What is wrong with the pricing of the energy crisis consequences?

Markets are pricing in aggressive rate hikes based on 2022 nostalgia, falling into a trap where raising rates now is monetary suicide, not inflation control.

Following the blockade of the Strait of Hormuz, global markets almost instantly returned to the rhetoric of 2022. Oil prices surged, investors began repricing the rate trajectory, and expectations regarding future monetary policy tightening once again became one of the main topics for financial markets. Just a few months ago, the market was actively discussing upcoming rate cuts from the Fed, ECB, and BoE. Now, however, a completely different question is being raised more and more frequently, whether central banks will have to return to rate hikes once again.

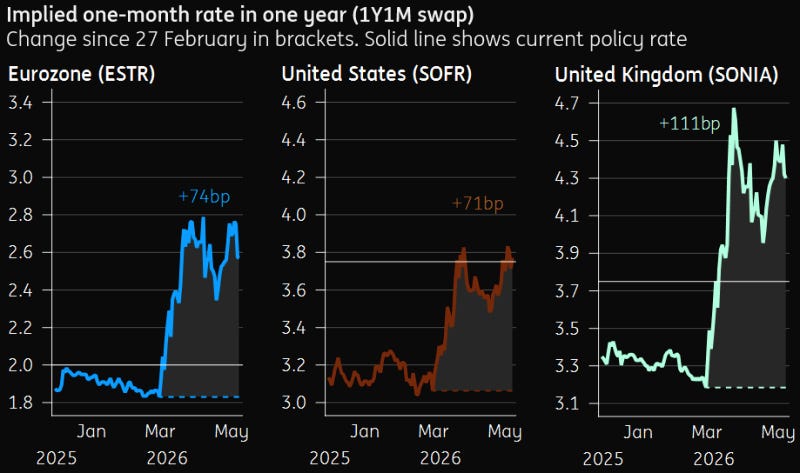

How markets have repriced future interest rates:

And this looks logical. An energy shock is almost automatically associated with inflation. More expensive oil quickly translates into higher costs for transportation, logistics, aviation, food products, and industrial manufacturing. For consumers, this means more expensive fuel, for businesses, it brings a new wave of rising input costs and for central banks, it poses the risk of inflation getting out of control again, just at the moment when they had already started talking about a gradual normalization of policy.

But the problem is that markets today might be looking at the situation too much through the prism of 2022. Back then, the energy crisis hit an economy already overheated in the post-pandemic environment, with global demand rebounding sharply, supply chains remaining disrupted, the labor market exceptionally strong, and governments continuing to support growth through large-scale fiscal stimulus. It was this exact combination that laid the groundwork for a full-scale inflationary wave and the most aggressive rate-hiking cycle in decades.

Today, the starting conditions look different. The global economy is entering a new energy shock with significantly weaker growth, a cooled labor market, and interest rates that are already near or even above neutral levels. In other words, while in 2022 central banks were fighting an overheated economy, now they risk facing both a new inflationary impulse and an additional blow to economic growth at the same time.

That is why the main question today is not just how high inflation can rise due to the oil shock. Far more important, however, is whether central banks are truly prepared to tighten policy aggressively again and risk completely stifling economic growth. Or is the market currently overestimating the future tightness of global monetary policy, automatically projecting the 2022 scenario onto a completely different macroeconomic reality?

Why this oil shock is different from 2022

Despite obvious parallels with the beginning of russia’s war against Ukraine, the current energy shock differs in one fundamental respect, as the global economy is entering it in a significantly weaker state. This is precisely what could drastically change the reaction of central banks and limit the scale of the future tightening cycle that markets are currently actively pricing in.

In 2022, inflation was already a problem even before the energy crisis. And here is why: