still believes the country’s exclusive wealth lies in the fertility of its land, but that is only a portion of the resources in use and in plain sight. Let’s go through them in order.

Gas relations

Natural gas and the pipelines carrying it bound Russia and Ukraine within the Soviet space without any friction (logical under a communist regime). But after Ukraine’s independence, Ukraine became, in part, a competitor to Russia. Gas imported from Russia was Ukraine’s primary energy source and played a decisive role in powering its economy and industry for an extended period. The transit fees Ukraine collected for transporting Russian gas to Europe through its pipelines and territory were an important source of budget revenue.

Access to Europe via the Ukrainian pipeline system was critical for Gazprom, since the European market was its main revenue source. This meant Russia depended on Ukraine. In 2005, 80% of Russia’s gas exports to Europe passed through Ukrainian pipes. Under the Soviet Union, the question of gas supplies never arose. Under Ukrainian independence, it became one of the central issues.

Political fault lines in Ukraine then followed, tied to two poles. Simply put: Yanukovych represented Kremlin interests; Yushchenko embodied a European political course, his wife having previously worked in the administration of U.S. President Reagan.

Yushchenko’s victory in Ukraine’s presidential election led to difficult negotiations over natural gas prices. Until that point, Ukraine had been paying Russia roughly one-third of what EU countries paid. There was no point in subsidizing Ukraine with cheap gas given that even with subsidies it had accumulated enormous debts for gas deliveries, and was now governed by a president seeking independence from Russia.

One of the Kremlin’s political objectives became control over the Ukrainian gas transport system, critical for moving Russian gas to Europe. For Ukraine, the same system was an equally important political and economic instrument.

Without reaching an agreement, on January 1, 2006, Gazprom cut off supplies destined for Ukraine. Ukraine then began drawing on gas intended for the eurozone, which reduced supplies to Europe and caused friction in relations between Russia and the EU. Western countries read this as a demonstration of energy power as a political tool.

After that episode, both sides reached a new agreement. Ukraine retained control over its pipeline system, but the company RosUkrEnergo continued to play a significant role in gas relations.

The same scenario played out on January 1, 2009, when Russia again cut off supplies destined for Ukraine, claiming Ukraine was stealing gas meant for Europe. Gas deliveries to Europe also stopped as a result. Ukraine and the eurozone managed the situation using stored reserves, after which a new agreement was reached. Cutting supplies doesn’t serve Russia’s interests either.

To diversify its supply routes around Ukraine, Russia built other pipelines: Yamal-Europe through Poland, and Blue Stream running from Russia under the Black Sea to Turkey. But Nord Stream, between Russia and Germany along the Baltic seabed, was far more significant. Germany is the largest economy in the EU, and a direct route lowers gas transport costs. It allowed Russia to sell gas to Germany without paying transit fees to intermediary countries like Ukraine or Poland, making the route more profitable.

The eurozone’s goal, meanwhile, was flexibility and diversity in energy supply, to avoid being locked into imposed prices and conditions. European companies began interconnecting pipelines to allow supply routing to shift as needed. Emphasis was also placed on building liquefied natural gas (LNG) terminals and creating larger gas storage facilities. This expanded Europe’s ability to receive gas not just by pipe but by sea, with the U.S. becoming the main supplier via that route.

European policy pushed to move away from old contract structures in which gas was sold on terms of up to 20 years or more, with prices tied to oil. The EU instead sought to introduce more competitive and transparent markets where buyers and sellers could interact freely. This meant a transition from long-term, fixed supplier-buyer relationships toward markets where conditions and prices could be adjusted flexibly in response to market conditions.

In 2013, Ukraine found itself at a crossroads between East and West, and on the surface it looked purely like a trade question. On one side, Russia was actively promoting the “Eurasian Economic Union,” a grouping of post-Soviet countries under its leadership with a common tariff regime and a unified economic space. At the same time, Ukraine was negotiating an association agreement with the EU that would entail deeper economic integration with Europe.

