Unsafe Zone

"Don't Make the Mistake of Thinking That What's Now Happening is Mostly About Tariffs" — Ray Dalio.

Recent political and economic events have shaken the entire world. Many people have responded by mocking Trump’s actions and dismissing them as the foolishness of a dim-witted man.

The goal of this article is to look at the situation not from the perspective of someone reading cartoon headlines and memes, but from the perspective of someone willing to examine what’s happening with a cold head.

A Brief Primer on Deficits

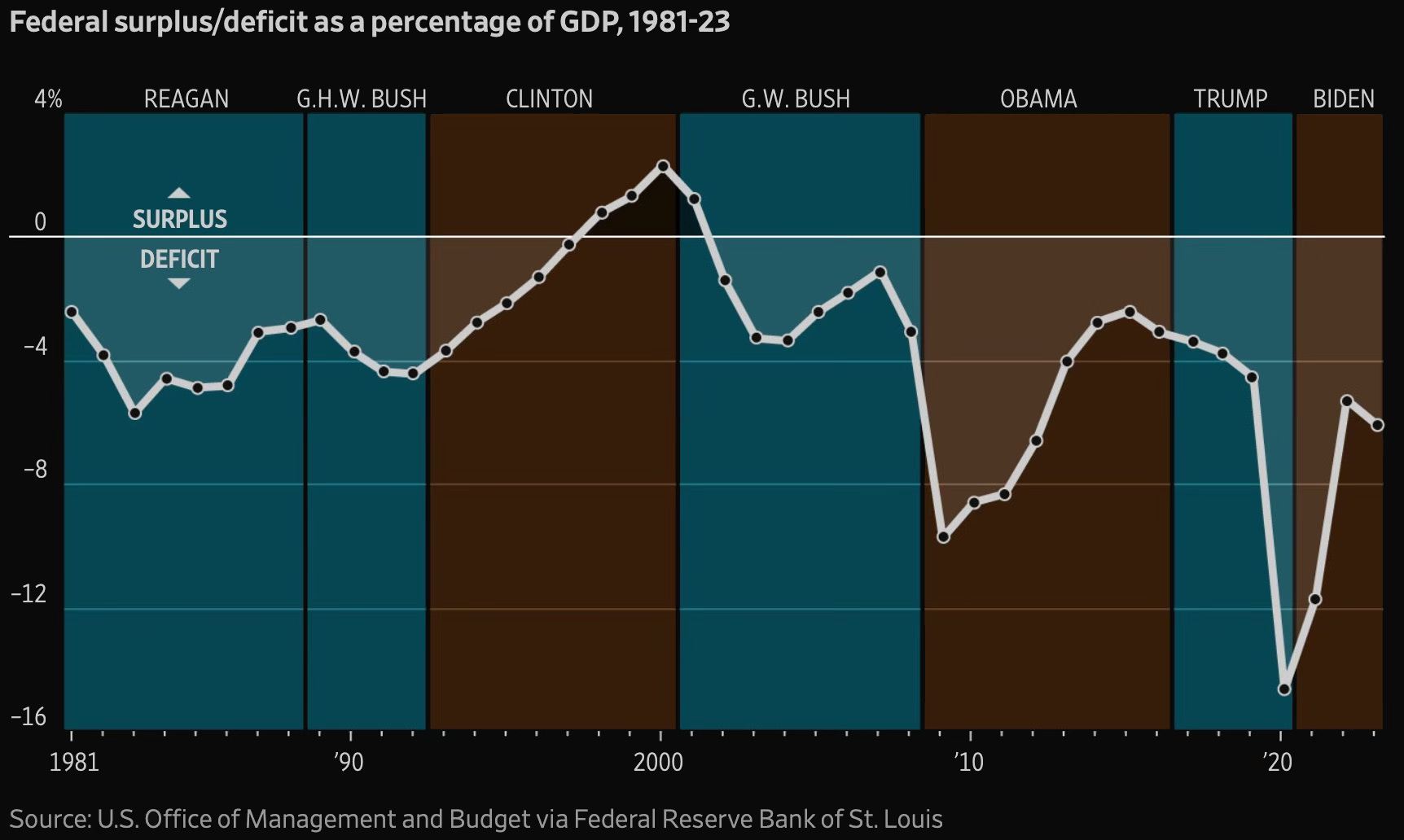

Every so often, alarming news surfaces about the U.S. national debt hitting its ceiling, the budget falling apart, states unable to pay their bills, and so on. All of it sounds dramatic, but let’s be honest: this isn’t just exaggeration, it’s a myth packaged in a scary headline. It repeats year after year, decade after decade.

Imagine taking out a loan. But there’s a catch: you print the currency for that loan yourself. Literally. You just fire up a home printing press and pull out money whenever a payment is due. Sounds like fraud? Maybe. But if you’re the U.S. government, it’s called monetary policy.

Your “bank” (the rest of the world) doesn’t just accept this money, it eagerly accumulates it. Because these aren’t just dollars, they’re the global reserve currency, used in international trade, savings, and even currency interventions. The entire rest of the world extends credit to the U.S. in dollars that the U.S. prints itself.

This arrangement is the product of a post-war geopolitical construction. After World War II, the U.S. found itself in a unique position: the largest economy left undamaged by the war, with the most powerful industrial base, enormous gold reserves, and critically, a dollar pegged to gold. That was the Bretton Woods system, where the dollar became the anchor of the global financial architecture.

Then in 1971, President Nixon closed the “gold window.” The dollar, and with it every other currency, permanently lost its peg to gold. From that point on, paper money existed purely by government decree, not through any backing, creating an era of financial flexibility where constraints became political rather than material. The dollar’s gold peg under Bretton Woods was, in essence, a conditional formality. Yes, the dollar was officially convertible to gold, but in practice money was already being issued in volumes far exceeding the gold backing. Gold was a symbolic pillar of confidence, not an actual brake on the printing press. So the abandonment of the gold standard in 1971 didn’t change the underlying reality: it merely removed the need to pretend that reserves placed any limits on money supply. The last risk of the U.S. running out of gold disappeared, and along with it went the external constraints on financial expansion.

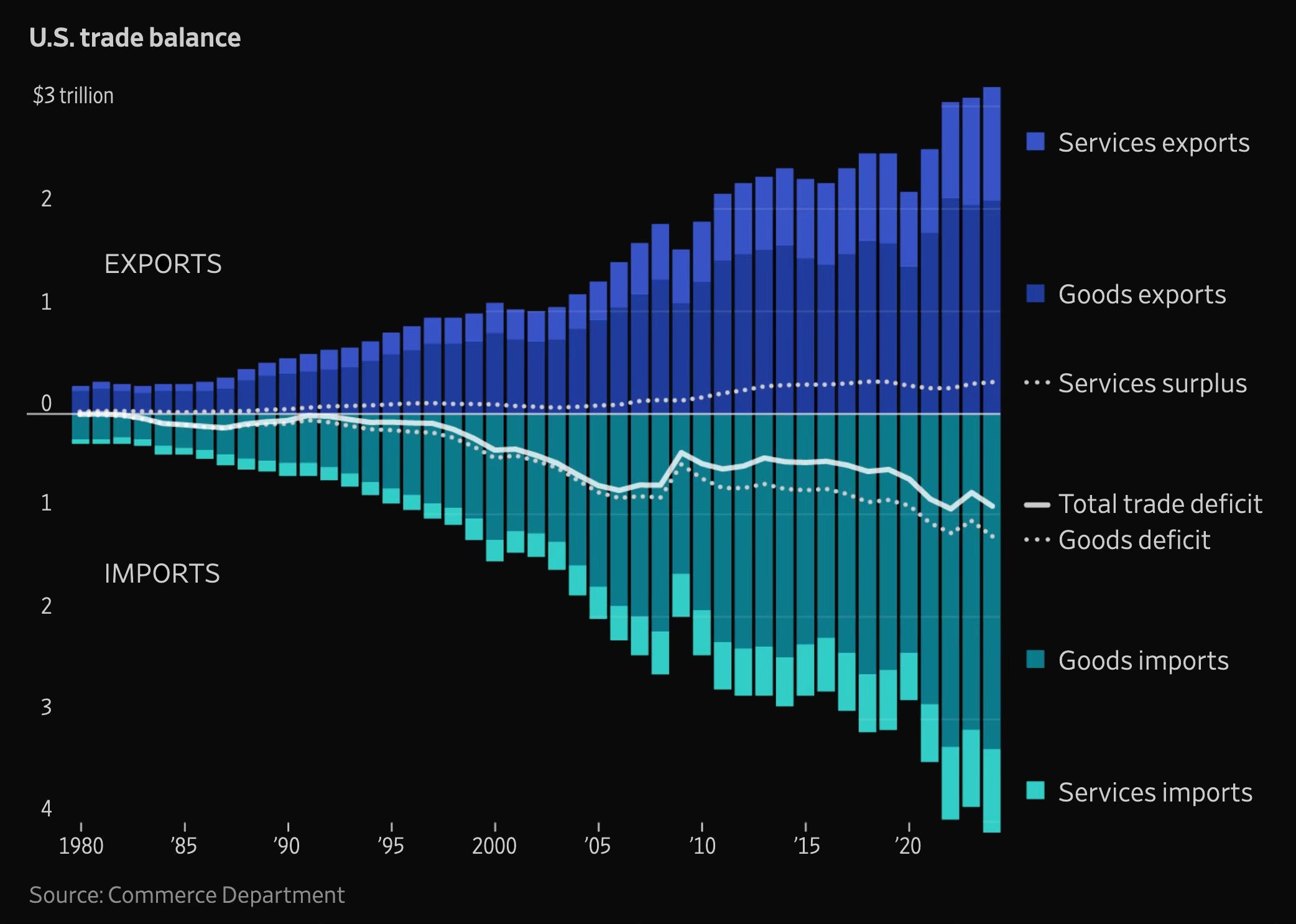

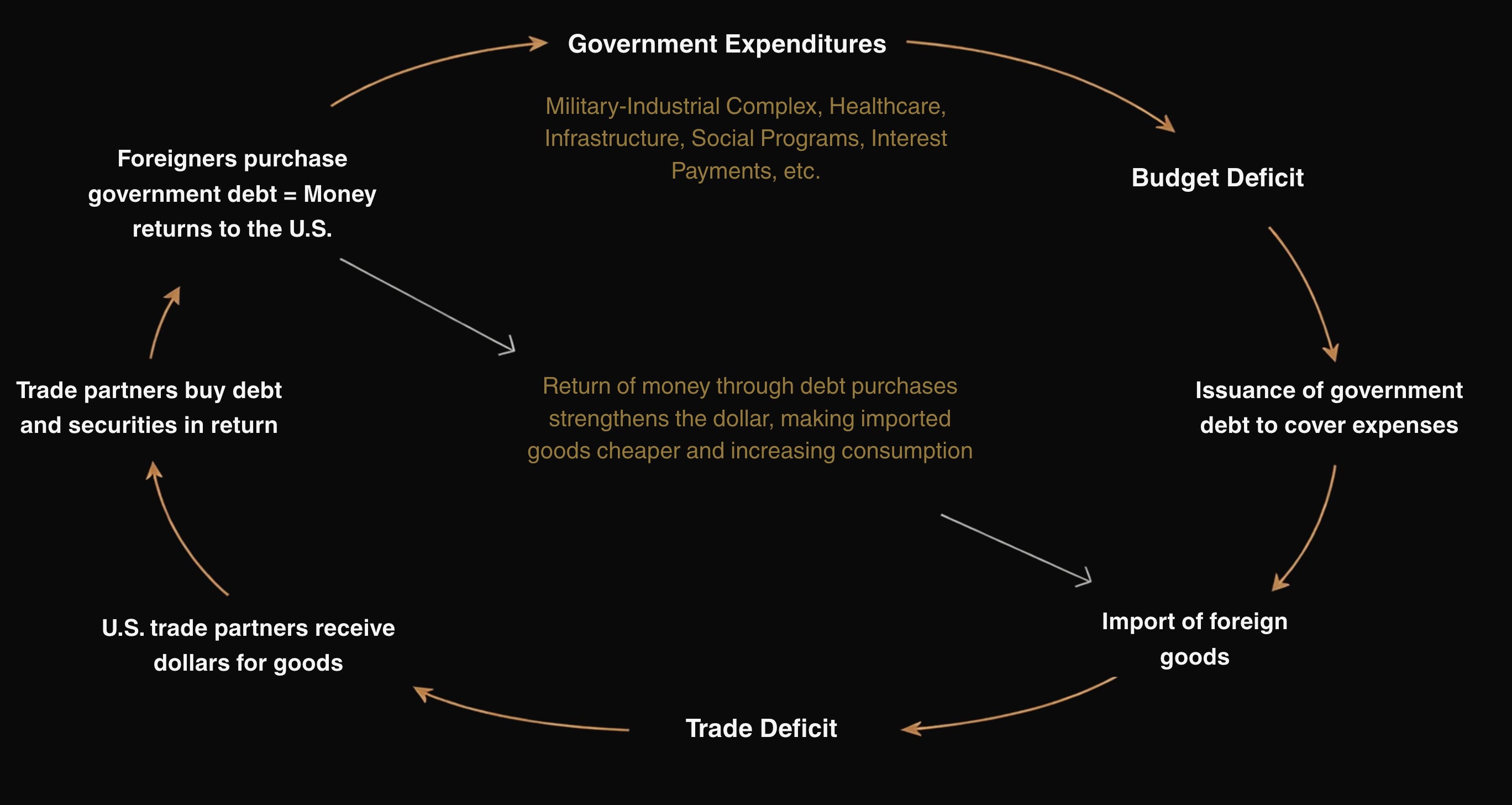

Over time, the U.S. became not only the issuer of the world’s primary currency but also its primary consumer. Its manufacturing base partially relocated to Asia (mainly China), while America imported ever more goods, paying for them with its own dollars. This gave rise to the growth of the U.S. fiscal and trade deficits.

These deficits are not a malfunction of the system. They are its foundation. To sustain economic growth, employment, and consumption, the government spends more than it collects in taxes: a fiscal deficit.

That spending goes toward infrastructure, healthcare, defense budgets, and social programs, maintaining domestic demand. At the same time, the American economy runs on mass consumption: people buy a lot and often, but a large share of those goods is produced abroad. This creates a trade deficit, where the U.S. imports more than it exports.

To finance both deficits, the U.S. issues debt: Treasury bonds, bought by both private investors and foreign governments. Why? Because those investors end up holding dollars from selling goods to the U.S., and those dollars need somewhere to go. If China sells a massive shipment of iPhones to the U.S. and receives dollars in return, what do you do with those dollars? That’s why U.S. government debt remains the most liquid and reliable asset.

The result is a kind of closed loop:

Both deficits, fiscal and trade, grow in sync, feeding each other. More spending means more imports. More imports mean more offshore dollars recycled through bond purchases, creating room for new spending. The more America consumes, the more credit it receives. The more credit it receives, the more it can consume. At present, consumption accounts for 70% of U.S. GDP.

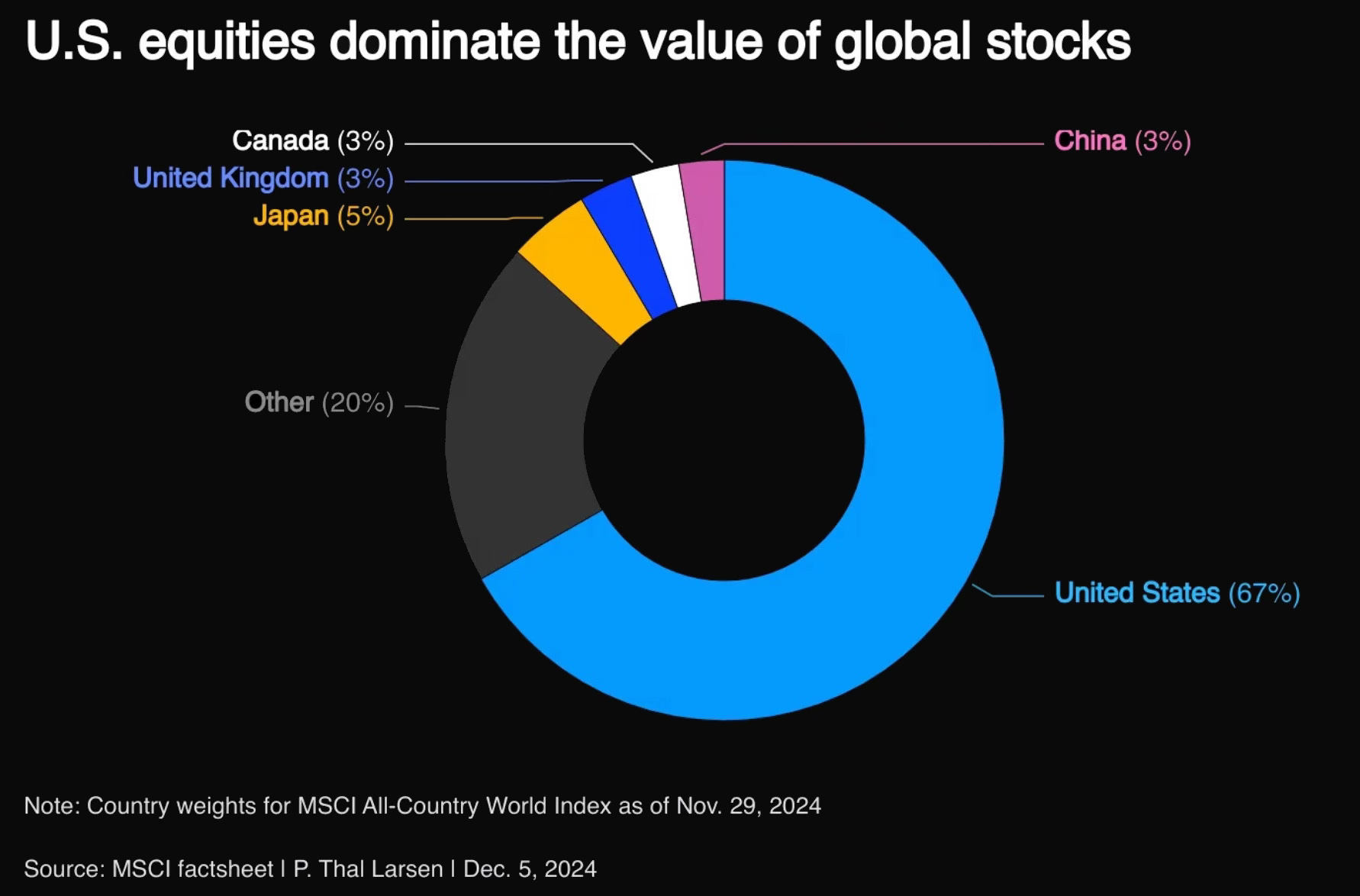

The U.S. fiscal and trade deficits, together with the growth of public debt, form the foundation of the current global economic order. They facilitate the accumulation of financial assets domestically, support the consumption and welfare of American citizens, finance allies (including in defense), and feed the global financial system by generating demand for dollars and American assets worldwide. This is partly why the U.S. accounts for roughly 67% of global equity market capitalization.

So if the carousel has been spinning this long, why worry?

Debt Risks

Let’s look at this from several angles, not just one.

First: Warren Buffett’s view on the U.S. deficit spiral. Back in 2003, Warren wrote an interesting letter that captured the real problem of mounting debt and deficits through a single parable about two fictional island nations: Squanderville and Thriftville (a reference to the “Triffin dilemma”).

In the parable, the residents of Squanderville lived lavishly (consuming a lot, producing little). They were accustomed to a high standard of comfort, but covered their needs through imports from the neighboring island of Thriftville, where people lived modestly, worked hard, and saved. Squanderville couldn’t pay for imports with its own goods: it barely had any. Instead, it paid with IOUs and sold off portions of its assets (land, businesses, bonds). Thriftville happily accepted these assets, since they generated income.

Over time, Thriftville’s residents became owners of an ever-larger share of Squanderville. Their ownership stake grew. They began to hold buildings, factories, banks, even land. Squanderville still lived well, but no longer on its own means: it was selling its future. In that future, Thriftville’s thrift turned into economic dominance, while Squanderville’s extravagance turned into a loss of control over its own country.

Through this metaphorical parable, Buffett argues that the current generation in the U.S. benefits from overconsumption, but future generations will be forced to pay for it through interest on debts and dividends to foreign asset owners, while also suffering the consequences of currency debasement. It sounds strange, given that the U.S. still dominates globally, backed by its growing economy. But look at the actual ownership data Buffett points to:

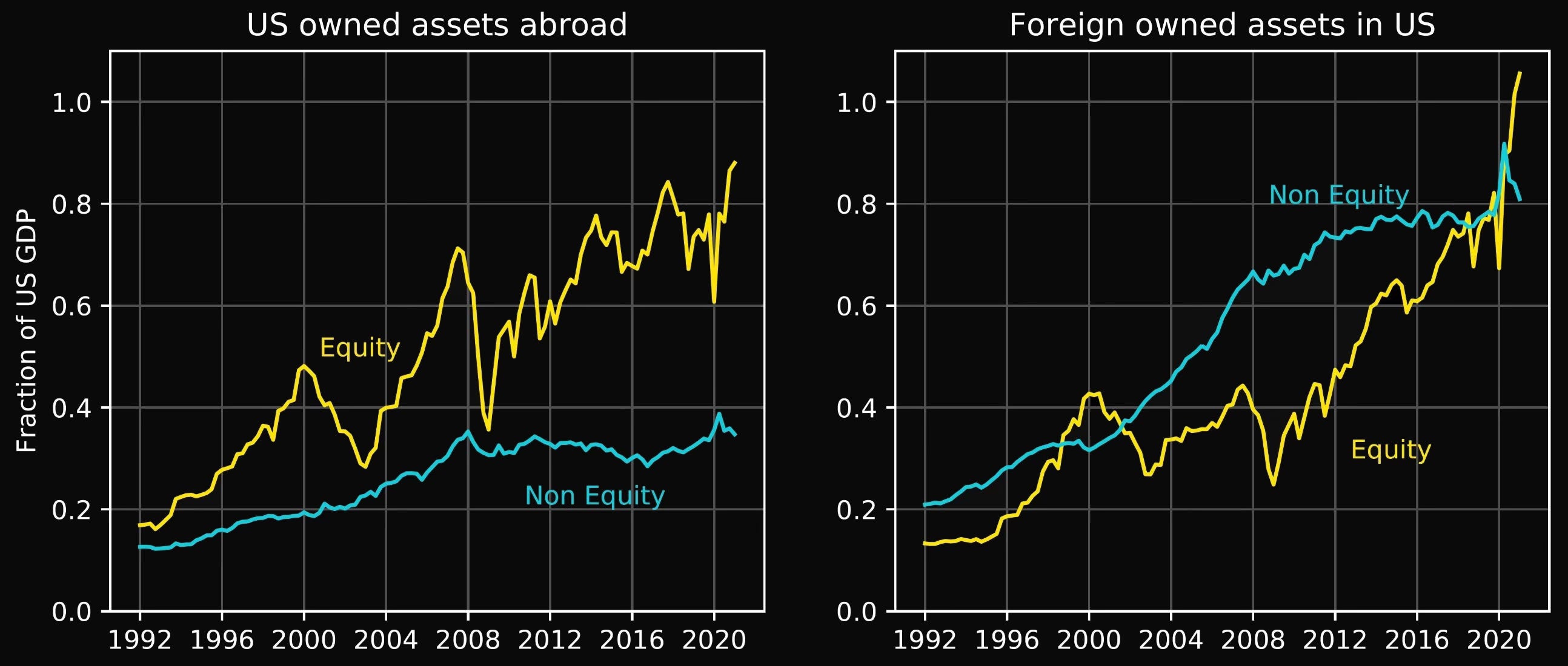

Foreign ownership of American assets and liabilities has exceeded 100% of U.S. GDP. Looking specifically at equities, the share of U.S. companies owned by foreign investors has risen sharply since 1945 and reached 18%.

This indicates that as fiscal and trade deficits grow, so does the volume of foreign capital in the American economy, and that share will keep rising as public debt and interest payments increase. Buffett’s Squanderville parable is not empty noise.

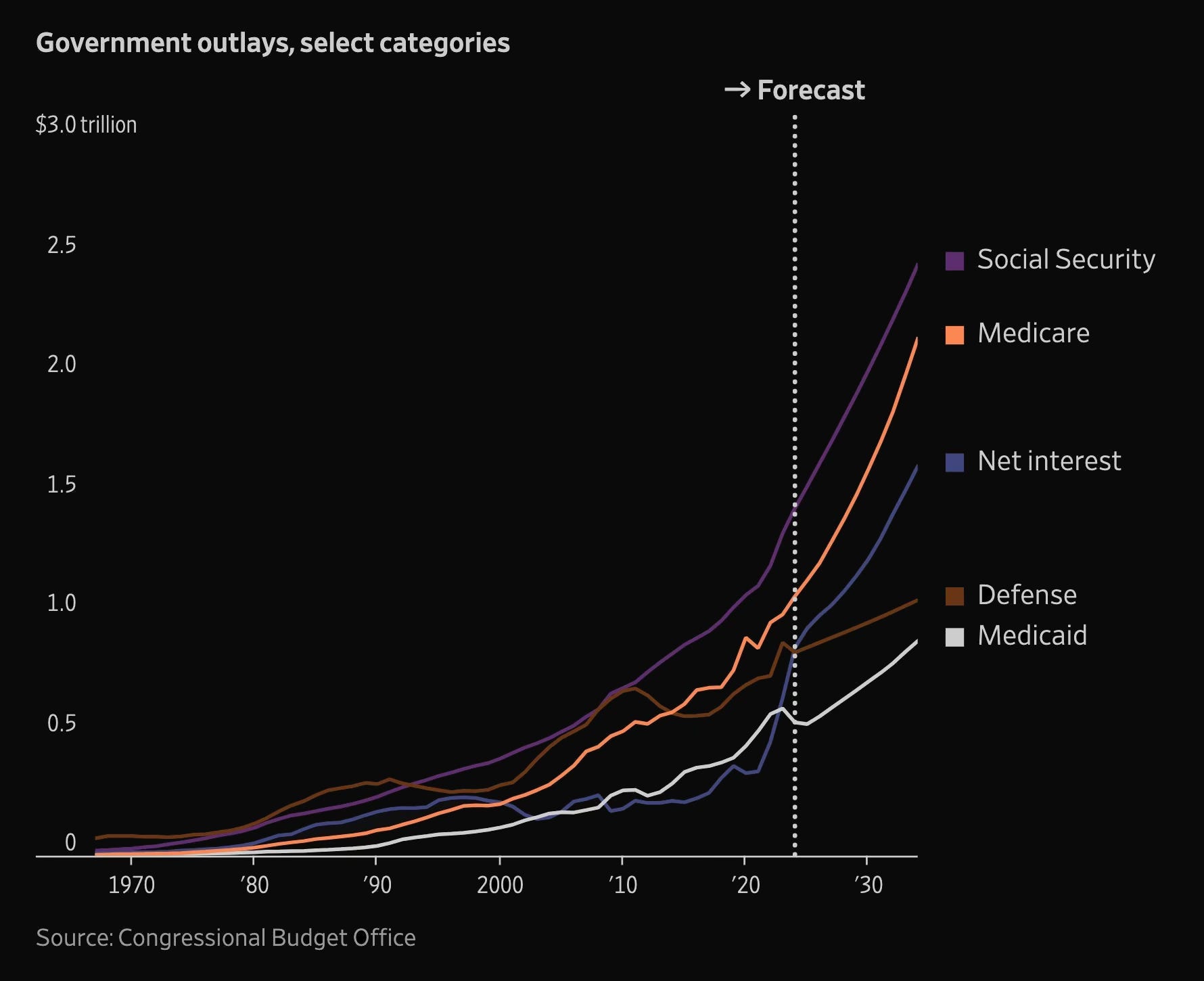

Second: Niall Ferguson’s “Ferguson’s Law.” This is the moment when interest payments on government debt exceed defense spending. That’s where the gradual erosion of a globally dominant superpower’s status begins. Geopolitical power, however you frame it, costs money. If the lion’s share of the budget goes not toward projecting strength but toward servicing debt, it becomes clear the leading state lacks the capacity to maintain the same world order that underwrote its dominance.

