SaaS Armageddon

AI is undermining the seat-based SaaS model faster than Claude can code. But the survivors will be those who rewrite their pricing for agents, not empty chairs.

In the age of AI, capitalism is going through a fundamental rupture comparable in scale to the shift from an agrarian to an industrial model. Where surplus value was once inseparable from the exploitation of human labor, today algorithms and data centers are gradually taking over as the primary source of profit, generating it through exponential scalability without fatigue or strikes. The SaaS industry, built on per-user subscriptions, finds itself in the crosshairs of AI agents capable of replacing entire departments, which is driving a collapse in multiples across the sector. I’ll try to explain why this is happening and what will replace the old rules.

The Labor Market

For most of human history, the surplus value of any commodity was ultimately generated exclusively by human labor. Raw materials have no market value on their own: deposits of metal in the earth, oil beneath layers of rock, or timber in the wilderness don’t become commodities until labor is applied, until they are extracted, processed, and given the form in which they can be exchanged. In this sense, a commodity emerges from a sequence of purposeful labor operations that transform the natural state of things into a generally accepted product form.

Raw material provides the material base, but it is labor that adds to it form, functionality, and use value, and with it exchange value. It is on this labor that the markup is applied, which is what forms surplus value. Capital seeks to buy people’s working time as cheaply as possible and sell the results of that time as expensively as possible. Let’s look at all of this in the chart below.

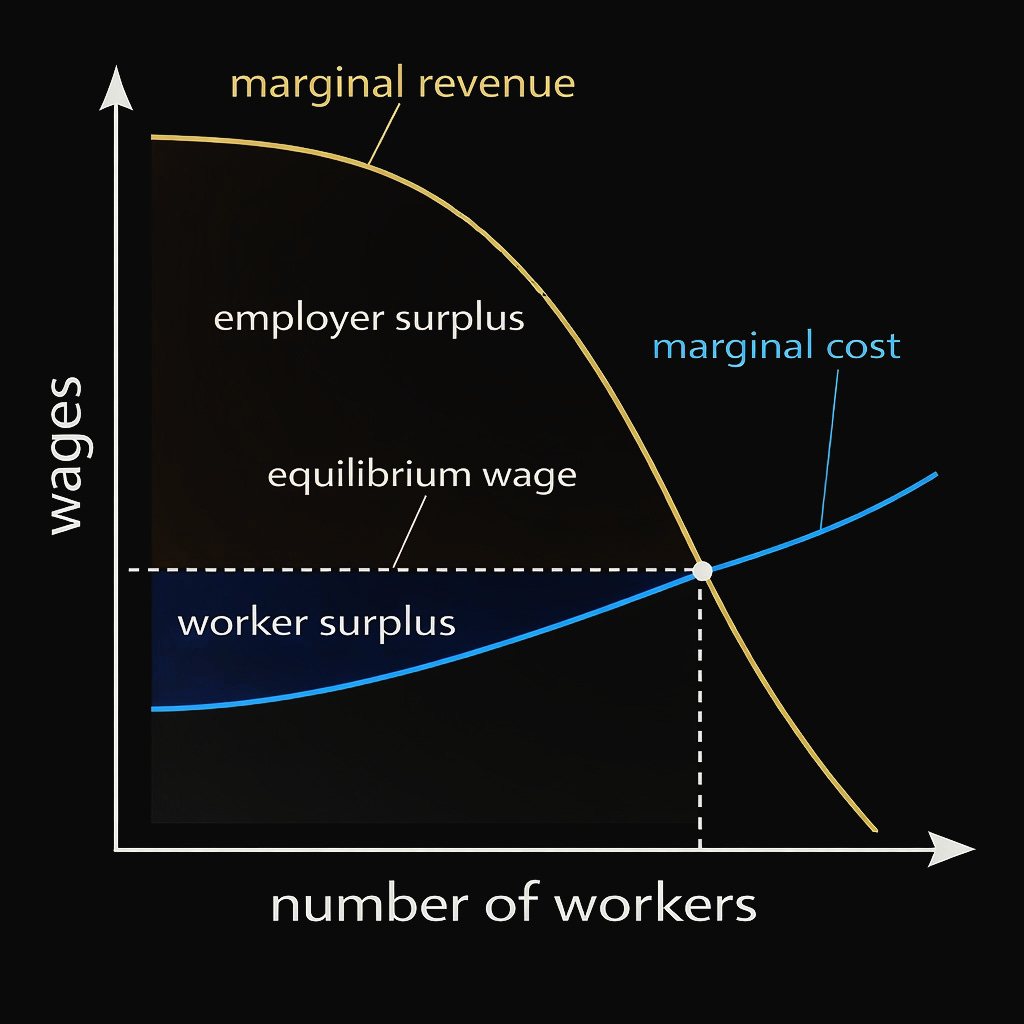

This shows the labor market from the perspective of a single firm. The vertical axis shows wages, the horizontal axis shows the number of workers. There are two main curves. The blue curve is the marginal revenue product of labor, showing how much additional revenue each new employee brings to the firm. It declines because as the number of workers increases, the contribution of each new employee typically diminishes, and the law of diminishing returns kicks in, which I described in some detail in the previous article.

The orange curve represents the marginal cost of hiring. It rises because to attract more workers, the firm has to offer higher wages. And since raising wages may affect not just the new employee but existing ones as well, the actual marginal cost of hiring rises faster.

The intersection of these two curves is the firm’s optimal level of employment. At this point, the additional revenue from a worker equals the additional cost of hiring them. Below this point it’s profitable to hire more; above it, the benefit disappears. The horizontal dashed line through this point shows the equilibrium wage.

The area between the blue curve and the wage level constitutes the employer surplus. This is the difference between what workers bring to the company and what they are paid. The area between the wage level and the labor supply curve (effectively the lower portion of the chart) reflects worker surplus, meaning the difference between the wage actually received and the minimum they would have been willing to accept. That’s the whole explanation of how profit from labor is formed.

Hence the constant corporate logic of seeking out territories where labor costs the least: colonial systems, then the offshoring of production, the relocation of factories and service centers to cheap-labor regions, the exploitation of migrants, and other forms of reducing the cost of human labor. At the root of all this is the widening gap between what an hour of labor costs on the labor market and what a capitalist can sell the results of that hour for on the goods and services market. And that’s precisely why we see the growing pay gap between management and workers.

Of course, the modern financial system has also played a significant role, feeding capital growth for decades with helicopter money, meaning cheap liquidity, credit expansion, and quantitative easing. These mechanisms allowed capital not just to preserve but to widen the gap between labor income and capital income, deepening wealth concentration and the real economy’s dependence on financial flows.

But as I wrote in the previous piece, a new factor has appeared in the modern era: artificial intelligence, which intervenes not just in the level of costs but in the very paradigm of labor pricing. Where added value was once inseparable from human labor, meaning hours of programming, analysis, design, AI is now shifting a significant volume of these operations into automated production, where the marginal cost per unit of output approaches zero after the initial investment in models and infrastructure. Tasks that used to require dozens of man-hours are now completed in milliseconds by a machine, with minimal variable costs and virtually unlimited scalability. This isn’t just the automation of physical labor, as on the assembly line during the Industrial Revolution, but an attempt to reproduce human intelligence, where algorithms replicate and amplify cognitive functions that were previously the exclusive domain of humans.

The result is a product where surplus value is increasingly generated not through the exploitation of human labor but through rent on ownership of technological infrastructure. The hunt for cheap labor gives way to competition for access to models, data centers, and algorithms. The markup shifts from man-hours to machine-time, which doesn’t tire, doesn’t strike, and scales exponentially. The man-hour as the universal metric for valuing labor and cost is distorting, and with it the entire logic of pricing and the distribution of surplus product, forcing a rethinking of the sources of profit in the modern economy.

The Problem Everyone Is Shouting About

AI is already rewriting the nature of programming. Tools like Claude, Cursor, and Copilot generate nearly half of all code, with developer acceptance rates exceeding 30%. According to GitHub, tasks are completed more than one and a half times faster. In practice, AI handles routine work better than a junior specialist with a few years of experience, writes cleaner code, and fixes bugs faster.

Sounds great. But that’s exactly where the problem starts.

Most IT companies built their business model on simple logic: the client pays for specialists’ time. More developers, longer projects, higher fees. If one developer with AI does the work of three, the project requires fewer people and fewer hours.

The client is happy, getting the same result for less. The vendor suffers, because its revenue depends directly on the volume of human labor. That’s the cannibalization dilemma: technology undermining the profitability of the very party deploying it.

The same logic hits the SaaS model from a different angle. A client company would buy 50 Salesforce or Slack licenses at $50-100 per seat, the seat-based model. Growth in headcount automatically meant growth in the monthly bill. A great arrangement, as long as all users were human. Goldman Sachs analysts now warn that the per-user model has no more than five years left. AI agents are taking over, handling tasks end-to-end, from writing reports to closing deals. One agent replaces several employees, and the need for extra seats simply evaporates.

Some companies have already proven this in practice. At Klarna, after deploying agents, revenue per employee doubled and approached nearly a million dollars. SaaStr replaced its sales team with agents and maintained the same revenue. According to BCG, 40% of clients explicitly say they are reducing the number of paid seats to cut costs.

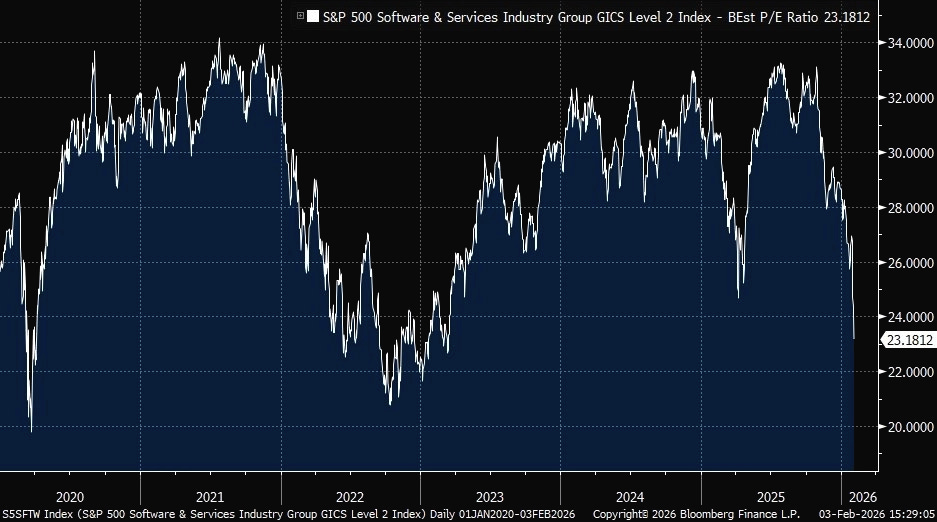

The real paradox is that vendors are trying to retain clients by adding AI to their products, but clients immediately use these features to cut their spending. Take ServiceNow: despite subscription growth and hundreds of millions from new AI services, the stock is falling because investors doubt the scalability of the new model. Profit, meanwhile, is steadily shifting toward owners of infrastructure and computing capacity. The market is responding with lower valuations, with P/E ratios already down from 30 to 20-25.

Vendors face a choice: transition to outcome-based pricing and take a share of the savings they create, or keep losing clients who have learned to count digital agents rather than people.

A note on Salesforce.

Let’s look at a specific case instead of staying in the abstract.

Salesforce is essentially a giant business Excel that stores customer contacts, deals, and reports. Large corporations like Coca-Cola have spent decades loading terabytes of data into it, building integrations, access rights, and processes. Migrating all of this to a custom-built AI product would be enormously expensive and risky. So companies like that will almost certainly stay on the platform as a reliable warehouse of data and relationships.

But the main blow lands on the analytics and AI features. Salesforce sells Einstein Analytics for around $50-75 per user per month. That used to look like a reasonable purchase, since without in-house expertise it was difficult to build dashboards, forecasts, and customer insights. Now you can export the tables to CSV, feed them into any AI service, and get charts, analysis, forecasts, and segmentation in a few minutes, possibly more flexible than anything the built-in module provides. Features that used to command dozens of dollars a month are gradually losing their value, and billions in potential subscription revenue are evaporating with them.

The next blow falls on new customer acquisition. Previously, a startup that needed a CRM almost automatically looked at off-the-shelf SaaS. Now executives realize they can build an MVP with AI assistants in an environment like Cursor or Replit, use an open-source stack, and skip the per-seat rent entirely. For this reason, the market is recording a slowdown in new user additions as clients shift to optimizing existing licenses rather than expanding.

Large platforms with deep data and high migration costs, like Salesforce and Workday, are still holding their ground. But niche SaaS products with a set of analytics widgets are losing value and risk disappearing. The strong get stronger, the weak disappear. AI is simply radically accelerating the natural selection that was always happening anyway.

The Other Side

Since the 2000s, the internet lowered the cost of distributing software. AI is doing the same to the process of building it. Development volume is growing almost exponentially, costs are falling, and as code gets cheaper, companies start automating tasks that used to seem too complex or unpredictable.

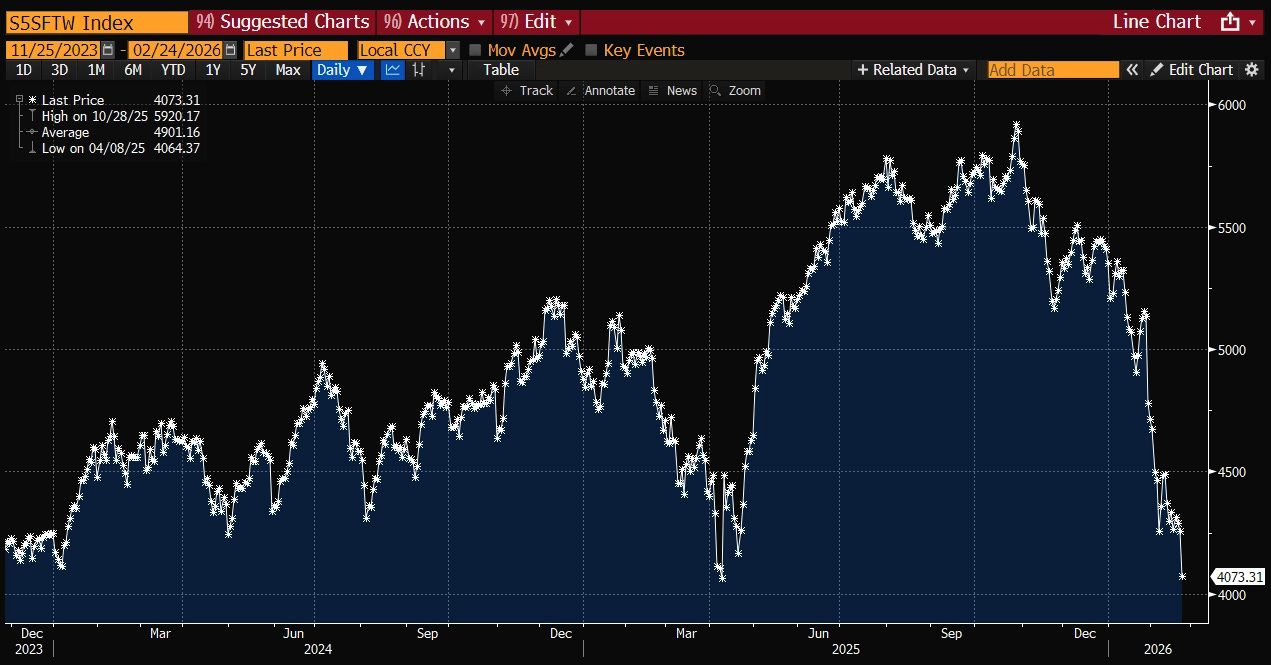

But the market sees only one side of the picture and panics. The software company index has fallen by a third since October, driven by the explosion of AI news. Investors have bet on the complete collapse of the entire SaaS model, as if everything will disappear tomorrow. Revenue multiples fell from 18-19 at the 2021 peak to 5.1 by December 2025. Revenue growth slowed from 17% in 2023 to 12.2% in Q4 2025.

Yet operationally, most SaaS companies remain quite healthy. The average public SaaS company generates $179 million in operating cash flow per year. Revenue is growing, free cash exists. But the market is punishing everyone wholesale, without distinction.

That’s the mistake. Market participants are lumping two fundamentally different types of business into one basket and applying the same discount to both.

The first type is deterministic systems: CRM, ERP, accounting. These require absolute precision, rule compliance, integration with client data, and proven business processes. A company that stores client data for decades, executes complex business logic, and integrates with thousands of other systems is critical infrastructure. AI isn’t a competitor here, because errors are unacceptable and migration costs are prohibitive.

The second type is probabilistic systems with pattern recognition, content generation, analytics widgets. If AI can replicate them at 90% of the quality for 10% of the cost, those businesses will collapse. These products are genuinely vulnerable, and the market is right to be worried about them.

But the problem now is that all SaaS trades at the same multiples: those with free cash margins five times over revenue and data on thousands of clients, and those selling one-off reports. That’s the investment opportunity, because once the market notices this difference, multiples will normalize and the opportunity will disappear along with them.

Writing code with AI accounts for roughly 1% of the work. The other 99% is reliability, scaling, security, and updates. Vibe coding is good for drafts, but it doesn’t replace deep systems understanding. Goldman may be right that tectonic shifts are coming in five years. But that’s a forecast, not a verdict.

Adaptation

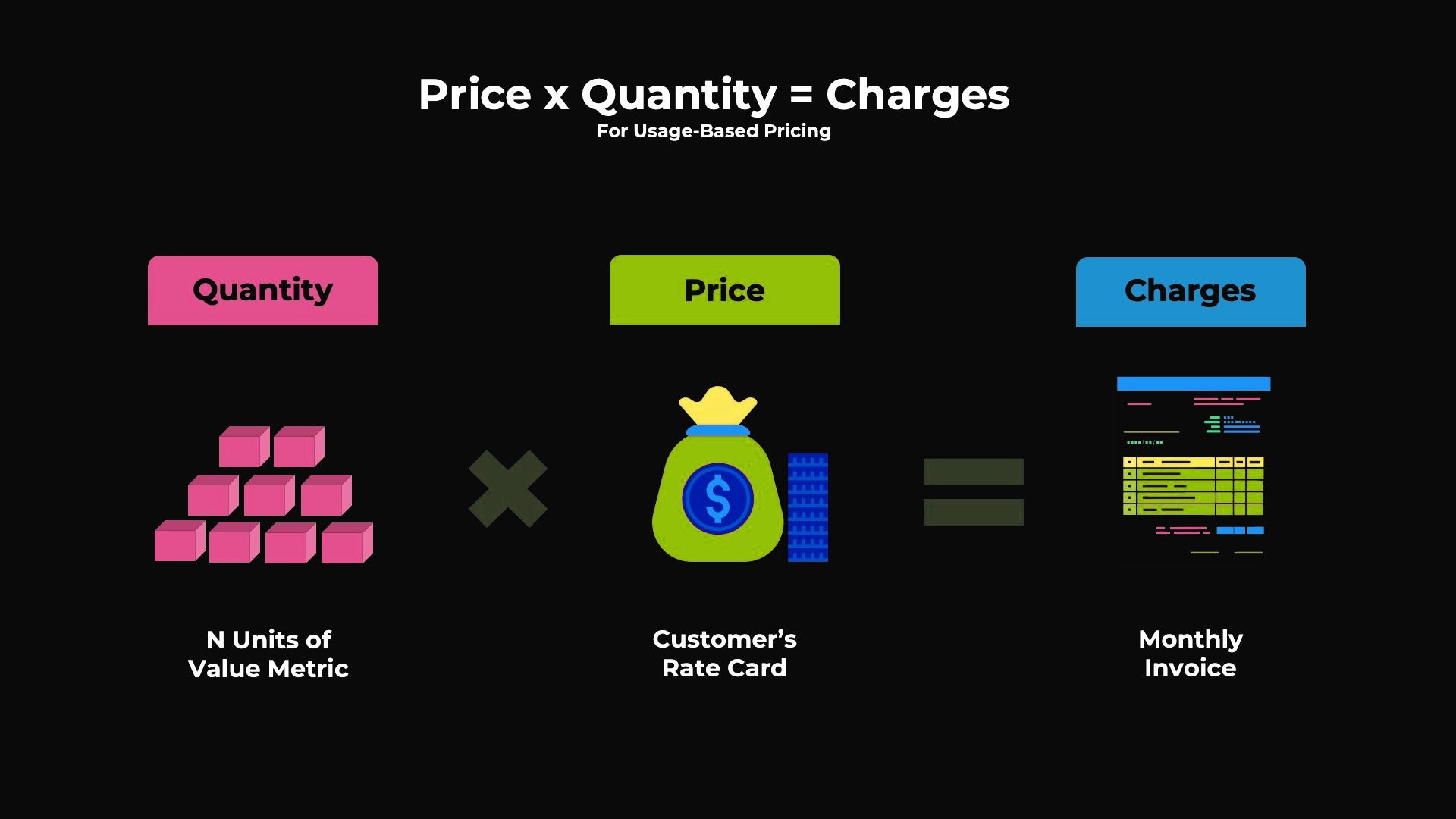

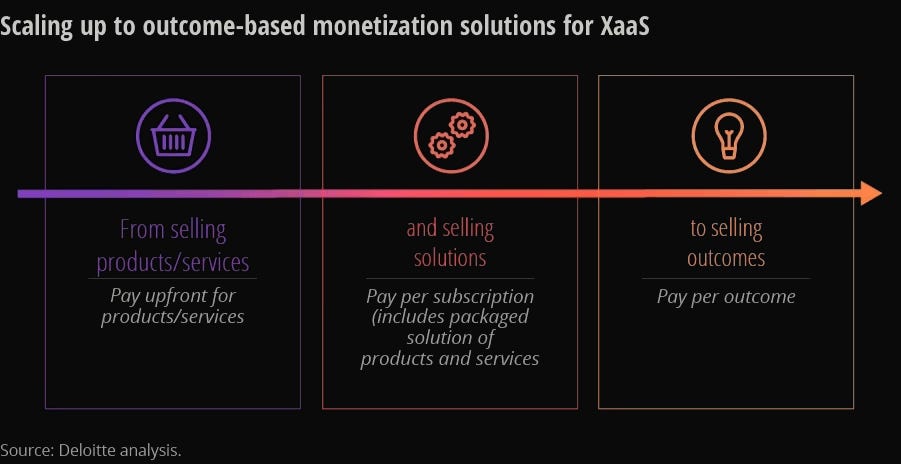

The pricing model will inevitably move from per-user toward payment for result, volume, or actual value. Charging for AI agents under the old model makes no sense, and vendors will have to accept that whether they want to or not. Two competing paradigms will take its place.

Usage-based: payment for volume, where the number of requests, transactions, computations, and API calls gets monetized. The more actively agents use the platform, the higher the bill. For the vendor this is good news, since agents work around the clock and at scales unavailable to humans, so total consumption volume can grow many times over even as the number of human users shrinks. That’s precisely why some platforms in the new reality won’t get cheaper but more expensive. An agent integrated with ERP and sending thousands of requests per hour generates far more revenue than a manager who opened the CRM three times a day.

The downside of this model is unpredictable costs for the client. Companies used to a fixed software budget suddenly get a bill that depends on how intensively agents are working. This creates a new type of negotiation, where the business must answer not “How many seats do we need?” but “How many operations are we planning per month?” And that’s a question most companies can’t answer right now.

Outcome-based: payment for a specific result, whether a closed deal, a resolved ticket, a processed document, or a generated lead. The model is elegant: the vendor literally takes responsibility for the product’s value, not just for the fact of its delivery. The client pays only when something actually happened. This shifts the relationship from transactional to partnership.

But how do you measure the result? Who’s to blame if the deal didn’t close? Did the agent underperform, or did the manager ruin it on the final call? Outcome-based pricing requires clear attribution, and business processes are rarely that transparent. The first companies to solve this measurement problem will gain an enormous competitive advantage, not because their product is better, but because they’ll be able to prove that it works.