The problem: these two paths were completely incompatible. Ukraine could not be part of both systems simultaneously, since the tariff rules and economic conditions of the EU and the Eurasian Union were mutually exclusive. If Ukraine chose integration with the European Union, it would have to abandon participation in the Kremlin’s Eurasian project. Beyond that, through integration into Europe, Russia would have gained a new competitor on several fronts at once. The key one: gas.

Ukraine was trying to increase its economic and energy security by developing its own natural resources and diversifying away from Russian imports. In August 2012, the government selected ExxonMobil and Royal Dutch Shell to lead development of the Skifske deepwater natural gas field on the Black Sea shelf, alongside Romanian OMV Petron and the national joint-stock company Nadra Ukrainy.

In 2013, a large-scale oil and gas privatization began. That same year, at the World Economic Forum in Davos, Shell signed a deal with Ukraine to extract shale gas from the Yuzivska field (Donetsk and Kharkiv regions), one of Ukraine’s largest oil and gas deposits. Resource volumes at that site alone exceed 1 trillion cubic meters. Chevron subsequently signed a shale gas extraction deal at the Olesska field (Lviv, Ivano-Frankivsk, and Ternopil regions).

This “European course” was not in Russia’s interest, since Ukraine’s gas reserves in the Olesska field alone could have satisfied three years of EU demand (approximately 3 trillion cubic meters).

Kremlin representatives understood that signing the EU association agreement would exclude Ukraine from the Eurasian Economic Union. Yanukovych consequently walked away from the agreement, receiving a $15 billion “gift” loan from Russia in return. What followed was the clash of interests and the widely known events on the Maidan. All agreements with foreign energy companies on gas extraction were subsequently severed with the annexation of Crimea and the start of the war in the Donbas in 2014.

Work on Nord Stream 2 began in late 2015, four years after the first pipeline launched. But the second project faced resistance. Much of the opposition was directly connected to the situation in Ukraine. Criticism came from Poland and the Baltic states, as well as from the European Union itself: a sharp contrast to its earlier support for Nord Stream 1.

On one side sat concerns about increased dependence on Russian gas and potential geopolitical consequences. On the other, economic interests and the desire for stable energy supply also played a substantial role in decision-making. Some leaders, including German Chancellor Angela Merkel, treated Nord Stream 2 as a purely commercial project whose decisions should be made by the participating companies, not by politicians.

But the pipeline was not “just an economic project,” as Chancellor Merkel said. Political factors were also built in: ensuring the continuation of gas transit through Ukraine, to avoid depriving it of transit revenues and creating economic pressure on the country. Without that provision, the new pipeline would have allowed supplies via Ukraine to be reduced to minimal volumes, barely enough to keep the old routes technically operational. Germany, naturally, gained a key benefit from this arrangement: the ability to present itself as a partner to everyone.

In December 2019, construction of Nord Stream 2 was in its final stages. On December 20, Russia and Ukraine signed an agreement guaranteeing five years of natural gas supplies to Europe via Ukraine, securing a level of transit income for Ukraine. Russia also agreed to pay Ukraine $3 billion in settlement of an arbitration claim Ukraine had won against Gazprom. That amount was roughly equivalent to one year of transit revenue for Ukraine. The war was ongoing throughout this entire period, worth keeping in mind.

Today Europe is part of a global market with a wide range of gas supply options. As a result of the war, Ukraine is forced to import gas from Slovakia, Hungary, and Poland. It’s understood that part of what is imported is Russian gas mixed with LNG from other countries. All of this continues today. But 2025 is considered the deadline on supplies, around which debate is also ongoing.

Beyond that, as noted earlier, Ukraine holds significant natural gas production potential. Approximately two-thirds of the country’s total domestic gas demand is met by local production. Ukraine may hold the largest natural gas reserves of any European country, opening prospects for increased domestic output and exports in the future.

Most of current gas production in Ukraine (roughly 80%) is carried out by the state gas company. The second-largest producer is a private company called Burisma. It accounts for only 5% of domestic output but acquired outsized notoriety outside the energy sector. This is the company Donald Trump wanted investigated in Ukraine because Hunter Biden, son of then-Vice President Joe Biden, sat on its board of directors.