This produces a double blow. On one side, the state starts cutting its own defense: armies wear down, research programs get shelved, and allies hear only vague expressions of solidarity instead of concrete support. On the other, global partners, long accustomed to “Uncle Sam” pulling out a checkbook and an aircraft carrier at any moment, begin to wonder whether he can actually fund the security banquet anymore. Trust is a currency, not a natural endowment. It leaves the moment a sign of financial weakness appears on the horizon.

History shows that such turning points are not coincidences but patterns. From late Rome to the British Empire, the story is the same: when a state starts spending more than it can afford, it gradually loses the ability to fund its military, support its allies, and shape events beyond its borders. It becomes increasingly occupied with servicing old debt rather than building the future. America, for the first time in nearly a century, has arrived at the edge of this vortex. The question is not whether it knows what it’s doing. The question is whether it recognizes the language its own numbers are already speaking. And the numbers are striking:

Interest payments on the national debt have already surpassed spending on defense and Medicare, which Trump is so fond of cutting.

No surprise, then, that the U.S. has so abruptly reversed course on its foreign and domestic policy. When you take off the rose-colored glasses and look at the real numbers, it becomes obvious what’s at stake: U.S. global dominance and the entire world order, including the dollar system. And whatever you think of the policy shift, you can call the Trump team a bunch of fools and Trump himself a clown: it doesn’t matter. Because like it or not, the U.S. faces a systemic problem, and it will not disappear by magic.

You could, of course, argue that Trump single-handedly broke everything. But let’s be honest: did one person run the U.S. for all these decades? This is not a system failure. This is the system. The political, economic, and financial landscape of the U.S. was built over decades on the assumption that you can borrow endlessly, print endlessly, import endlessly, and still maintain global dominance. At some point the bills come due. Current decisions and changes are not the cause: they are the symptom.

That’s why the situation resembles a terminal diagnosis, where the patient has exactly two options. Either begin treatment, however painful, grueling, and uncertain, with a chance of recovery. Or let things run their course and get a sudden but entirely predictable death at some future date. And treatment at this point can no longer be outpatient: emergency surgery is needed.

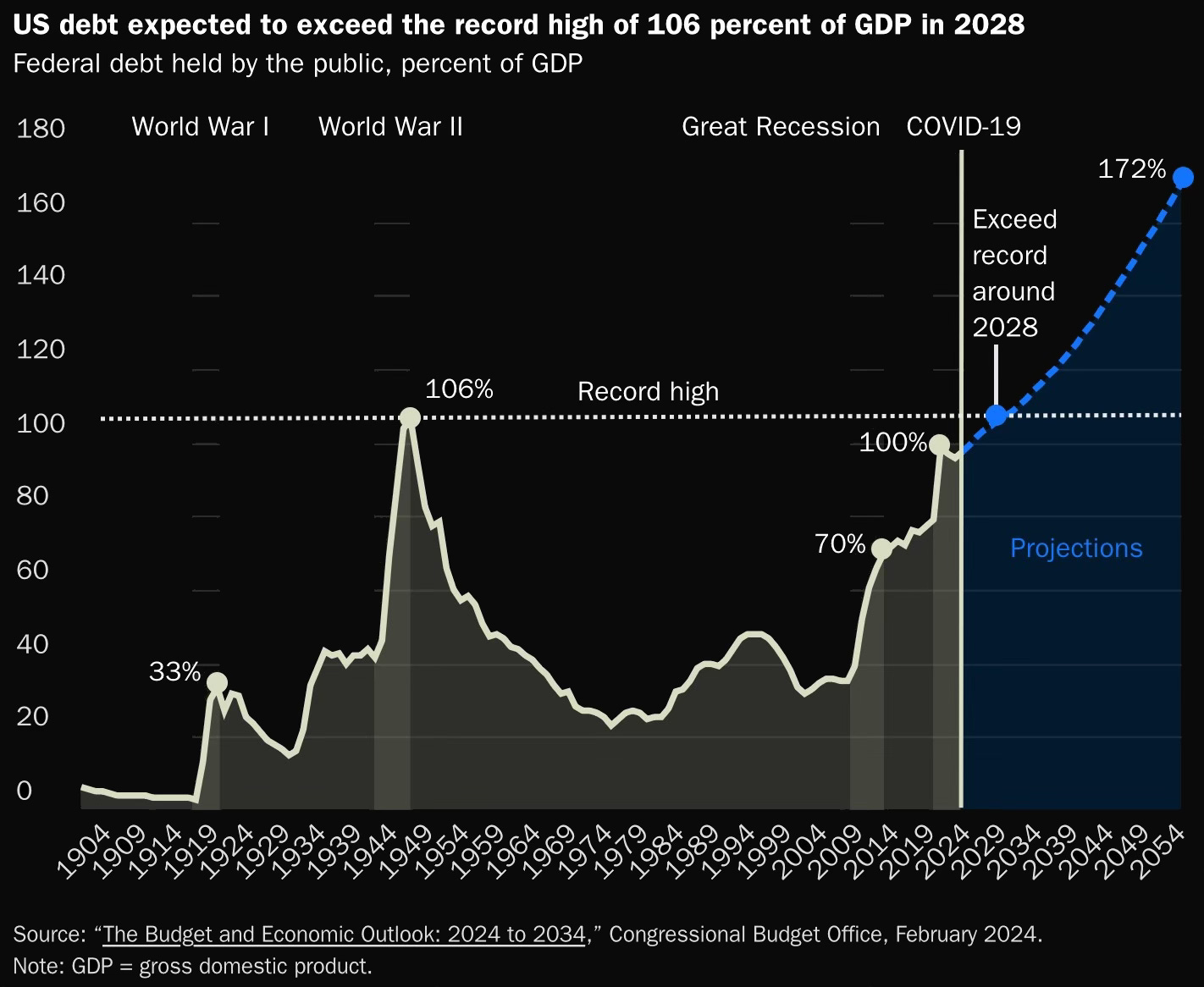

There’s one very convenient argument claiming that U.S. government debt has already reached similar levels before, back in the 1940s, and nothing catastrophic happened. 120% of GDP? Seen worse:

But the problem is that in 1945, the U.S. had not only more steel and factories than the rest of the world combined, but also a comfortable luxury: no bombs on its own territory.

For one thing, America in the 1940s was not a finance-and-services empire built on consumption. It was an industrial monster, armed to the teeth with factories, ships, and motivation. Europe and Asia lay in ruins, and the U.S. exported literally everything, from tanks to toothpaste. Today, core supply chains sit in China, Vietnam, and anywhere but Detroit.

For another, the debt of the 1940s didn’t just grow on its own: it was the price of a world war that mobilized the entire economy. People worked, saved, bought war bonds out of patriotism rather than yield. Most importantly, after the war they returned to an economy primed for a manufacturing boom, not Twitter influencing and a deficit-ridden federal budget.

Today, debt grows because that’s how the system was built, because deficits became a way of life and deindustrialization became the norm. In the 1940s, the Fed tried to cap rates and coordinate with Treasury. Today, everyone more or less pretends everything is under control.

And social obligations should not be forgotten. If in the 1940s wages were low, consumption limited, and health insurance sounded like a utopia, today’s taxpayer expects pensions, hospitals, and preferably no tax increases. Yes, the U.S. climbed out of its debt peak back then, largely through GDP growth, exports, a demographic boom, and a monopoly on producing essential goods with cheap labor. Today, debt grows without a war, without mobilization, without a plan, and without brakes.

Comparing the current debt situation to 1945 is like comparing an ultramarathoner who ran the full distance in body armor and boots to someone who just sits around getting fat on a calorie credit card.

Geopolitical Risks

While some comfort themselves with World War II debt analogies, here is one scenario that would genuinely make things worse: war. Not one war, but several at once, and not necessarily with direct American military involvement. It’s enough for allies to be fighting while the U.S., as the coalition’s senior partner, delivers democracy in crates of ammunition. According to the Global Conflict Tracker, 28 armed conflicts are currently burning across the planet.

Say the war in Ukraine continues, escalation breaks out on the Korean Peninsula, Arab states launch coordinated action against Israel, China invades Taiwan, and the U.S. decides to strike Iran to halt its nuclear program. If China backs Iran, that means a direct collision of interests between the world’s two leading powers, with “volunteer” Chinese formations on Iranian soil.

All of this would require weapons deliveries, allied support, expanded presence, resource mobilization, and enormous sums of money that don’t exist. The source would be increased public debt and currency emission. That would push interest rates up and drive debt servicing costs far higher, deepening the deficit spiral. Not a favorable game in the long run.

That said, allies remain critically important for preserving the global order and maintaining the status of leader. This applies especially to Europe, where many countries have spent years failing to meet NATO’s 2% of GDP defense spending target, counting on U.S. protection. Under current conditions, with spending rising, that model is no longer viable. And even if European countries sharply raised defense budgets above the 2% threshold today, it needs to be clearly understood that you cannot make up for years of underfunding overnight. This is not just a budget number: it’s decades of lost time.

Looking at all of this soberly, it becomes clear that these are exactly the factors shaping Trump’s harsh and often unpopular decisions. His actions are not irrational: they reflect an attempt to adapt to new circumstances in which the U.S. can no longer afford to bankroll half the world. In that context, questions of sovereignty or human costs in the developing world may become secondary. The primary priority is America’s own interests: not scattering resources on secondary tasks that might not support but actually undermine the viability of the global financial system and the country’s own defense capacity.

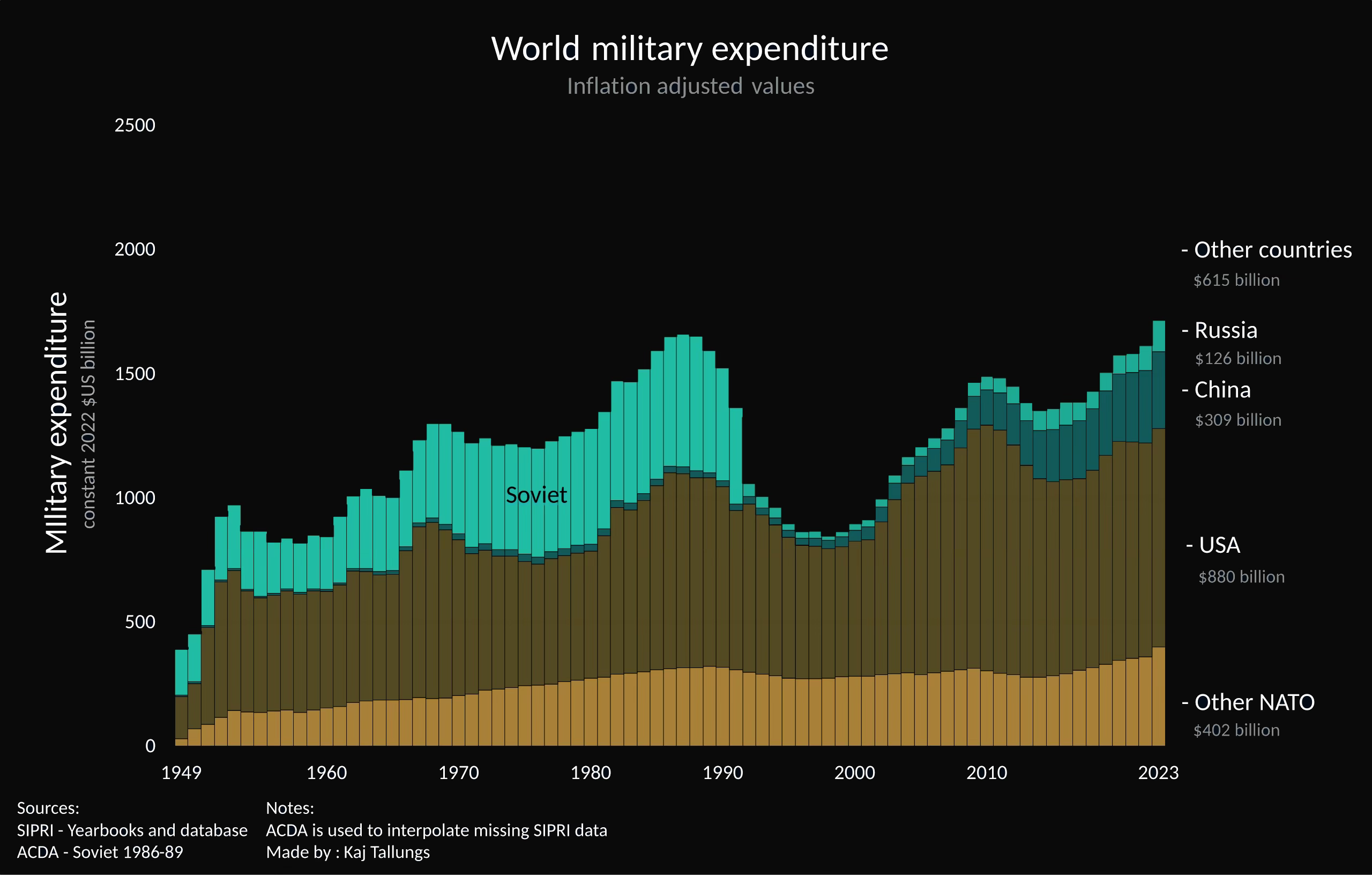

At face value, comparing U.S. and Chinese military budgets seems obvious. America spends close to a trillion dollars a year, while China spends roughly a third of that. But absolute numbers don’t always reflect real capability.

The American military budget is less about strike power than about the infrastructure of global presence. Hundreds of military bases worldwide, vast logistics, pension obligations, veteran support programs, expensive research, and private contractor agreements: all of it generates sprawling expenditures. The U.S. still has the most powerful military in the world, but its resources are stretched thin, and its effectiveness in local conflicts is increasingly questioned (the Afghanistan withdrawal being the most recent example).

China, by contrast, is focused on projecting force within its own region. Its strategy does not aim for global military dominance but for control over its immediate neighborhood, primarily Taiwan and the South China Sea. Beijing invests with precision: hypersonic missiles, next-generation air defense systems, cyber forces, satellite technologies. It simply avoids unnecessary costs, while maintaining a powerful industrial base that gives it autonomous weapons production.

The core difference lies in approaches to military economics. In the U.S., the private sector plays an enormous role: Lockheed Martin, Raytheon, and other defense contractors set the pace of innovation, but operate under market incentives where profit consistently outranks necessity. China operates through a centralized system with fast decision-making, state-controlled spending, no tender disputes and no political compromises.

Against these two models, the European Union looks like a structure where everyone acknowledges the importance of security but few want to pay for it out of their own pocket. Member states have armies and budgets, but collective combat readiness is diluted. Diversity of standards, absence of unified command, and political fragmentation leave Europe dependent on NATO. Germany spent years unable to reach its 2% GDP defense target, France maintains capability but avoids acting without allies, and Eastern European countries, despite ramping up military efforts, are still not positioned to play a decisive role in collective defense.

Russia presents an entirely different case. Its military budget is modest by global standards, but the spending structure is aimed at specific objectives: maintaining influence in neighboring countries, projecting force in select zones of interest, and nuclear deterrence. The priority is not expensive technological development but large-scale production of artillery, tanks, drones, and ammunition. The war in Ukraine has exposed weaknesses in both logistics and tactics, while simultaneously demonstrating a high degree of combat readiness. Possession of a full weapons production stack, including nuclear, remains a significant factor that constrains the range of external pressure.

Against this backdrop, a number of autocratic allies with their own regional ambitions are beginning to shift the balance of power in global politics, coordinating not through summits and press releases but through direct, back-channel, fast-moving agreements, without parliamentary pauses and long approval chains. Such claims carry enormous weight in the context of the current financial architecture, built on America’s persistent fiscal and trade deficits. But if at some point confidence in that model begins to crack, the blow will fall not only on the U.S. but on the entire system it sustains. Market democracies are vulnerable not only to tanks but to volatility. Any serious weakening of the dollar as a reserve currency, or loss of control over global capital flows, will raise the cost of debt, collapse budgets, and ultimately reduce defense spending, meaning a reduced ability to protect both the country’s own interests and those of its allies.

In this sense, the attack can come not through guns but through bonds (stopping purchases of U.S. debt or outright dumping it), not through invasions but through trade rerouting (alternative markets and other currencies). And if in the past the main instrument of power was an army, today the main instrument is increasingly trust, or its absence. China doesn’t need the yuan to become a reserve currency. It only needs to undermine confidence in the current one, the dollar. And that can be accomplished simply by accelerating the deficit spiral through more military conflicts and market expansion.

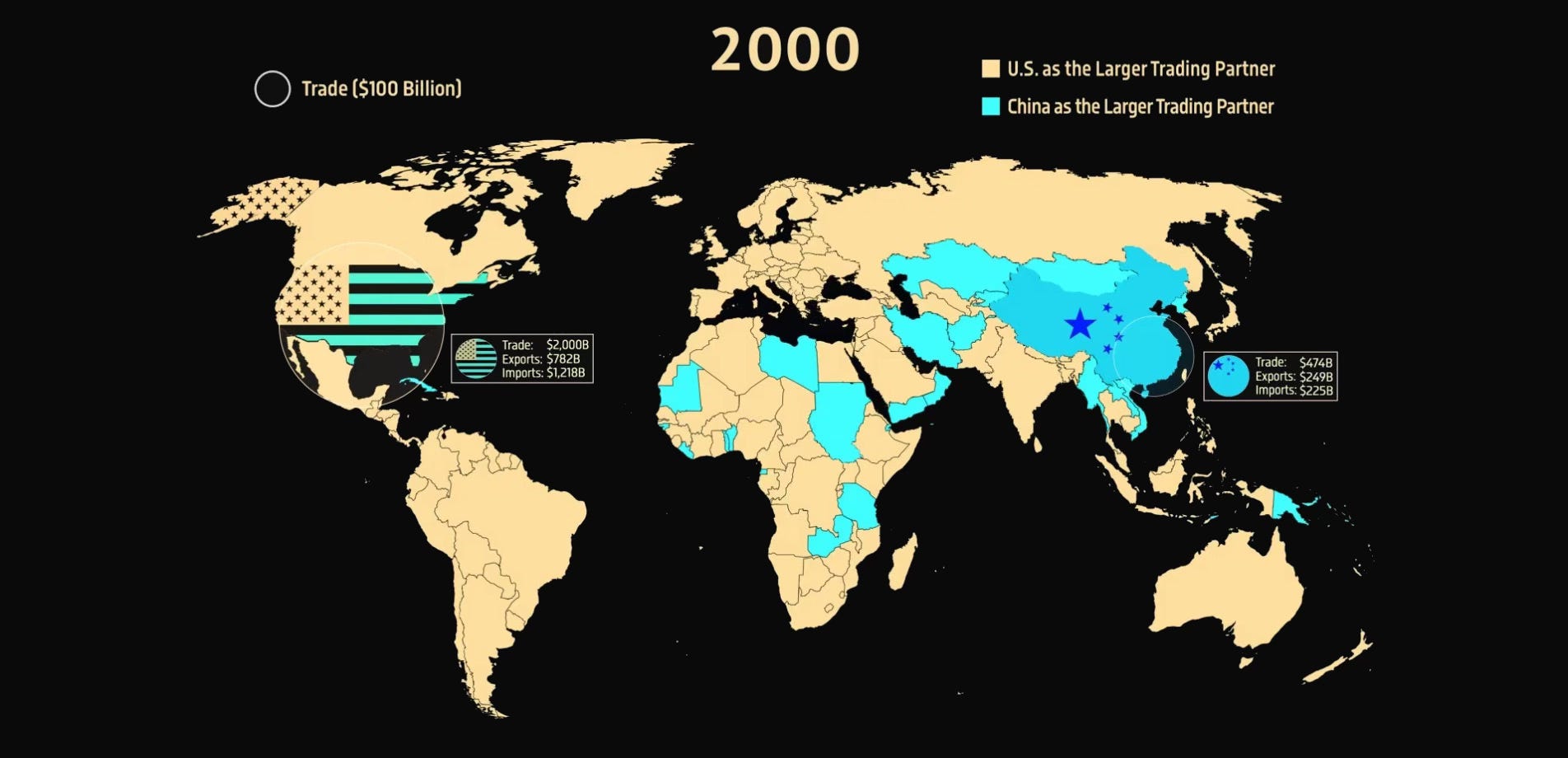

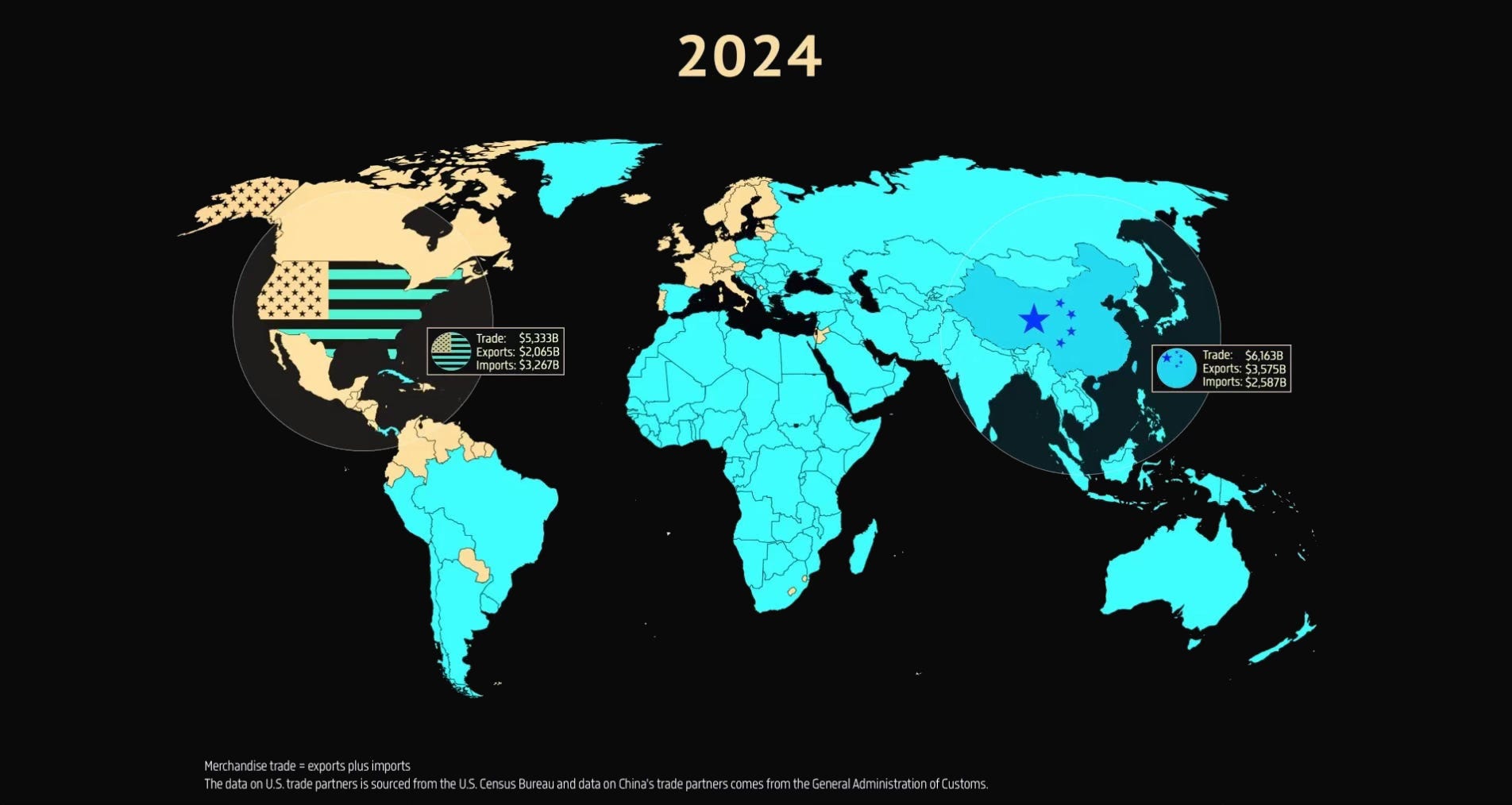

As conflicts multiply, U.S. spending will rise, while tax revenue will struggle to keep up, widening the fiscal deficit. Meanwhile the U.S. is trying to maintain influence in economic zones worldwide while pushing back against China. Just look at how global trade dominance has shifted between the two. In the early 2000s, the U.S. held leading positions in international trade, dominating economic zones with high external trade volumes.

Today the picture has reversed entirely. China has become one of the world’s leading trade partners, aggressively expanding its export capacity and deepening its role in global supply chains. This has driven a redistribution of economic and trade influence toward China.

That means new American agreements with other countries, loans, subsidies, and investments in infrastructure and security across unstable regions will require large expenditures with no guaranteed return. The effectiveness of the American defense apparatus is also in question, given that too many contracts run through private corporations where profit interest routinely outranks strategic value. So it’s not just the volume of spending that grows: it’s the sense of overextension. And when other countries begin to see that debt is growing, interest on it is rising, conflict zones are expanding, and economic returns are shrinking, confidence in the dollar and American assets starts to erode. Investors demand higher yields, which raises the cost of debt, demand for U.S. Treasuries contracts, and the dollar loses its “safe haven” status.

Conflicts and economic expansion, then, are not simply creating risk: they are becoming catalysts that amplify the vulnerability of the American financial model. China can simply watch and give the process a gentle nudge.

In that scenario, U.S. inaction is just waiting for the existing order to collapse, while action is a painful attempt to preserve dominance, or the final throes before an inevitable collapse that could drag on for years. The only question is how effective the stabilization tools will be.

Which brings us to the central question: what are tariffs actually for?

Trade Wars

No one can describe the tariff war plan better than the head of the Council of Economic Advisers in the Trump administration. Back in 2024, he worked as chief strategist at Hudson Bay Capital, where he wrote a paper titled “A User’s Guide to Restructuring the Global Trading System,” laying out all the economic levers that would be used to shift America’s economic and geopolitical course:

“If the U.S. is no longer willing to bear the burdens of the current order, it will take steps to change it.”

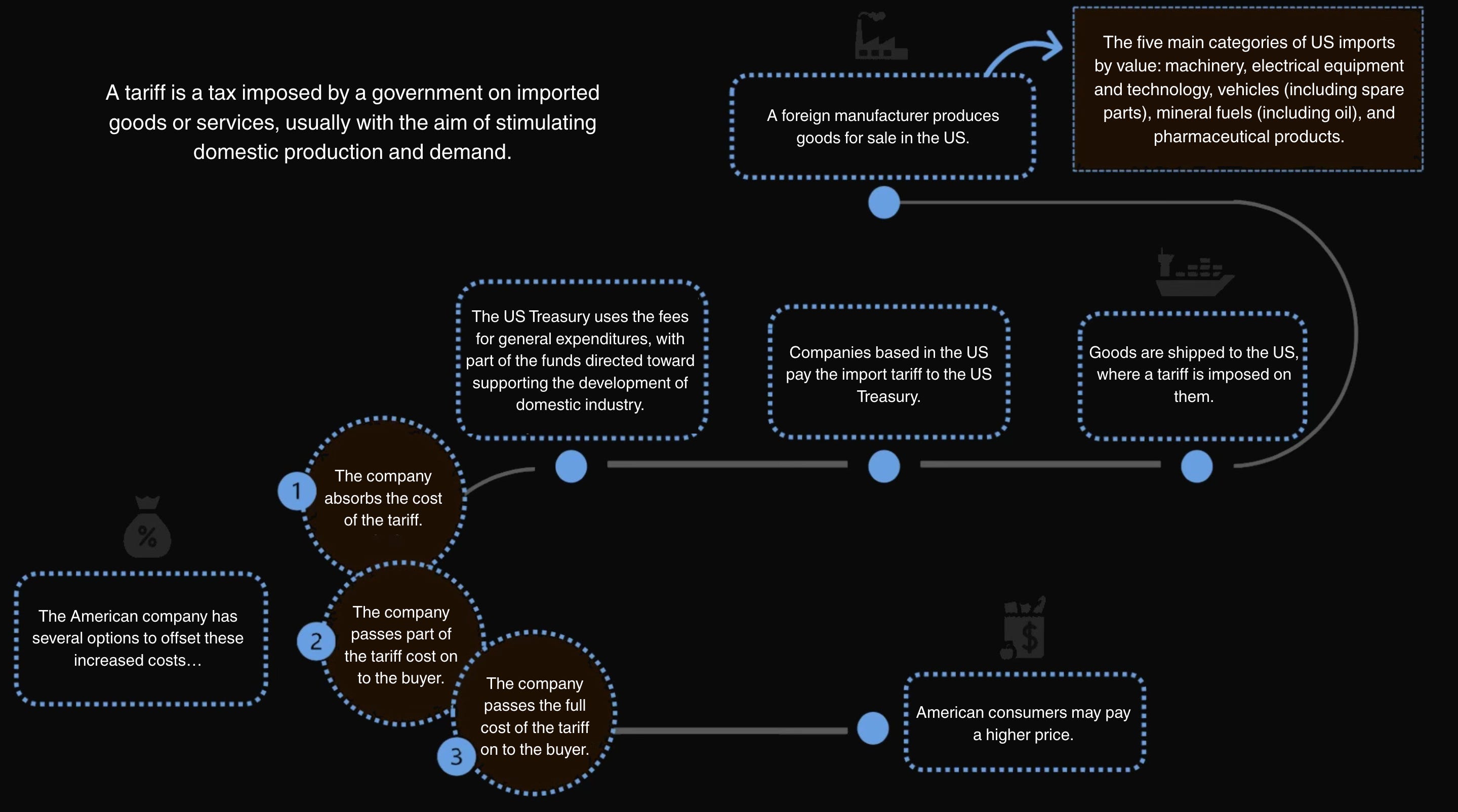

Tariffs raise the cost of imports, making American goods relatively cheaper. In theory, this should stimulate domestic production, bring back jobs, and reduce the trade deficit. But if foreign currencies weaken in response, the dollar strengthens, imports don’t get more expensive, and American exports become even less competitive. So weakening foreign currencies against the dollar acts as a compensation mechanism that makes American goods more attractive on foreign markets.

But under the administration’s plan, tariffs won’t be uniform. Trump adviser Scott Bessent proposes dividing countries into “good,” “bad,” and “neutral” based on criteria like currency manipulation, compliance with NATO commitments, or support for China at the UN. Friends of the U.S. (those who pay for NATO and don’t manipulate their currency) get low tariffs, while adversaries get crushed under the weight of high ones. The idea is to make access to the American market a privilege, not a right, while forcing allies to share the security burden.

This isn’t only about protecting industry: it’s also about money. In 2018-2019, tariffs generated billions that were effectively paid by China through yuan depreciation. Why? By weakening the yuan, China absorbed the tariff cost increases and kept its goods cheap and accessible, leaving consumer prices manageable. China essentially reduced its manufacturers’ yuan-denominated revenues.

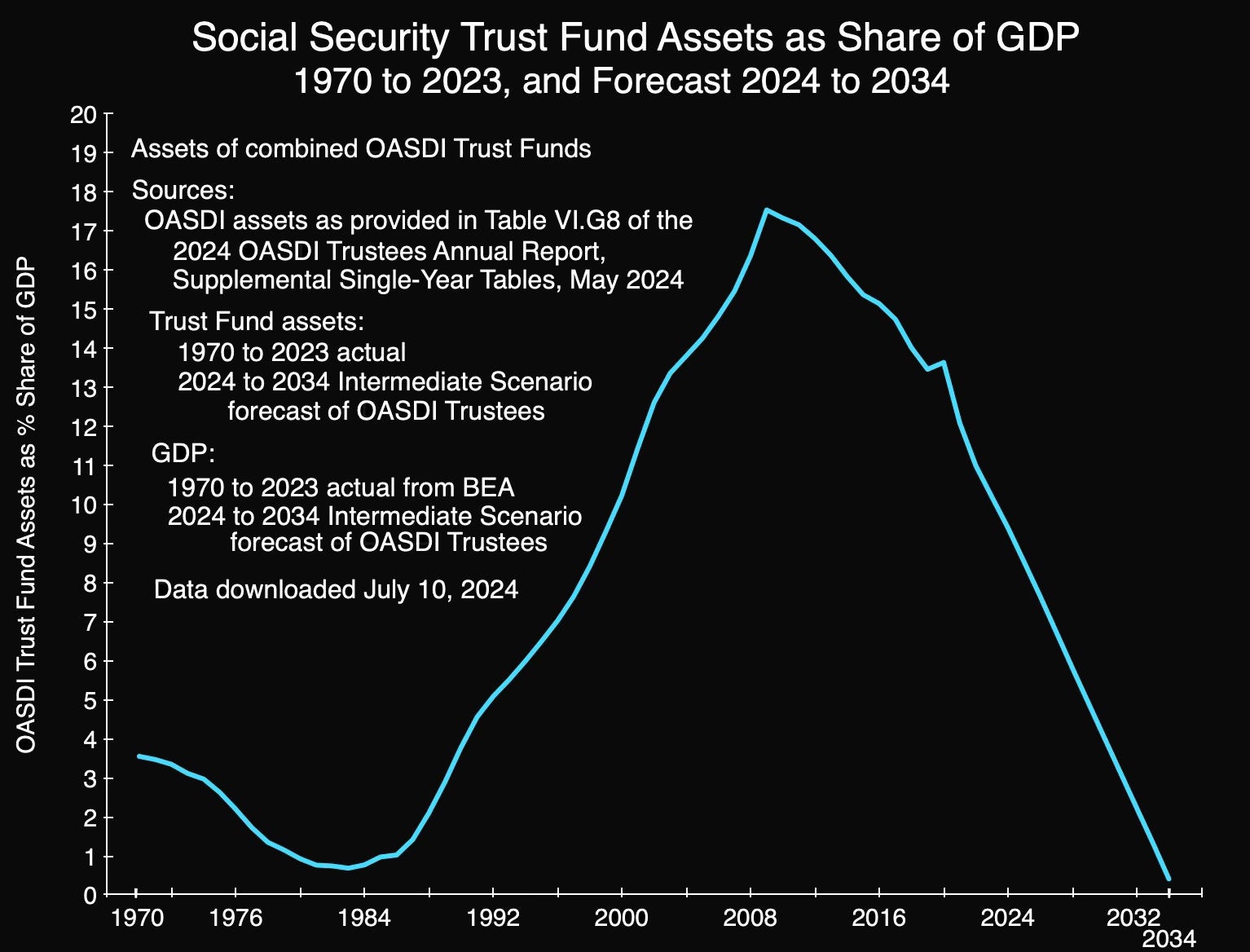

Now, with the U.S. fiscal deficit at 7% of GDP and the Social Security trust fund projected to be exhausted by 2033, tariffs are seen as a potential source of funding for tax cuts or new factories.

Of course, tariffs fit perfectly into national security rhetoric. Trump once said, “If you don’t have steel, you don’t have a country.” In that logic, tariffs can help protect critical industries like steel, semiconductors, and pharmaceuticals from Chinese espionage and dependence on unreliable supply chains. If China were to cut off chip or drug supplies tomorrow, the U.S. would find itself in a vulnerable position.

Tariffs are meant to create a powerful incentive to relocate production to the U.S. Semiconductors are the brain of the modern economy, from smartphones to missiles. Dependence on Taiwan and China (where 60% of global chip production is concentrated) is a key American vulnerability. Tariffs on Chinese chips will make them uncompetitive, pushing companies like TSMC or Intel to build plants in Arizona or Texas. The CHIPS Act of 2022 already allocated $52 billion for this, but tariffs add a lever of pressure.

Pharmaceuticals are another raw nerve. The U.S. imports 80% of active pharmaceutical ingredients from China and India. In a crisis (think COVID) this can become catastrophic. Tariffs on Chinese drugs and components will push companies like Pfizer toward relocating production. But relocating complex manufacturing takes years, requires billions in investment, and demands skilled workers that the U.S. doesn’t have in abundance. Plus, China can keep retaliating with its own tariffs, complicating exports of American technology. This is a chess match where every move carries losses: geopolitical zugzwang.

But that’s only one part of Miran’s plan. The second part is weakening the dollar. In the administration’s view, an overvalued dollar is the root of all problems, and it needed to be weakened. The problem is that the dollar, as the global reserve currency, is persistently overvalued, with an exchange rate higher than what balanced trade would require. Dollar overvaluation is driven not only by domestic consumption policy and deficits, but above all by its status as the world’s reserve currency, which creates persistent demand for the dollar regardless of the trade balance. A strong dollar, in turn, sustains the consumption model and the growth of deficits (and public debt accordingly).

Weakening the dollar is the only option for increasing competitiveness, shrinking the trade deficit, and reviving industry, while simultaneously pressing geopolitical rivals. Miran sees two paths to this.

Option One: Mar-a-Lago Accord

Historically, the U.S. weakened the dollar through international agreements like the 1985 Plaza Accord, when allies agreed to let their currencies strengthen (yen, deutschmark), so the dollar could fall and American exports could recover. The current administration is apparently planning its own version, called the “Mar-a-Lago Accord.” Its central goal: persuade Europe, China, and Japan to strengthen their currencies so the dollar weakens and the U.S. regains its price advantage.

The problem is that no one wants to play this game. Europe is sitting on negligible growth and is comfortable with the status quo. Japan is still wary of the deflation that hit it in the 1990s. China is holding onto exports. Diplomacy won’t work here: you need carrots and sticks. The stick is tariffs. The carrot is tariff removal. And to amplify the pressure, the next idea emerges: century bonds.