In practice, companies will likely arrive at hybrid models: a fixed platform fee for access to data and infrastructure plus a variable component based on volume or results. Something like a gym membership with a separate fee for a personal trainer, except this trainer never tires and is never late.

Horizontal companies with universal products will remain under maximum pressure, because competition is high and any new player with a smart algorithm can do the same thing faster and cheaper. Vertical companies built around a specific industry, with its rules and processes, are more resilient. To threaten such a business, AI would have to replicate almost the entire industry expertise and offer a price 4-5 times lower at the same time. That’s substantially harder than replacing an analytics widget.

A large auto manufacturer isn’t going to build its own ERP managing billions of dollars. An error for such a company would cost not just a regular employee their career, but top management as well. Nobody applauds a perfect payroll calculation, but a failure gets noticed immediately. It’s simpler to rent from specialists who have worked it out on thousands of clients. Nothing will fundamentally change here, only how the bill is calculated.

In fast-changing areas like technical support or lead generation, older large firms often lose out to speed. But only if AI complements their core, rather than competing with it. New narrow niches will be taken by emerging companies. Large players with data on thousands of clients, complex processes, and convenient APIs for agents will strengthen their position.

Conclusion

Artificial intelligence is not destroying SaaS but rebuilding it for the agent era, where platforms with data and integrations will survive and vulnerable widgets will disappear. The shift to volume or outcome-based pricing will allow machine activity to be monetized, strengthening large players and driving a recovery in the market and multiples accordingly. In the end, profit will shift toward infrastructure, and the labor economy will evolve from the exploitation of man-hours to rent on algorithms, defining the new winners of techno-capitalism (or “techno-feudalism,” to borrow from Yanis Varoufakis).

This isn’t the end of enterprise software, but its upgrade, with a redistribution of who exactly will collect the cream.

And the first to collect it will be those who manage to rewrite not just the product but the price list.