All of that led to Trump asking President Zelensky in a July 2019 phone call to investigate the Bidens’ activities in Ukraine. That call and the subsequent actions of the Trump administration became the subject of a congressional investigation, ultimately leading to Donald Trump’s first impeachment in December 2019. Complex, I understand, but all of these political actions only underscore the importance of Ukraine’s energy sector as a sphere of influence.

Oil

There isn’t much publicly available information about Ukrainian oil and its quantities. The International Energy Agency (IEA), for instance, notes that “Ukraine has only small oil reserves (exact volumes are a state secret), and legislation on emergency oil supplies that would regulate the use of strategic oil reserves in the event of supply disruptions does not exist.”

In the largest digital atlas (SOAR), I came across maps that also indicate oil deposits.

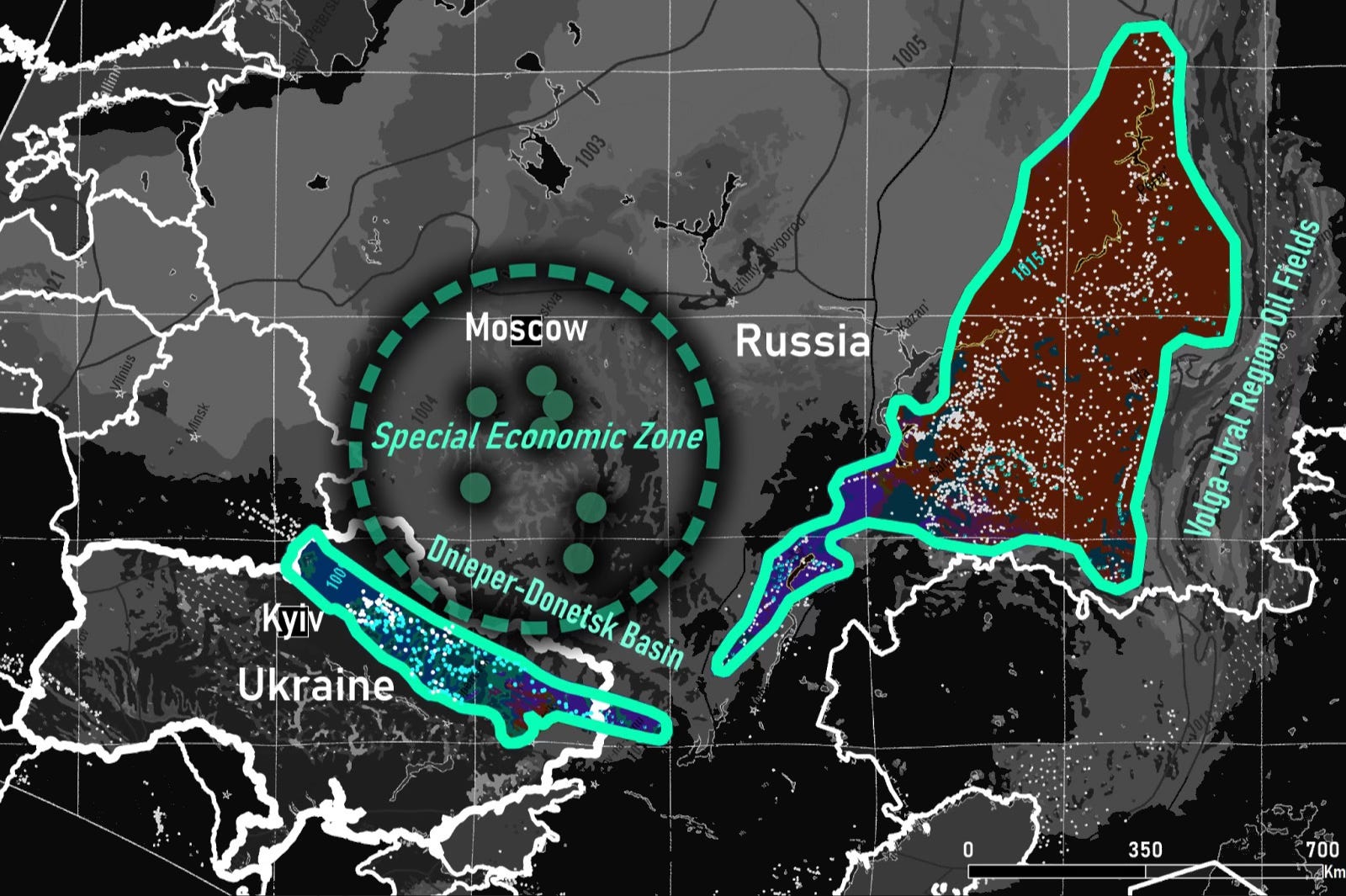