The idea is that countries under the U.S. “security umbrella” (NATO, Asian allies) must buy not just short-term bonds but hundred-year bonds. In other words, America says plainly: “Want our protection? Pay for the next one hundred years.” This simultaneously:

Locks in external demand for government debt, relieving pressure on the American budget (a 7% GDP deficit is a problem).

Forces allies to sell dollars and buy their own currencies to invest in long-dated paper: the dollar weakens.

Links defense and economics: want tariff relief, buy our debt and fund NATO.

Selling this idea to China is impossible, of course. China will sooner park reserves in gold (which it’s been doing for a while) than sign up for a century-long attachment to U.S. debt. Europe won’t be enthusiastic either, given economic stagnation. But through the dollar, tariffs, and Treasuries, the U.S. wants to change the rules of the game in its favor.

Option Two: IEEPA and Currency Reserves

Miran noted that the Wall Street view that exchange rates depend solely on Fed rate decisions is wrong, since the Trump administration can take many steps independent of the central bank’s decisions (which, frankly, even surprised me).

If diplomacy fails, Trump will turn to a more radical tool: the International Emergency Economic Powers Act (IEEPA). This economic Swiss Army knife allows for sanctions, asset freezes, transaction blocks, and a “tax” on foreign dollar reserves.

The idea is to impose a “parking fee” on foreign central banks’ holdings of U.S. Treasuries. For example, withholding 1-2% annually for the privilege of accessing dollar liquidity.

This would make dollar reserves less attractive. Countries, to avoid these costs, would start reducing dollar assets and thereby strengthen their own currencies. The dollar would weaken, and the U.S. trade balance would improve. But if you overdo it, you can break the whole structure: the dollar goes into steep decline, yields on bonds soar, and the U.S. mortgage market could collapse again. So it needs to be done gradually.

There’s one more option: the Treasury could begin manipulating currency exchange rates directly. By selling dollars and buying euros, yen, or even yuan, it would artificially raise foreign currency rates, weakening the dollar through direct intervention. The catch is that it costs money. To accumulate $1 trillion in reserves, you’d need to either pull those dollars from the market or print them. And printing means inflation risk, which the Fed is fighting so hard to contain.

Trade as a Weapon

The Trump administration wants to tie trade to national security, turning the U.S. into a fortress surrounded by tariff walls and loyal allies. The idea is to make the world share the burden of providing reserve assets and the security umbrella. If you don’t pay for NATO, don’t fight China, or steal American intellectual property: welcome to the high-tariff club.

“Trade terms can be used as a tool to achieve better outcomes in security and burden-sharing. A clearer delineation of the international economy into security zones with shared principles and economic systems would help identify persistent imbalances and introduce more friction points to address them. Countries that want to be under the U.S. security umbrella should also be under the umbrella of fair trade.” — from Miran’s document.

China is the main adversary. Enormous tariffs are an attempt to strangle China’s export model and force it to open markets, stop technology theft, and strengthen the yuan. If other countries join the “tariff wall” (say, the EU imposes heavy duties on Chinese cars), China ends up isolated. But if they refuse, the U.S. wins anyway, collecting revenue from their exports.

There’s also an alternative scenario where China could avoid tariffs by investing in the U.S. Imagining Chinese car factories in America is difficult, but it would be a repeat of the Reagan-era playbook, when Japan built factories in the states to avoid tariffs. The problem is that China, obsessed with control, is unlikely to agree to export its factories and create jobs for Americans. Reality diverges from theory further still: trading partners don’t sit still.

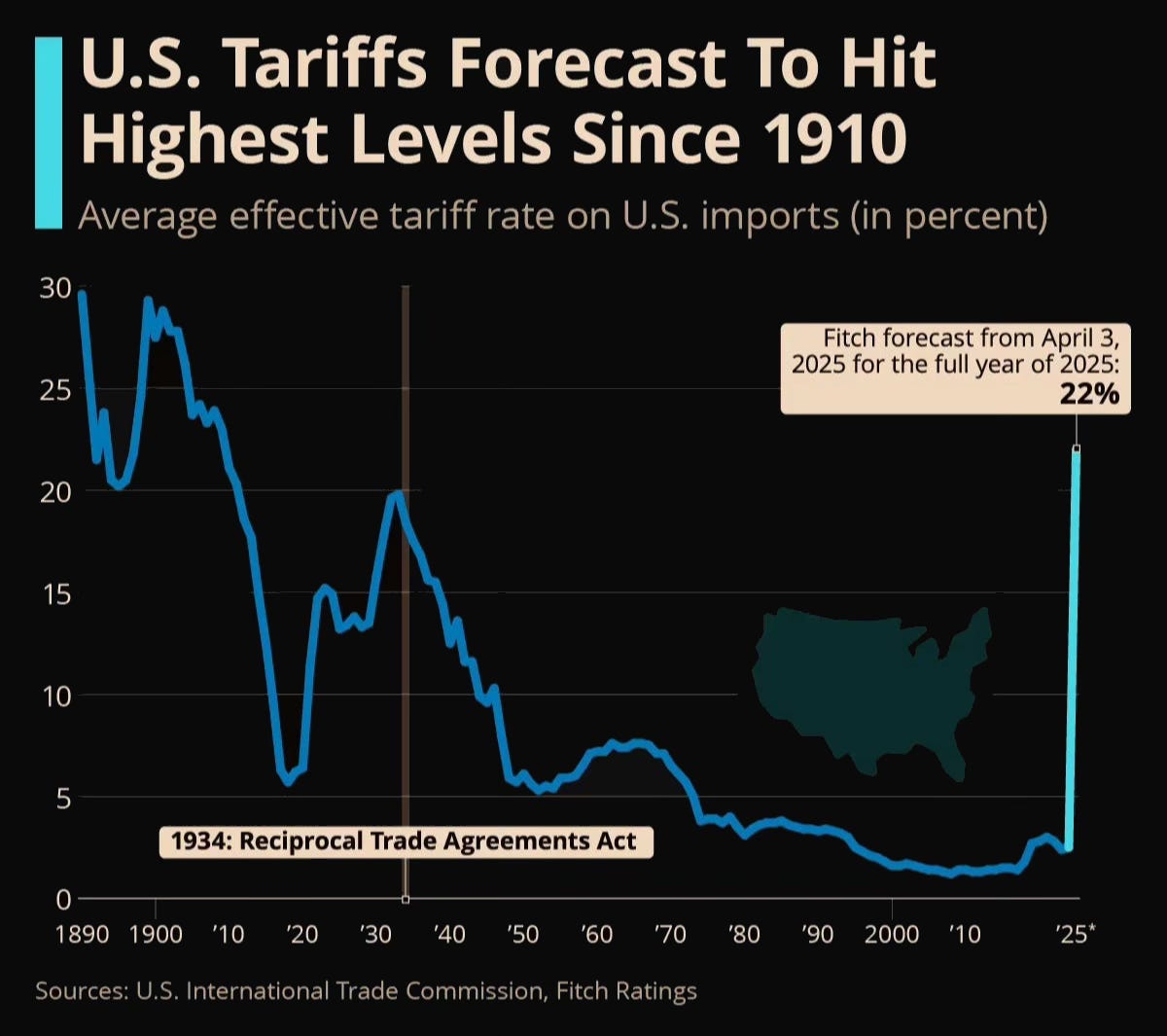

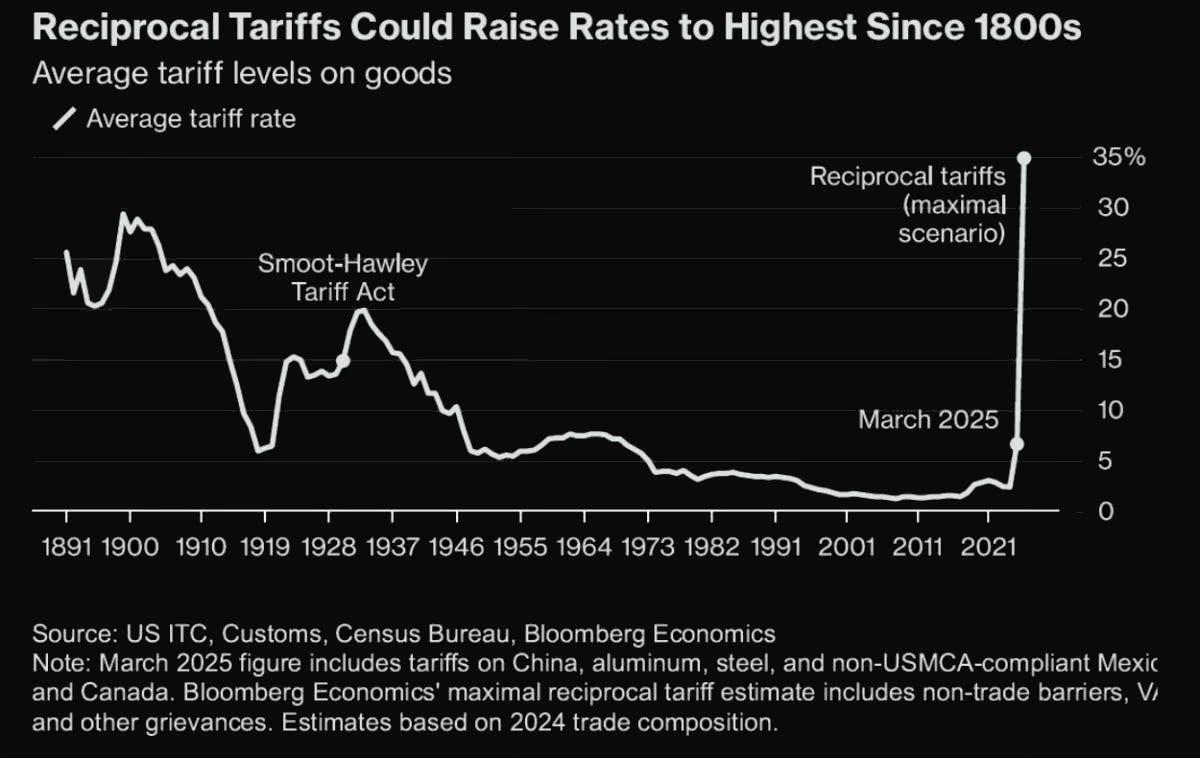

So what we’re actually watching today differs from the script above. Trump didn’t start with a gradual tariff increase. He went in with a shock, stunning absolutely everyone without exception. The effective tariff rate has returned to early 20th century levels, which means one thing: we’ve entered territory unfamiliar not just to us but to several generations before us.

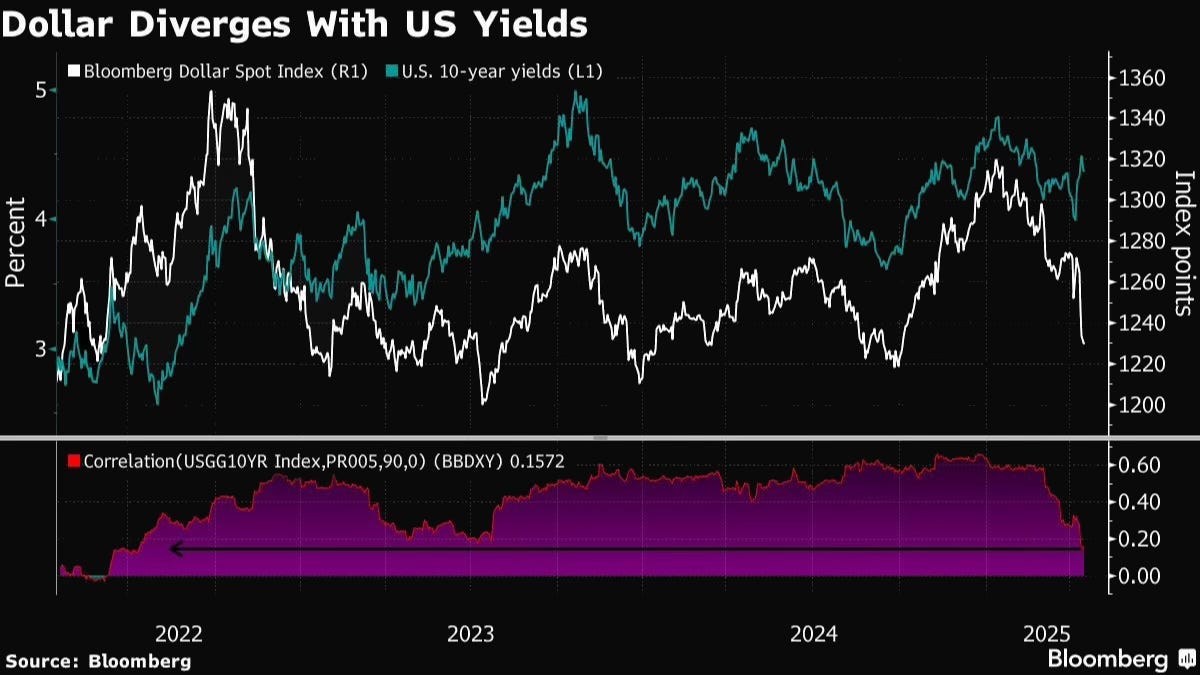

This is a blow to allies’ exports, with their currencies beginning to strengthen (trade surpluses falling), as tariffs restrict the flow of dollars abroad, reducing demand for dollar assets and for the dollar itself. Sarcastically speaking, that’s already a win: the dollar weakened without any negotiations. The American administration made a sharp first move in its attempt to reshape the system through leverage. But there’s a complication.

Foreign investors (presumably China) started dumping Treasuries, pushing yields up and increasing the risk of even greater debt loads and fiscal deficits with a weakening dollar. China may have needed only a small intervention for algo traders to pick it up in a low-liquidity market with few buyers.

Rising yields mean new bond issuances come at even higher rates, while old ones get replaced upon maturity. We’re back where we started: rising yields mean rising debt service costs. This is an enormous risk that will gradually erode leadership. Recession fears triggered a flight to alternatives: bonds from other countries and gold. That further weakened the dollar and strengthened foreign currencies as demand shifted to alternative safe havens. As a result, Trump had to step back somewhat, announcing a 90-day pause on tariffs for all trading partners except China, to slow the avalanche of negative consequences from an abrupt tariff policy.

And so a kind of negotiation is unfolding, one capable of pushing the global economy toward a situation where recession would look like a walk in the park. This is literally shock therapy for the global economy, and it will have a sequel. Worth quoting one of the best macroeconomists of our time, Olivier Blanchard:

”If you are a firm, either an importer or an exporter, or just a supplier of an importer or exporter, you just do not know whether and where to invest. The option of value of waiting is very high, and so you wait to invest until things clear. The right decision for you, but very bad news for investment demand and economic activity. Ironically, it is not the US which is likely to suffer the most. But the countries which have bet their growth on exports and their participation in supply chains, the Mexico, the Korea, or even the Germanys of the world. Sad and scary.”

The central problem is this: if such aggressive tariff policy continues for all four years of Trump’s presidency, and trading partners keep retaliating in kind, destabilization is inevitable. Businesses and ordinary citizens under uncertainty will try to minimize risk: holding back investment, building up rainy-day cash, and cutting spending, which is already happening. The result is a sharp contraction in economic activity that could trigger something worse than a recession, possibly a new depression. The economist Thomas Sowell is well-suited to this context:

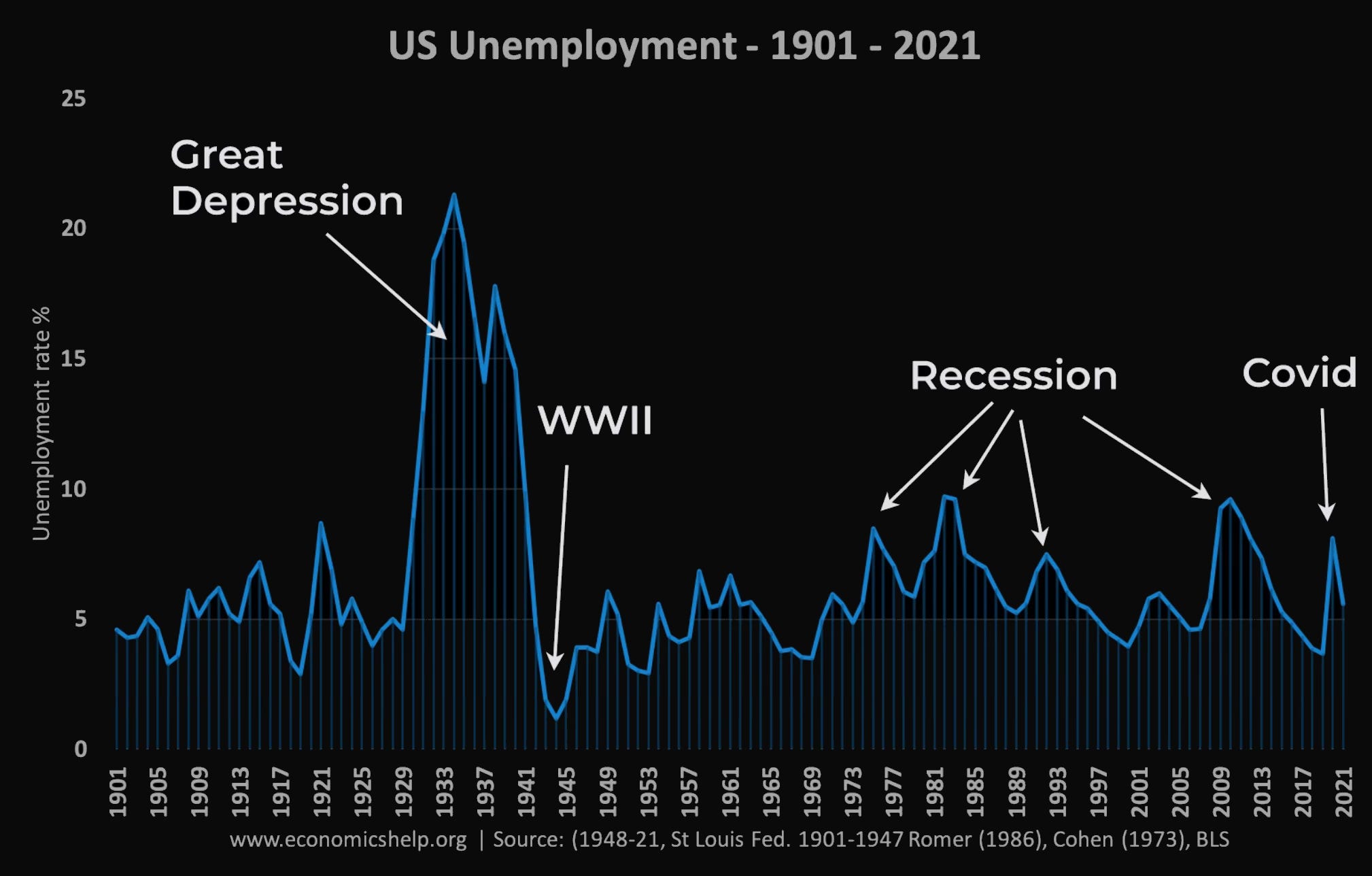

“Government intervention during the Great Depression began under President Herbert Hoover, who signed the Smoot-Hawley Tariff Act in 1930, which set the highest import duty rates in more than a century. The idea was that more American-made goods would be sold, providing more jobs for Americans. This decision seemed reasonable, as do many actions by politicians.”

“However, an open letter signed by a thousand economists from the country’s leading universities warned against imposing these tariffs; the scholars argued that Smoot-Hawley would not reduce unemployment but would produce the opposite results. This had no effect on Congress, which passed the bill, nor on President Hoover, who signed it in June 1930. Within five months, unemployment reversed course and for the first time in the 1930s rose to double digits, never falling below that level for a single month for the entire decade, as all subsequent government interventions proved either useless or counterproductive.”

One can argue that mass unemployment in the 1930s was caused less by the 1929 stock market crash, as is commonly assumed, than by the Smoot-Hawley Act, which sharply raised tariffs on imports. Although unemployment did begin rising after the market collapse, it didn’t exceed 10% in the twelve months that followed. But just five months after Smoot-Hawley was signed, unemployment shot to 11.6%, then continued rising past 20%, staying above 11.6% for eight years. This suggests that protectionist policy triggered the collapse of global trade, deepening the economic downturn.

During the Depression, protectionist measures also undermined international cooperation, intensified economic conflicts, and made countries more isolationist and aggressive, creating ideal conditions for the rise of dictatorships and radical ideologies, and ultimately World War II and the restructuring of the global order.

Industrial Fizzle

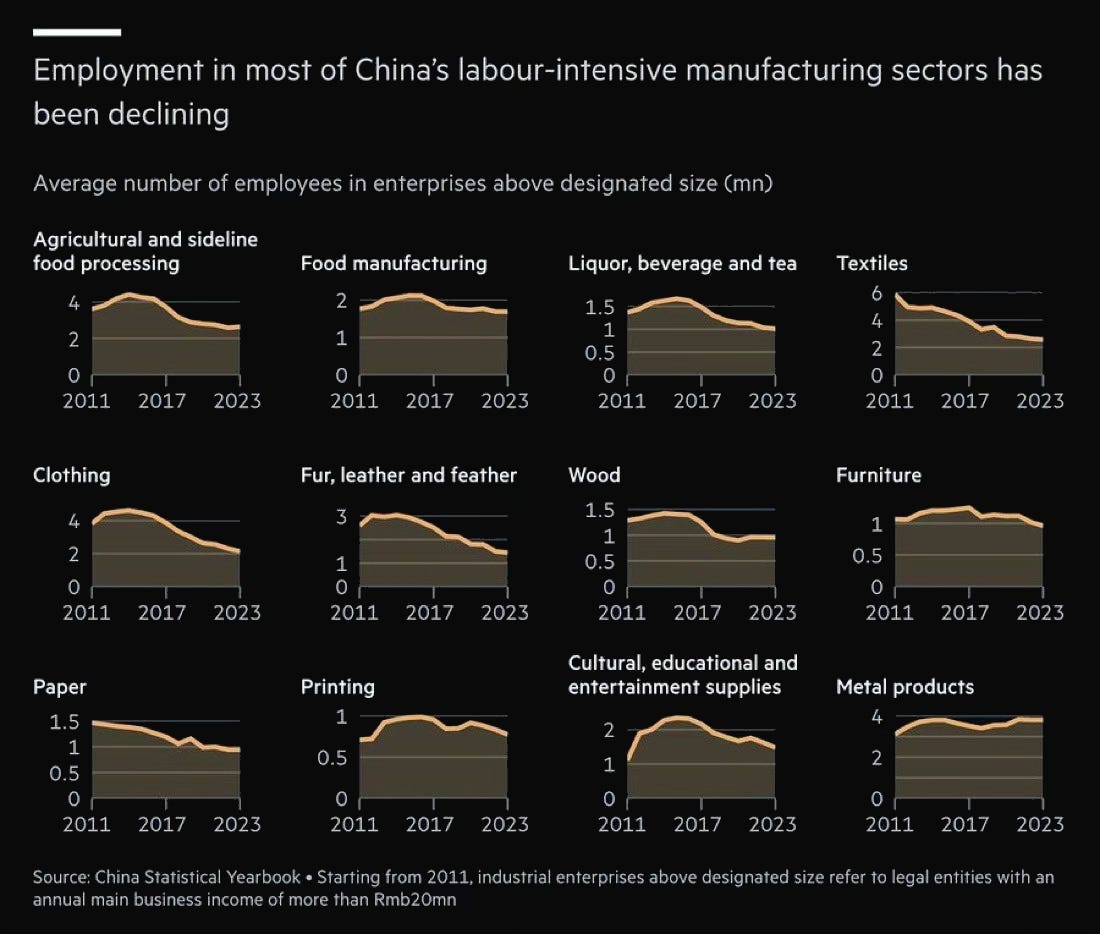

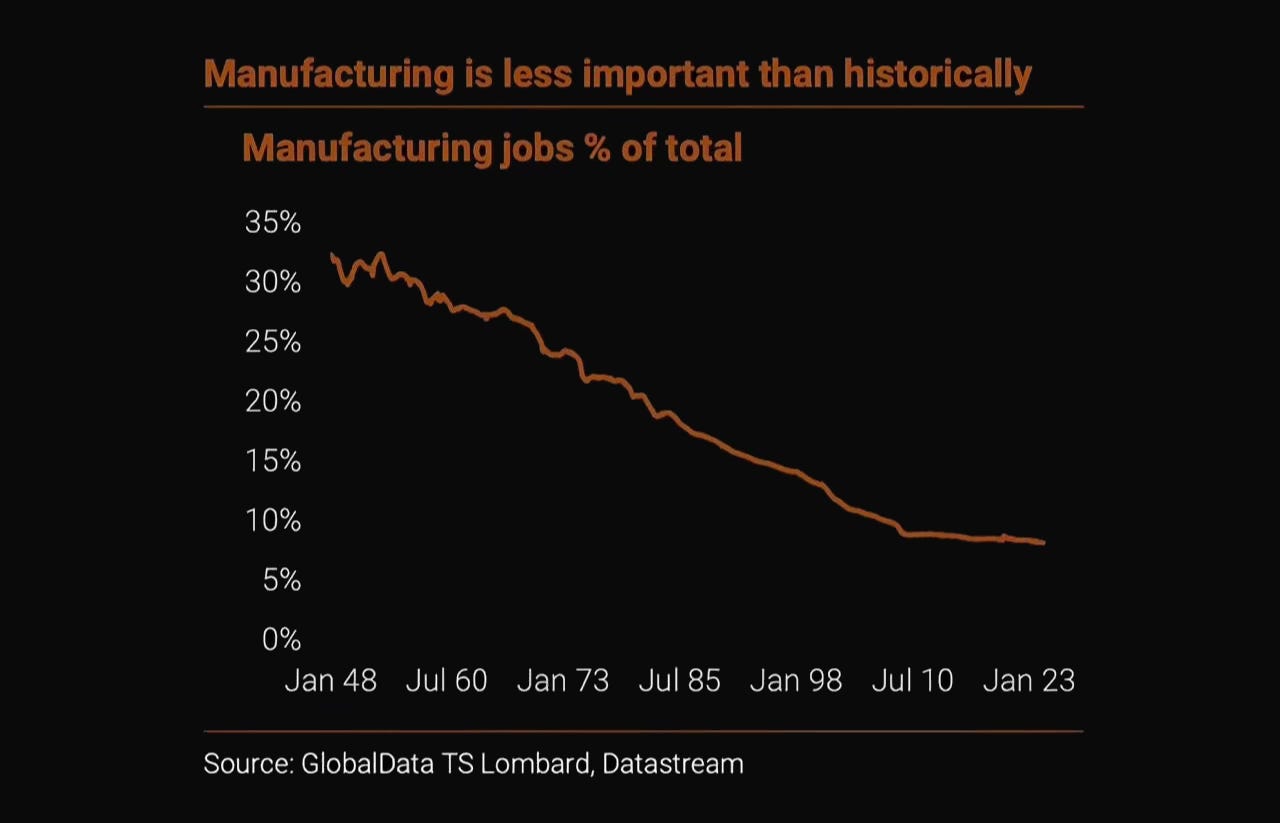

Equally important is Americans’ misreading of Trump’s “manufacturing revival” through tariffs, where everyone imagines job growth. In the modern world, this sounds more like a political slogan than an actual strategy. Even in China, the world’s factory for so long, manufacturing employment is not growing: it’s declining.