In the right portion of a map from the complete geological map of the former Soviet Union, the location of oil and gas fields is visible in the northeastern region of Ukraine, where approximately 2,000 km of border with Russia runs through the Dnieper-Donetsk geological basin: the primary oil province of Eastern Europe. Oil fields are marked with white dots, gas fields with blue.

At a minimum, it’s reasonable to accept the fact that oil exists on Ukrainian territory. The exact reserve quantities are almost certainly not findable in open sources.

Uranium

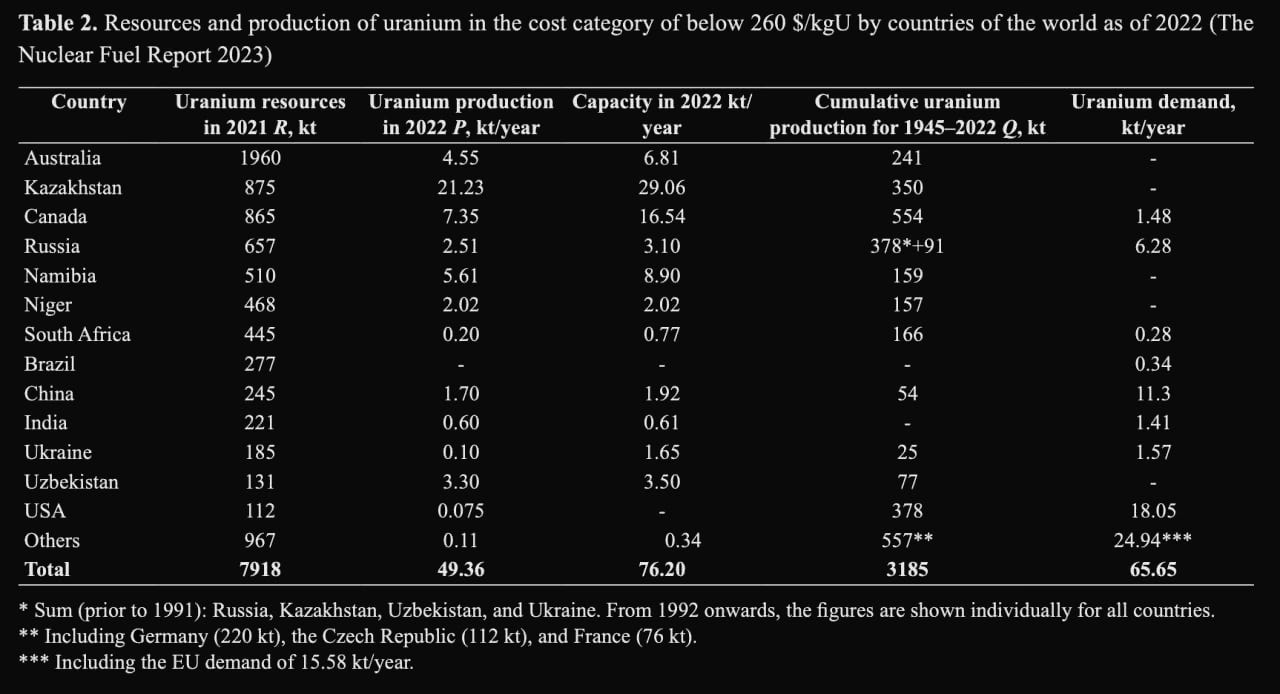

Nuclear energy is expanding rapidly worldwide, particularly in countries like China, India, and the United States. Despite these trends, natural uranium production has been declining in recent years, and the gap between production and consumption grows each year. That gap is approximately 20,000 tonnes of uranium annually, currently being filled by existing stockpiles. This situation could lead to a sharp spike in uranium prices in the near future, once stockpiles begin to run out: they are not unlimited. Below is a list of countries with the largest uranium deposits and their metrics on resource reserves, production capacity, consumption, and deficit.