This is not because China is losing trade wars. It’s because robots, algorithms, and automation systems are simply displacing people from the production cycle. In the U.S. today, only about 8% of employed workers are in manufacturing, and even among them, half are not factory workers in the classical sense but office workers, accountants, logistics specialists, and other support roles.

If the Trump administration continues betting on extremely high tariffs as a way to stimulate production, the result could be severely negative. Global supply chains will fracture, raw materials will get more expensive, exports will lose competitiveness, and automation will keep reducing labor demand, raising unemployment not just in manufacturing but across all related sectors.

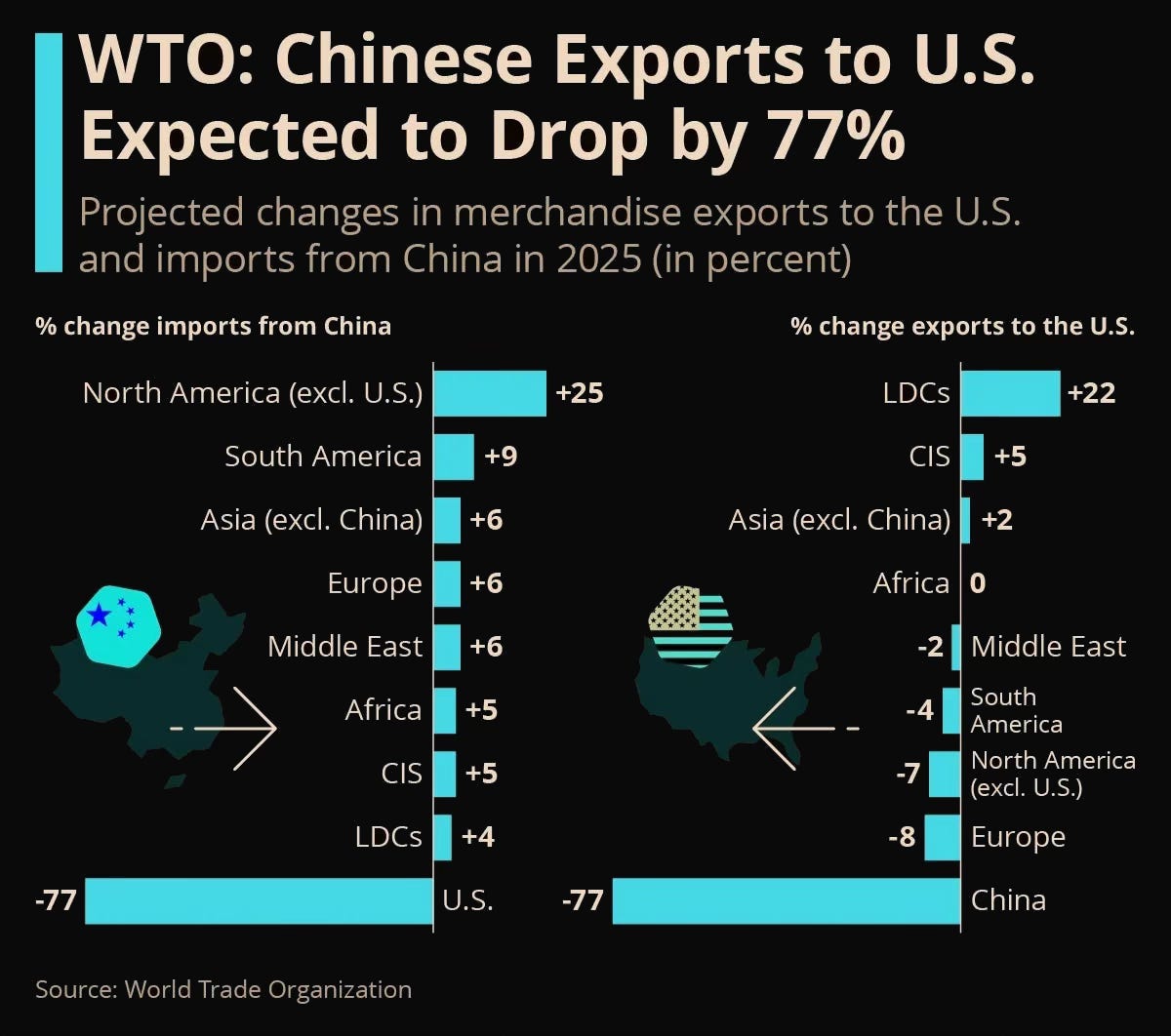

As for global supply chains: WTO projections already forecast that Chinese goods exports to the U.S. will collapse by 77% in 2025.

Trump’s tariff pressure and political rhetoric are making the American market unattractive and toxic. But China is not panicking. As the data shows, it is simply planning to redirect its flows to wherever it can trade: Latin America, other parts of Asia, even Africa.

Meanwhile, other countries also dependent on the American demand model are feeling the effects of tariff policy. Their imports into the U.S. are starting to stall as well. The winners are those supplying goods the American economy cannot do without (resources, energy, raw materials), along with countries willing to fill vacated niches with cheap labor and flexible terms with minimal demands.

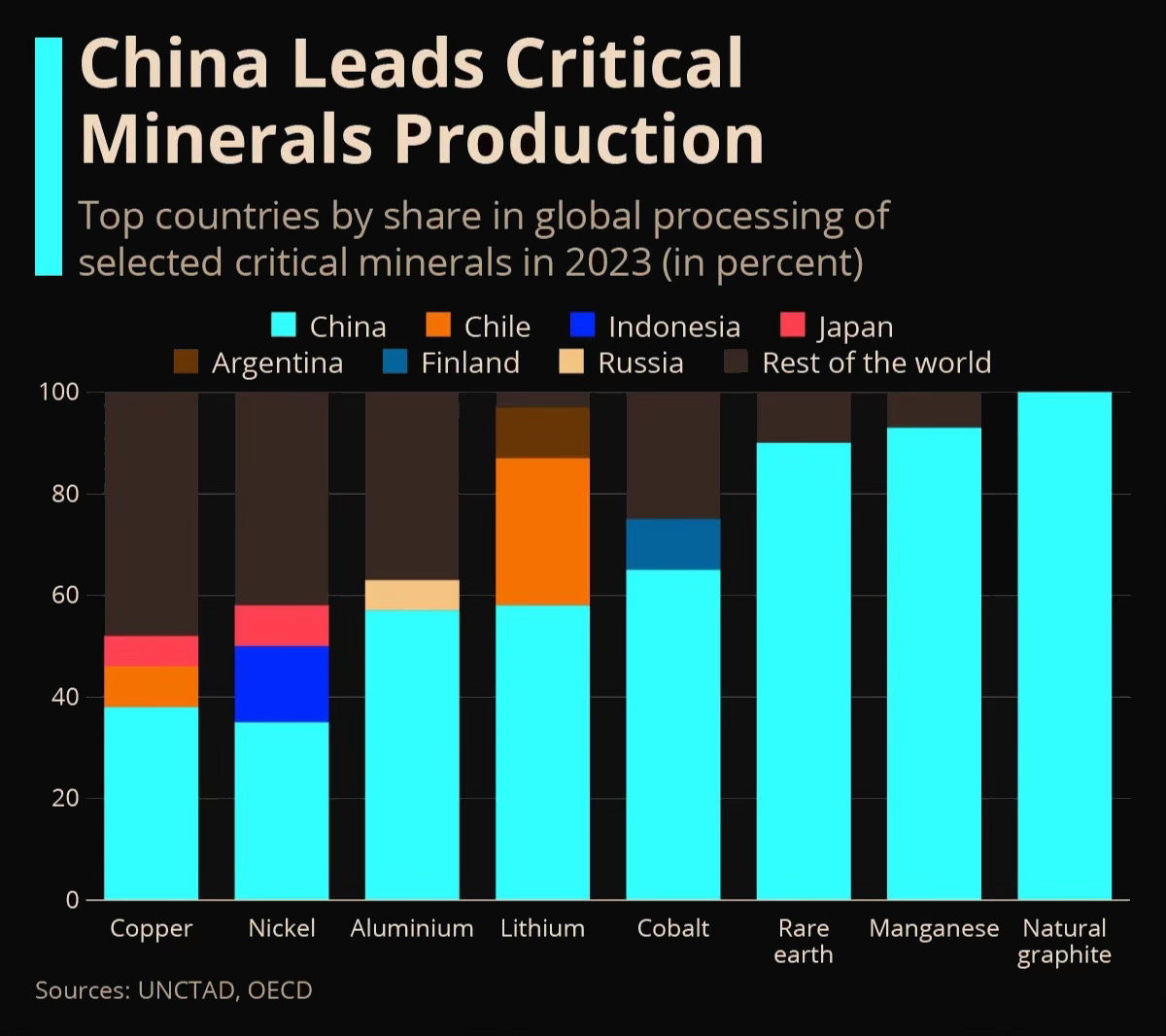

For the U.S. itself, all of this means higher prices, supply disruptions, and further complications of already tangled logistics chains. Breaking dependence on China sounds like a beautiful idea in theory and an expensive indulgence in reality. Especially when that dependence extends beyond cheap T-shirts and electronics to raw materials: the very foundation on which green energy, advanced technology, and defense are built, all the things the U.S. wants to hold global leadership over. When a deficit can no longer serve as a source of strength, the only remaining universal lever is control over what is genuinely valuable: resources and technology, where the latter depends on the former. But there’s a problem there too: China near-monopolizes the rare earth supply chain and the processing of critical resources.

And as the U.S. severs ties with Beijing, it urgently needs to figure out where to source what’s being cut off. That’s why talk of joint American-Russian Arctic projects carries strategic weight. Greenland’s resources are also back in focus, despite its inaccessibility.

Meanwhile, against the backdrop of war, sanctions, and frozen relations, Americans are increasingly pushing a mineral resources deal with Ukraine, and also with Russia, aimed at driving a wedge into the solid Russia-China alliance and trying to build a more independent resource base. When resources and the preservation of dominance are on the table, ideology about democratic values takes a back seat.

But replacing China and restarting supply chains takes years and careful diplomacy. And while the tariff wars continue, business lives in a state of uncertainty, navigating a minefield where any decision could prove fatal. In that instability, the silhouette of a new global recession is visible, not an industrial resurrection.

An economic downturn amid aggressive tariff policy will only worsen the situation. To cushion the blow and support consumer demand, the government will again have to cut rates, increase spending, and issue new debt obligations. That in turn will raise the cost of debt servicing and perpetuate the chronic fiscal deficit. Under those conditions, breaking out of the deficit spiral becomes not just difficult but practically impossible. With each new round of stimulus, the system only digs itself deeper into debt dependence. Accordingly, the weakening of the dollar architecture and the loss of global leadership sounds not like a hypothesis but like a scenario slowly unfolding.

Conclusion

Protectionism? It hits the consumer and allies. Continuing deficits? It deepens the debt spiral. Weakening the dollar? It undermines confidence in the reserve currency. Raising rates? It suffocates the economy. Cutting them? It accelerates inflation and weakens the dollar further. This is geo-economic zugzwang, where every next move worsens the position and could prove destructive, while inaction only postpones the inevitable.

When Trump launched the trade war with China, it initially looked like just another populist move: “America is losing,” “we’re being exploited,” “we need to bring back factories.” But behind these loud slogans stood a fairly well-structured plan. The idea was to redistribute global supply chains, reduce the trade deficit, and restore some degree of American independence from Asian manufacturers. The Hudson Bay Capital document lays out these goals in detail: regain control, restore sovereignty, rebuild the architecture of global trade.

The strategy is clear. It exists.

But that’s where the rational part of its execution ends. Instead of using diplomatic channels or working toward long-term agreements, Trump chose the path of abrupt action: tweets, sudden tariff changes, public intimidation of allies. What should have been a strategic reassessment of global trade through tariffs has turned into an unpredictable show.

So even when the decision rests on logic, that guarantees neither competent execution nor safe consequences. The global economy is cracking severely, not so much because of shifts in underlying structures or institutions, but because one man decided it was better to slash first and ask questions later. Whether that turns out to be better in the long run remains an open question.

The task facing the administration is, frankly, one that may be unsolvable. But that doesn't mean the approach has to be equally chaotic. If anything, the attempt to solve it should be surgically precise, not a merciless bloodletting whose consequences can only accelerate the collapse of the current world order while continuing to widen the deficit. Living with a deficit is possible for a while. But the outcome is predetermined.