According to the IAEA, Ukraine has been a member of that organization since its founding. But Ukraine’s uranium resources have not been fully explored or studied. All deposits are located in the Ukrainian Shield and the Dnieper-Donetsk Depression. The estimated uranium resource base: 185 kilotons, making Ukraine the largest uranium deposit in Europe and the 11th largest in the world.

Ukraine has a highly developed nuclear energy sector, generating more than 55% of total electricity output. At the same time, domestic uranium mining can meet only 30% of its needs. Energoatom purchases the remaining uranium from other countries. So, despite holding the largest deposits, the country lacks the technology and investment to extract uranium at a scale that would cover 100% of domestic needs, let alone export.

With energy consumption growing in developed economies and uranium deficits widening, uranium could become one of the key geopolitical objectives.

Critical raw materials

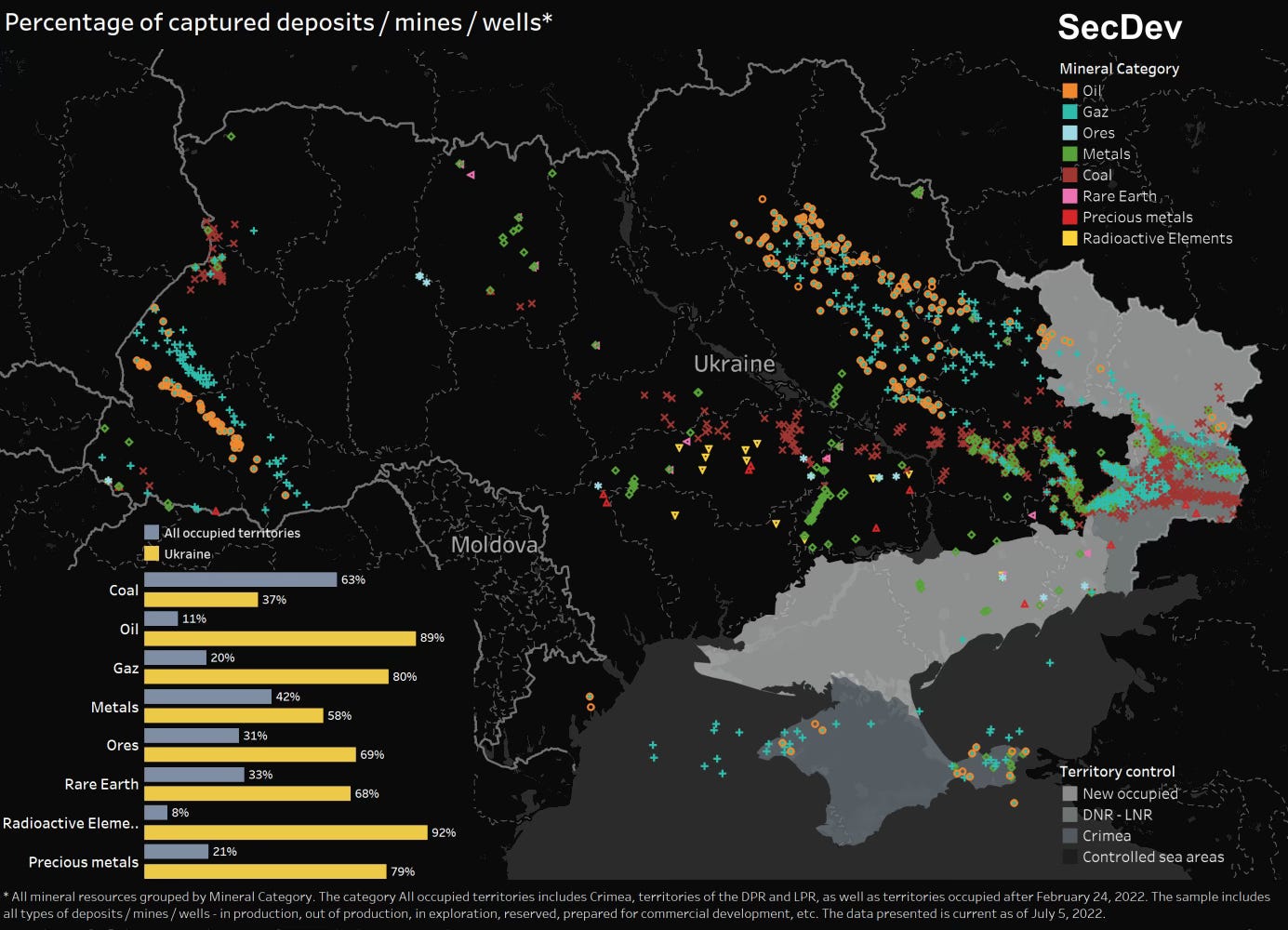

More recent research conducted by SecDev showed that the territories currently under Russian occupation contain hydrocarbons valued at more than $12 trillion, while the total estimated value of Ukraine’s national resources is assessed at over $26 trillion. These are precisely the figures cited by senior U.S. Senator Lindsey Graham in his Face the Nation interview:

“Ukraine has critical minerals worth somewhere between $10 and $12 trillion dollars. They could be the richest country in all of Europe. I don’t want to give that money and those assets to Putin so he can share it with China.”

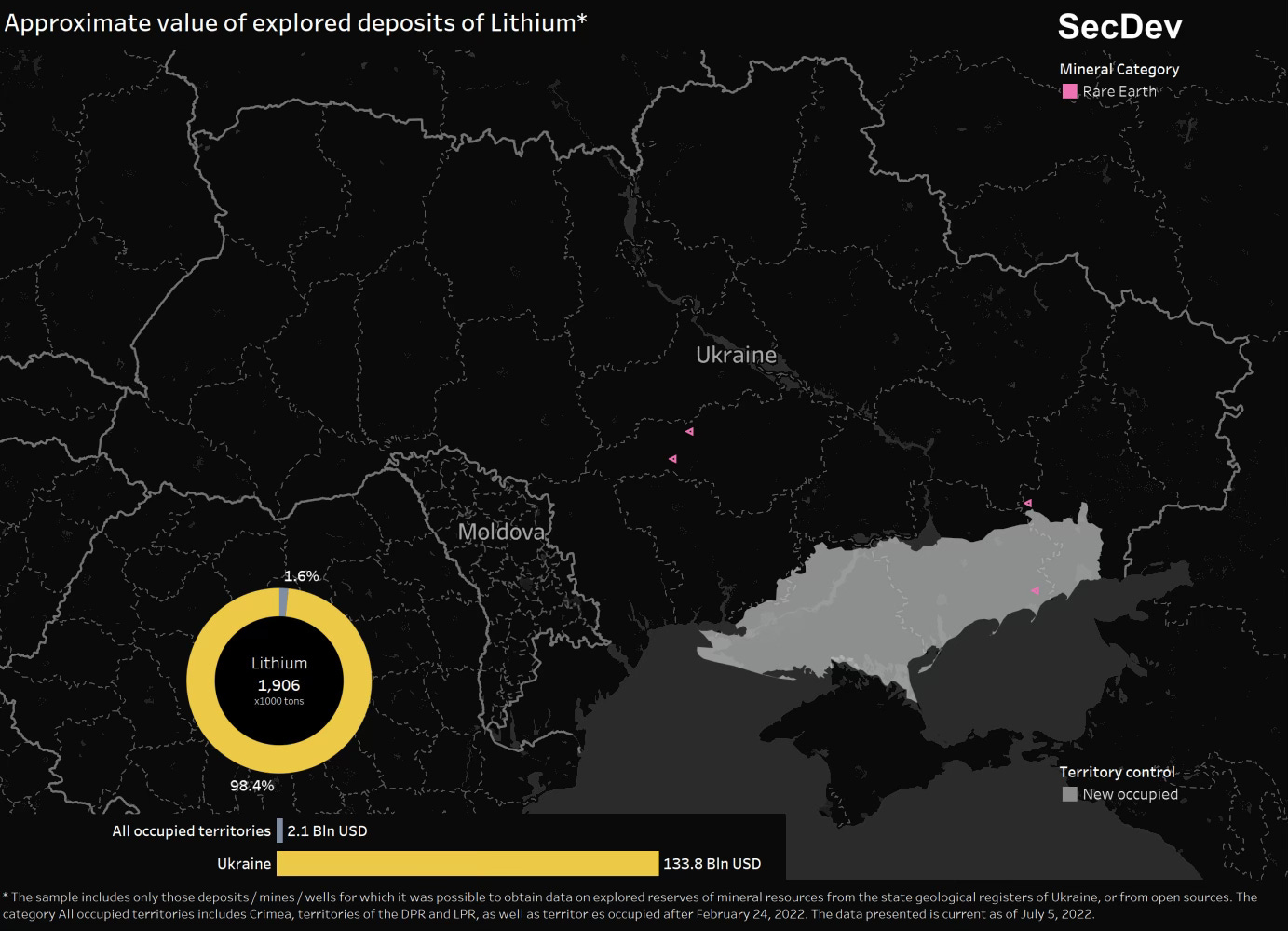

Research by the Ukrainian Geological Survey indicates that ancient rock formations of the Ukrainian Shield conceal lithium deposits with enormous potential. These deposits are located primarily in the area around Mariupol, a port city in the Donbas. The New York Times published the same findings.

In 2021, the EU was already attempting to diversify away from China and Russia through a “strategic partnership” with Ukraine, since Europe is critically dependent on raw material imports from China, which accounts for 98% of supply.

The bulk of these materials is used in electric vehicle batteries, smartphones, and wind turbines. As of 2021, the EU’s critical raw materials list comprised 30 materials, including rare-earth elements, bauxite, lithium, and titanium. At least 20 of them are found in Ukraine.

China has become the global leader in the extraction and production of critical resources and has gained further geopolitical leverage as a result. This gives Beijing the ability to apply pressure on the economic and political decisions of other countries.

Protectionism is rising elsewhere as well: Zimbabwe and Chile are restricting lithium exports, while Indonesia and the Philippines are tightening control over nickel supplies. All of these moves are significantly disrupting global supply chains, making them less stable and predictable. With the full-scale war in Ukraine, prices for lithium and nickel, used in electric vehicle manufacturing and renewable energy development, rose sharply.

Platinum group metal prices also increased: these play a key role in the development of the hydrogen economy. The consequences of these processes are already being felt worldwide.

European industry, dependent on critical raw material imports, is beginning to deteriorate. Electric vehicles produced in the EU and the U.S. are gradually becoming uncompetitive compared to their Chinese counterparts due to the absence of alternative raw material supply routes. That is just one example of how dependence on a single supplier of critical resources can undermine the economic stability of entire countries and entire industries.

Conclusion

Ukraine has become the epicenter of geopolitical change, where the interests of autocratic regimes and democratic alliances have collided. Control over energy, food, and mineral resources is the primary objective, since each of these strategic resources is present in Ukraine in abundance.

Tracking all of these interconnections makes the logic of Russia’s and China’s actions more legible: both are working to strengthen their positions on the global stage in economic and geopolitical terms. Control over natural resources is the core strategic objective. This explains the “military competition” between autocratic and democratic states, in the Middle East or Africa for instance, where energy and rare-earth resources are also concentrated.

Historical, cultural, religious, linguistic, ethnic, and other factors, however significant, serve merely as tools for managing human resources. The true cause of conflicts is control over scarce natural resources. That is the key to global dominance.

The question arises: "Can the parties abandon strategic objectives in favor of temporary compromises?" The answer, I think, is obvious.